What’s more, the modern networked economy has made it easier than ever for unsociable techno-nerds to make serious money. Just think of all the crypto-millionaires who mined made-up money in their basements.

But for most of us, moving in wealthier circles will raise our expectations – and potentially our bank balances.

Even Warren Buffett’s best friends include fellow billionaires Charlie Munger and Bill Gates.

A rich vein of study

There’s plenty of scientific research to back up this folksy-sounding advice.

To give a recent example, in a major study published in 2022 a team led by Harvard economist Raj Chetty studied the social networks of more than 70 million Facebook users to see if they could correlate their social capital with their financial wealth.

As Business Insider reports, out of three ways of measuring social capital:

…the only one actually linked to upward economic mobility is friendships with people from a higher socioeconomic status.

In fact, if lower-income kids grew up in areas that have the same economic connectedness as higher-income kids’ neighborhoods, their future earnings increase by an average of 20%.

According to Hugh Lauder of the University of Bath, Chetty’s research is a call to ensure schools are well-mixed in terms of socioeconomic background – albeit that’s difficult given how some parts of the country are far richer than others.

The alternative – an educational system where a lot of rich kids are segregated into their own schools – is bad for social mobility. (And for our politics).

One kink I noticed from the New Scientist reporting is that the Harvard team estimated income levels via the proxy data of each Facebook user’s mobile phone model.

More than 15 years as a personal finance blogger makes me wonder – were some of those apparently upwardly-mobile friends of richer people just flashing a fancy handset to keep up appearances?

Presumably the academics eliminated the risk of such social striving from affecting their results.

Big fish, small pond

There’s just one snag with the strategy of having richer friends, especially in childhood.

I’ll illustrate it via a slightly stylized story about an ex-girlfriend.

My ex – let’s call her Catherine – is a talented violin player. From the age of seven, she showed great promise with the instrument. By her early teens she was established as the best bow in town.

Catherine enjoyed being the lead violinist in her school orchestra. But she knew she could push her talent further than her school could take her. Most of her friends might as well as have been banging on saucepans for all they could inspire her.

Catherine’s teacher agreed she was being held back. He arranged for her to go to weekend classes in London at a fairly prestigious music school.

At last she’d be among musicians of her own caliber!

To cut a long story short, they were indeed better than her – and she didn’t like it one bit. No longer was Catherine the biggest fish in a small pond. In fact, by her own estimation she was the worst musician at the new school.

Catherine continued to attend the classes, because she was too ashamed to retreat to her old school colleagues. But she admits that her heart wasn’t in it. When she went to university, she didn’t even bother to join the music society.

Could Catherine have tried harder? Perhaps. Many people respond to competition, but some are too timid. A shy person, Catherine wilted in the light of others.

Yet the fact is she can play beautifully compared to 99% of people who ever pick up a violin.

Rich friends when you need them

If Catherine had never gone to the elite music classes, she’d probably have had a happier childhood. She might still be playing her violin today.

Similarly, you will make more money if you meet rich friends, but you’ll likely feel miserable.

Researchers from Warwick Business School in the UK found that people who earned more than others in their “reference group” – that is, those of the same age, gender, religion or nationality – were more likely to feel happy with their lives.

Warwick professor of behavioural sciences Nick Powdthavee said that people actually care “very little” about the actual figure they earn, but they are concerned with how their income compares to those around them.

“For example, their sense of wellbeing is more likely to be influenced by whether they are fifth or 40th highest-paid person in their workplace, rather than their precise salary,” he explained.

So do you want to be rich or would you rather be happy?

Perhaps the best solution is to decide who your real friends are – as distinct from who is in your wealth creation circle.

Spend quality time with your true friends for a pick-me-up, and hang out with your rich friends when you see your income sliding!

I know we only recently revisited the meme stock mania of 2021, when I reviewed the Netflix documentary Eat the Rich.

But there’s no better post to flag up today than Alexander Hurst’s epic variation on the theme in the Guardian this week.

The title – How I turned $15,000 into $1.2m during the pandemic – then lost it all – sets the stage.

But there’s more than just ‘loss porn’ to Hurst’s account, as we’re shown how suddenly coming into money warps your thinking:

I stopped searching for 50 sq meter one-bedroom apartments in central Paris and instead started browsing €1.5m lofts with rooftop terraces, or scrolling through Sotheby’s listings in French Polynesia, drooling over a small private island I could buy for $890,000 – as in, I could actually buy it.

It wasn’t hard to rationalize it. After all, my Amherst classmates had grown up going to vacation homes and boarding schools, and were destined to inherit large transfers of property or investment wealth.

I would not; instead, I felt the impending burden of my parents’ underfunded retirement accounts looming.

The piece really spoke to me: Hurst feels like a brother from another mother who went down a rabbit hole I avoided only by being born 20 years earlier.

And it takes guts to admit to such losses – and the truths that lie behind them – in public.

As my co-blogger wrote when he revisited the bursting of the 2021 bubble:

The market mints winners and losers every day.

The tricky bit is that failure is silent, while success is noisy.

Generally that’s true – but this time has been different.

The Reddit traders paraded their successes and failures very publicly throughout their epic bender.

Maybe that’s why this time we’ve been given an account of the morning after.

The first trillion is the hardest

Notes from the meme stock boom are not easy reading for the squeamish, what with all the leverage and the roll call of trading tools like options and shorts – as well as plenty of obscure small cap stocks.

But the truth is you can lose a lot of money just fine with everyday investing into some of the biggest companies in the world.

As Ben Carlson says over at A Wealth of Common Sense this week in recounting the fall from grace of Meta (nee Facebook):

I’m not trying to pour salt in the wound here for people who own these stocks.

This is just a not-so-gentle reminder that stock picking is extremely difficult, even over the long run and even for best-of-breed corporations.

On the way up you kick yourself for not investing in name-brand companies with stellar stock performance.

Then when they inevitably crash you begin to wonder if those gains are ever going to return.

For those who don’t follow the market with a magnifying glass like me and Ben, this chart shows how Meta has left the trillion-dollar market cap club:

Despite being one of the most successful and profitable companies of all-time, Meta has now been beaten by a diversified index fund over the past decade.

For love not money

When I used to write more about my naughty active investing – that stands in such contrast to the Monevator house view and the wise posts of my co-blogger – I was sometimes accused of hypocrisy.

Why was I telling people they should invest in boring index funds, when I do something completely different?

Was I keeping all the good stuff to myself? Did I think I was better than everyone else?

That sort of thing.

Follow that link to learn more about why I’m still a stock-picker and an active trader, for my sins.

But let’s be clear about one thing.

I haven’t increasingly told people over the years that they’ll almost certainly do better with index funds despite my being an active investor.

On the contrary, I know all the market’s capricious whims. The agonies and ecstasies, as Ben puts it.

And I say you’ll almost certainly have a more pleasant life if you invest passively because of my experiences as an active investor!

Enjoy the weekend, and the many great links below.

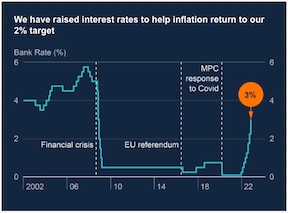

I can’t think of a much trickier in-tray than that facing governor Andrew Bailey at the Bank of England right now.

The institution he runs just hiked UK Bank Rate by 0.75% to 3% in the biggest jump for three decades.

And nobody is very happy about it.

“Too much too soon!”

“Too little too late!”

Everyone could do a better job than Bailey.

Never mind that just a month ago the Bank had to intervene directly in the market to stop a liquidity crisis in gilts cascading into the banking sector.

A mini-crisis manufactured overnight by wonks, that took less than a week to blow up.

And never mind – as many now seem to forget – that less than three years ago we faced a depression had not governments and central banks alike acted to offset the economic hit caused (unavoidably) by Covid and (perhaps over-egged) by repeated lockdowns.

Just look at where this interplay of fiscal stimulus, near-zero interest rates, economic inactivity, Brexit, and the shifting demand for goods and services has put us:

Average five-year fixed mortgage – 6% (highest for 12 years)

GBP/USD – $1.12 (down 15% over five years)

Number of UK chancellors since July 2022 – four (careless!)

10-year gilt yield – 3.5% (up 250% since the start of the year)

It’s a cat’s cradle of contradictory indicators – and it could have been worse.

Truss and Kwarteng: gone but not forgotten

In the wake of the Truss and Kwarteng mini-budget show (parental discretion advised) the market briefly expected the Bank of England to have hiked rates by as much as another 2% by now.

That fear saw banks scrambling to raise their mortgage rates, if not pull their products altogether.

Thankfully the decapitation of the Truss regime saw new chancellor Jeremy Hunt undo a lot of that damage. Rishi Sunak as prime minister has further soothed frayed nerves.

It now feels like a bad dream. We still got the same 0.75% interest rate rise that we expected before Liz Truss had ever said she’d never resign for the first time.

Except that like in some horror movie where the relieved victim wakes up from a nightmare only to discover their cat impaled on a candlestick in the living room, those higher mortgage rates have yet to drop back to where they were.

Partly as a result, some pundits now forecast house price falls of 10-15%.

And if you think that’s not so bad – overdue if anything – then be careful what you wish for.

So long and thanks for all the cheques

Because just as one does not simply walk into Mordor, one does not simply repeatedly hike rates, play musical chairs with prime ministers, and ding the housing market without consequences.

Sure enough, the Bank of England has got even gloomier about the economy.

It already thinks a recession is underway. And its chart now suggests the pain will last for two years:

The good news is the Bank’s central projection is for a shallow recession, albeit an overlong one.

The better-but-not-exactly-news-news is that – contrary to what many people now protest – if the Bank and politicians hadn’t acted in 2020, then that plunge in GDP (orange line) would have taken far longer to bounce back.

In other words, the pain we’ll suffer soon is to pay for what we avoided back then.

The Bank of England governor under fire

For me, inflation continues to be the truly perplexing puzzle.

Some left-leaning rabble-rousers economists pitch the BoE as raising rates simply to mete out justice:

If your mortgage is £100,000 that Bank of England have just signalled they want to take at least £750 a year out of your annual income to punish you for inflation. How does that make you feel? And do you agree that inflation was all your fault in the first place?

According to this fellow, Andrew Bailey actively wants to put millions out of work.

Obviously I don’t see it that way. Because I am a grown-up.

Nevertheless there is something perverse-seeming about raising rates even in the same breath as you forecast a two-year recession.

And I find the issue even more vexing because I’m seemingly one of the last people who still believes (perhaps being biased, having predicted it) that it was mostly the economic disruption caused by the pandemic and repeated lockdowns 1 – rather than solely excessive monetary and fiscal stimulus – that’s behind most of this inflation.

But whatever the origin story, at least inflation is forecast to start falling sharply, and soon:

Nevertheless on these figures as published, the Bank of England expects unemployment to climb above 6% by 2025.

Which will be miserable for anyone who loses their jobs – especially if house prices do start to fall sharply.

Indeed it’s not hard to see the potential for a fresh ‘doom loop’ where forced selling meets negative equity to make a bad situation even worse.

Think early 1990s, only with social media.

All of which is also what makes investing especially tricky at the moment, incidentally.

I’ve been getting more bullish for a while, partly because I had judged that market expectations for US rates were peaking.

But this isn’t a sunshine and roses view. Rather it’s because I think rising mortgage rates in the US have already done enough to throw that nation’s housing market into a funk.

It’s a similar story in the UK – albeit more Monty Pythonesque thanks to our political backdrop.

For me it’s a reason to avoid entirely abandoning those hated growth stocks, and to be wary of overloading on the cyclical value-style shares that have done so well since the end of 2021.

My hunch is the worst of the valuation compression is behind the growth companies, while at the same time the economic outlook is deteriorating for cheaper but less exceptional firms.

As for passive investors, no reason not to keep on trucking of course.

At least your bonds will be increasingly throwing off useful income.

Bailout Bailey?

As recently as December 2021, Central Banks didn’t think inflation would get so high, nor that they would have to raise interest rates by very much.

Low and slow was the forecast back then.

I can understand why central bankers feel they have to act tough now, given how wrong they were. But I also think a sharp pivot is increasingly more likely than not, as the cumulative effect of all this tightening adds up.

Personally, I see stagflation threatening to turn into mild deflation as becoming more of a risk than runaway inflation.

But it doesn’t have to end so bleakly either way. We could yet muddle through.

As anyone who saw the Lord of the Rings knows, it turned out you could simply walk into Mordor.

So perhaps Andrew Bailey similarly can raise interest rates, slow the economy, and then pull us up out of the descent before we dive into a really deep decline.

Bonds are among the most confusing and misunderstood of asset classes. This makes it harder to choose a bond fund suitable for your objectives and exposure to risk.

Bonds are often lazily mischaracterised as ‘safe’. They can be anything but. A major problem is the term ‘bonds’ covers a vast menagerie, running from benign to beastly. Yet the bond funds that most of us need can be boiled down to a handful of choices.

2022 has been historically bad for bonds. But we’d still argue they belong in a diversified portfolio, along with equities, cash, and perhaps gold.

It’s all part of weatherproofing your wealth against whatever economic switcheroos come next.

To choose a bond fund that’s best for your needs, you need to match their properties to your investment goals and the threats that could derail you.

The following table maps portfolio demands against the most appropriate bond fund type to fulfill the brief:

Role

Bond fund type

Diversify against deep recession

Long government bonds

Protect against rising interest rates

Short government bonds

Finance near-term cash needs

Short government bonds

Balance current risks vs reward

Intermediate government bonds

Protect vs unexpected inflation / stagflationary recession

Short index-linked government bonds

Note: UK government bonds are called gilts, and the terms are used interchangeably.

That’s the York Notes version of the story. But it’s a good idea to scratch beneath the surface to understand the pros and cons.

Long government bonds, for example, are the best defence against a classic deflationary recession. But they’re a liability in stagflationary conditions.

And while index-linked government bonds are the best protectors against a sudden flare-up in inflation, they come with health warnings. Not all index-linked bond funds are the same. Take the same care when choosing between them as with a sharp axe when chopping wood.

The rest of this post is about understanding what you’re getting into and how to avoid the big bond fund pitfalls.

Bond aid

We favour high-quality government bond funds because they’re the best diversifiers of equity risk. In other words, when equities are down a lot, these types of bonds are the most likely to be up.

By high-quality we mean funds that are dominated by government issued bonds with a credit rating of AA- and above. A sliver of BBB rated bonds in the fund is okay, too.

Short, intermediate, and long refers to the average maturity date of the bonds held by the fund.

Maturity refers to the length of time a particular bond pays interest before the issuer redeems the bond in full.

A bond fund’s average maturity – reflecting all the bonds it holds – influences its level of risk. We explained how that works in our piece on bond duration.

Here’s the cheat sheet on how average maturity influences bond behaviour:

Short bond funds

Short bonds are less volatile. That is, they experience smaller swings in value (up or down) as interest rates change.

However, that makes them less beneficial in a recession, because they don’t make the capital gains that intermediate and long bonds do when interest rates fall.

Short bonds also offer the lowest expected return over time. Less risk, less reward.

Maturities range between zero and five years. Look up your short fund’s average maturity figure on its web page. It’ll be somewhere between 0 and 5.

Long bond funds

Long bond values are the most volatile. You can experience a significant capital gain when interest rates fall, or a loss when interest rates rise.

That typically makes long bonds more beneficial in a demand-side recession.

They offer the highest expected return over time (for bonds). More risk, more reward.

Long bond funds are dominated by maturities over 15 years. Average maturity is likely to be 20+.

Intermediate bond funds

Intermediate funds are the Goldilocks helping of bonds, versus the short and long varieties.

They are somewhat risky, moderately helpful in a recession, and offer a middling long-term expected return.

Intermediate funds hold bonds across a wide range of maturities, from short to long, and everything in between.

Average maturities range upwards of 8+ to the late teens, depending on the intermediate blend you pick.

Next time might be different. We’re describing here the typical behaviour of the various bond fund types. They are not guaranteed to work this way in the short-term or during every economic event. Learn more about bonds behaving badly.

Short index-linked bond funds

Index-linked bonds offer unexpected inflation resistance that other bond types don’t have.

Unexpected inflation means high inflation that consistently outstrips market forecasts. This is the most dangerous type of inflation for equities and non-index-linked bonds (often called nominal bonds).

Index-linked bonds make payments that are pegged to official measures of inflation.

This should make them useful in stagflationary recessions that hurt equities and nominal bonds.

But you may have to stick to short index-linked bond funds for reasons explained briefly below, and detailed in our post about the index-linked gilt market’s hidden tripwires.

Young investor bond fund selection considerations

Are you a young (ish) investor who wants to guard against the threat of a deep, deflationary recession? (Think Great Depression, Global Financial Crisis, Dotcom Bust, Japanese asset price bubble).

Then long government bond funds are the best diversifiers for you.

That’s especially the case if your portfolio is heavily skewed towards equities. (Say a 70% or higher allocation.)

Diversification decrees you want the bond class most likely to profit when your big equity holding crashes. That’s long bonds.

Meanwhile a 70%-plus equity portfolio is likely to be so volatile you probably won’t much notice the relatively wild swings of long bonds on top.

Consider the long bond trade-off carefully

The opportunity: Because you won’t withdraw cash from your portfolio for 30 years or more, you can ride out capital losses should bond yields rise. But when the world is laid low by a major recession, you should capitalise on surging long bond values as interest rates tumble.

In this scenario, long bond gains cushion your portfolio from equity losses. We’ve seen bond funds do just that during past market slumps.

Later you can mobilise your bonds as a source of financial dry powder. You sell some bonds to buy more equities while they’re on sale – a technique known as rebalancing.

The threat: Long bonds can suffer equity-scale losses during periods of rising interest rates and when inflation lets rip. This risk has materialised with a vengeance in 2022.

This chart (from JustETF) shows how one long UK government bond fund has dropped 36.5% year-to-date:

Hardly an easy loss to shrug off! Even a young investor should think twice about long bonds given the current balance of risks – the strong possibility of prolonged rising inflation alongside interest rate pain.

That goes double if you’re the sort of person liable to get distressed by individual losses in your portfolio. (Versus viewing it holistically as a system of complementary asset classes that thrive and dive under different conditions.)

Intermediate high-quality government bond funds may offer a better balance of risk and reward for you.

Olderinvestor bond fund considerations

Near-retirees or retired decumulators have a trickier balancing act. That’s because you’re likely to withdraw funds from your portfolio in the near-term.

Short bond funds and/or (especially) cash won’t suffer from a rapid capital loss like long bonds can. So owning them means you’re less likely to face a shortfall that derails your spending needs.

Demand-side recessions are still a threat to a retiree’s equity-dominated portfolio. But adding long bond fund risk on top can ratchet risk to an unacceptable level when there’s less time to wait for a recovery.

Again, intermediate bond funds chart a better course between the threats of rising interest rates and insufficient diversification during a crisis.

But why not just stick to short bonds or cash?

The next chart shows why. This is how short, intermediate, and long UK government bond funds responded during the COVID crash:

As equities caved during the early days of the crisis, long and intermediate bonds spiked almost 12% and 7% respectively.

Short bonds barely registered there was a pandemic on. Cash was similarly indifferent. So while these assets didn’t lose, they didn’t counterbalance falling equities much either.

On the right-hand side of the graph, you can see long bonds came out ahead, with intermediates and short bonds in the silver and bronze positions. Just as you’d expect in a deflationary slump.

Meanwhile – in the middle of the crisis – a whipsaw effect temporarily crumpled all gilts thanks to a sell-off by large investors desperate for liquidity.

It stands as a useful reminder that our investments rarely work like clockwork during a panic.

Inflation protection

There’s no one-and-done, slam-dunk solution to inflation risk.

Anyone who fears uncontrolled, high, and unexpected inflation should consider an allocation to short maturity, high-quality index-linked bond funds.

But young investors with a long time horizon could just inflation hedge using equities.

That’s because the long-term expected returns of equities are higher than index-linked bonds, even after inflation prospects are taken into account.

Retirees, by contrast, are better diversified if their defensive asset allocation includes a slug of short index-linkers.

The twin thumbscrews of rising interest rates and inflation are torture for nominal bonds. Short index-linked bonds are better equipped to take the pain:

Blue line: This short global index-linked bond fund (hedged to GBP) has returned -1.1% since inflation took off.

Red line: Our short, nominal UK government bond fund fared worse with a -6.4% return.

Orange line: But the intermediate, nominal UK government bond fund did worse still. It took a -24% hit in the last eighteen months.

The index-linked bond fund has fared better than its two nominal bond counterparts in an inflationary environment. Just as you’d expect.

What’s surprising is that the index-linked bond fund is down at all. What happened to its vaunted anti-inflation properties?

Index-linked bonds can fall even when inflation rises

The problem is that index-linked bond fund returns are composed of two main elements:

Coupon and principal payments that are linked to inflation

Interest rates can climb so quickly that the resultant capital losses can swamp an index-linked bond fund’s inflation payouts.

This is what has happened in 2022. Hence index-linked bonds haven’t protected our portfolios nearly as well as we’d hope.

In particular, long index-linked bond funds have been absolutely awful these past six months:

The long index-linked bond fund (blue line) is down 26% vs -1.1% for the short index-linked bond fund (red line).

Why? Because the long index-linked bond fund is much more vulnerable to rising interest rates. Its underlying bonds – with their longer maturity dates – are subject to more volatile swings in value when interest rates yo-yo.

That makes a short index-linked bond fund a better analogue for inflation. Though it too suffers (smaller) temporary setbacks from rate hikes.

And because there isn’t a short index-linked gilt fund in existence, you’ll have to choose a global government bond version, hedged to the pound.

Hedging to the pound (GBP) removes currency risk from the equation.

Global government bonds or UK gilts?

You also face choosing between high-quality global government bond funds hedged to GBP or gilt funds, which are still AA- rated (at least for now).

We used to be agnostic about this choice. There are good intermediate index trackers available in both flavours.

But then this happened:

Gilts got pummeled relative to global government bonds when Truss and Kwarteng went on their bonkers Britannia bender.

UK government bonds have since climbed someway back out of the hole. Sanity has been restored, but this was a wake-up call. A stiff lesson in the danger of concentrating your risks in a single country.

We Brits proudly think of ourselves as members of the premier league of nations. So was this a one-off shocker or evidence we’re on the brink of relegation?

Your answer to that will determine whether you choose gilts or global government bonds.

Government bond funds or aggregate bond funds?

Another decision!

Aggregate bond funds cut high-grade govies by mixing in bulking agents like corporate bonds. The upshot is you gain a little yield but you give up some equity crash protection.

Crash protection from bonds is paramount in my view, therefore I favour government bond funds.

Our piece on the best bond funds includes ideas for intermediate gilt and global government hedged to GBP bond funds.

And when you do come to choose a bond fund, this piece on how to read a bond fund webpage may help.

Hedged or unhedged?

Should you choose a global bond fund, we think the argument is tilted in favour of selecting one that hedges its returns to the pound.

In other words, you’ll receive the return of the underlying investments unalloyed by the swings of the currency markets.

Bonds are meant to be a haven of relative stability in your portfolio. (Even though that hasn’t been the case for many of us in dystopian 2022.)

If you invest without hedging then you’re exposed to currency volatility – on top of whatever else might be knocking your bond investments around. Such currency moves may work for or against you. It’s lap of the gods stuff, despite what that nice man on YouTube says.

Hedging removes currency risk. Probably a good idea in the case of bonds though probably 1 a bad idea for equities.

Hedging is particularly sensible if you’re a retiree who can do without their bond fund plunging just because some loony gets installed in Number 10 and tanks the pound.

Obviously UK-based investors don’t need to hedge gilt holdings. They’re valued in pounds in the first place.

Go West, young man (or bond-buying woman)

There is a nuanced argument that younger investors might want to choose to invest in unhedged US treasuries – or at least that those young investors who are very hands-on with their portfolios could consider it.

That’s because US government bonds and the dollar often benefit from safe-haven status during a crisis. As such, returns from unhedged treasuries may temporarily outstrip any gains from gilts valued in sterling.

If they do then you can sell your treasuries and pop the proceeds into gilts, potentially adding a kicker to your overall return.

Historically, however, gilts have then reeled treasuries back in over time. So this ploy probably isn’t worth the trouble for proper passive investors.

How to choose a bond fund: model portfolios

Here’s some asset allocations devised in the light of all these ‘how to choose a bond fund’ ideas:

Young accumulators

Asset class

Allocation (%)

Global equities

80

Intermediate global government bonds (GBP hedged)

20

Long bond funds are technically the best diversifier but we think that the threat of high inflation and continued rising interest rates makes them too risky right now.

There’s a more nuanced approach that involves holding a smaller allocation of long bonds while attempting to dampen the risk with an accompanying slug of cash. Read the Long bond duration risk management section of this piece if you want to know more.

Older accumulators / lower risk tolerance

Asset class

Allocation (%)

Global equities

60

Intermediate global government bonds (GBP hedged)

20

Short global index-linked bonds (GBP hedged)

20

Equity risk is cutback while unexpected inflation protection is introduced. Note that index-linkers are nowhere near as effective as nominal bonds during a deflationary, demand-side recession.

Decumulators use cash / short government bonds for immediate needs, equities for growth, intermediates as shock absorbers, and linkers for unexpected inflation defence.

Decumulators – max diversification

Asset class

Allocation (%)

Global equities

60

Intermediate global government bonds (GBP hedged)

10

Short global index-linked bonds (GBP hedged)

10

Cash and/or short government bonds (Gilts)

10

Gold

10

This portfolio adds gold to the armoury of strategic diversifiers.

Gold isn’t an inflation hedge per se. But it has worked relatively well in two rising rate environments that have hammered nominal gilts (the 1970s and now).

“I think interest rates will continue to rise…”

Okay, if you’re sure rates are headed higher then stick to cash.

Or if bonds seem too scary at the moment then stick to cash.

But remember that ever since the Global Financial Crisis ushered in near-zero interest rates, cash has done little more than protect your wealth in nominal terms.

You’ve lost spending power after-inflation with cash, whatever your bank balance says.

Look, we get it. 2022’s historic kicking for bonds has been so savage that even ten-year returns are lousy for many funds.

But it would be bold – to say the least – to bank on a repeat performance over the next ten years.

The expected returns from cash are worse than bonds over the long-term.

Cash is not a free pass.

If you don’t believe you can predict the future course of interest rates (you can’t) then put your faith in diversification.

If you’re still not sure, maybe split the difference: some cash, and some bonds.

Take it steady,

The Accumulator

P.S. If you’d like to know more about bonds then check out these posts:

P.P.S. When we mention ‘interest rates’, we’re referring to bond market interest rates, not central bank interest rates. References to ‘yield’ mean yield-to-maturity. Please see our bond jargon buster for more.

We are saying “probably” here not because we can’t be bothered to consult a textbook, but because the case isn’t clear-cut and nobody knows the future.[↩]