How filthy rich would you be if you could see tomorrow’s newspapers today – and then trade on the back of your unfair insight?

Actually, many people could end up poorer.

At least that’s the takeaway of new research by Victor Haghani and James White of Elm Partners Management.

They decided to investigate conjecture by Black Swan author Nassim Nicholas Taleb that knowing the news in advance wouldn’t help most people make money.

Haghani and White devised a clever experiment to test out Taleb’s hunch: 118 ‘young adults trained in finance’ were given $50 and a copy of the front page of something called the Wall Street Journal, minus stock and bond prices, one day in advance.

The lab monkeys’ task was simple — to use their knowledge of the future to make as much money as possible by trading in the S&P 500 and a 30-year Treasury bond futures contract.

Participants were free to use as much leverage as they liked and asked to place bets on 15 different high-volatility days over the past 15 years, five of which coincided with big employment reports, five of which coincided with Fed announcements, and the other five of which were picked purely at random.

Now, if you’re a naughty active investor like me you’re probably licking your lips in anticipation.

“It’s very humbling,” said Victor Haghani, who was a founding partner of Long-Term Capital Management.

“Even if you have the news in advance, it’s still really hard to do asset allocation or whatever with a high chance of being right, let alone not knowing what’s going to happen.”

Haghani was a Monevator reader back in the day. I’d love to think my co-blogger’s passive investing articles added our two pence to the intellectual capital behind this research. 😉

Anyway if you’re the sort who doesn’t believe something until you’ve tried it for yourself then you can (a) join our Mogulsmembership gang (and be sure to track your returns!) and (b) play the same game over on the Elm Funds website.

Lie about let us know how you do in the comments below!

You partied in your 20s and 30s. Or you had kids early and there was no money leftover. Or perhaps you got divorced and your partner took the lot. Bottom line: you’re late to start investing.

Are you doomed to eat cat food in your retirement? To be grinding out another shift in your 80s as the oldest barista on the block?

Probably not – provided you to take sufficient action now to turn things around.

You’ll need to be more focussed than a younger saver though, without their head start.

And maybe you should do a few things differently.

Saving grace

Imagine you’ve woken up penniless after 20 years in a coma – long of hair, but short of time.

The good news? You avoided selfies, Brexit, Covid, social media, and the last series of Game Of Thrones.

However you also missed out on two decades of compound interest effortlessly growing your wealth.

It’s a financial morality tale is as old as time spreadsheets, handed down from bloggers to Twitter pundits to TikTok influencers.

Person A and Person B both start work in their early 20s. They earn the same salary.

Person A notices there are a lot of old people around and begins to save, before they too get old.

Person B imagines they’ll wear crop tops forever, eats out or orders in every day, spends everything, saves nothing, and reaches their 40s with little to show for it except for a pretty Instagram account.

Run the numbers and Person A may already be headed for a comfortable retirement in their early 60s.

But person B will need to save much more – and/or for much longer – just to catch-up.

What happens when you invest early

We’ve marvelled at the mathematical wonder of compound interest on Monevator before:

Consider two investors: Captain Sensible and Captain Blithe.

From the age of 25, Captain Sensible invests £2,000 per year in an ISA for 10 years until he is 35. At 35 he stops and never puts another penny into his fund again.

Captain Sensible then leaves his nest egg untouched to grow until he hits age 65. He earns an average annual return of 8% and when he looks at his account 30 years later, he has £314,870 to play with.

Captain Blithe, meanwhile, spends the lot between the ages of 25 to 35.

Only when he hits 35 does he sober up and start tucking away £2,000 per year in his ISA. He keeps this up for the next 30 years until he reaches 65.

Captain Blithe earns an average annual return of 8%, too. He ends up with £244,691.

To recap:

– Captain Sensible has invested a total of £20,000.

– Captain Blithe has invested a total of £60,000.

Yet Captain Sensible’s pile is worth over 28% more than the late-starting Captain Blithe’s – even though Sensible only invested a third of the amount.

Compound interest takes a while to get interesting.

All things equal, the earlier you start, the bigger your pension snowball will be by the time you’re old enough to start worrying about it.

What if it seems too late to start investing?

Of course hearing “you should have started earlier” isn’t any more welcome in personal finance than when you’re facing last dibs at a swingers’ party.

There’s not much you can do about that now. What matters is how to best proceed.

The good news is that beginning in 2012 most people have been auto-enrolled into pensions at work.

But if this came too late for you – or if you didn’t put enough away – then start addressing things today.

Powering-up your pension

To catch up with swots like me who were aggressively saving by age 23, you have two broad routes:

#1: Take the conventional approach on steroids. Live much more frugally, spend a lot less, save much more, invest riskier, work longer – and try to do it all smarter to further ratchet up your returns.

#2: Do something different. Start a business, take a more active approach to getting rich, marry strategically, rob a bank, punt on crypto…

Clearly you can also pick-and-mix from these options.

But know that all of them – from making your own lunch to save an extra tenner to gambling your life savings on a start-up – come with potential risks, rewards, and the chance of outright failure.

Risky bets like putting real money into the likes of Bitcoin might well speed up your gains.

But very often taking bigger or less orthodox risks will see you do worse. People try to get rich quick because it promises a shortcut, not because of any stellar track record.

So you must consider the options for yourself and chart your own course.

Just for the record, we strongly advise against robbing a bank!

Start at the end: work out your retirement income needs

We’ve looked at devising your investing plan before, and also how much you can eventually withdraw from a portfolio.

But before you get to that good stuff, you need to understand how far behind you are – and what investing success would look like.

When it comes to retirement, success mostly means meeting your annual spending requirements with a low risk of running out of money.

So you’ll want know how much you’ll need – realistically – to spend in your retirement years.

A good way to get a handle on this number is to track your current spending. Use that as a base to figure out your budget, adjusting as seems appropriate. For instance, fewer work suits in retirement, but more gardening magazines.

For a quick start though, see estimates from the likes of the Pensions and Lifetime Savings Association (PLSA) and Which magazine.

Here are the latest annual retirement income figures from the PLSA:

But for the purposes of a late-starter getting – well – started, ballpark figures will help you to zero-in on the scale of the challenge.

From there you can estimate the size of retirement pot you’ll need to generate your desired income – in conjunction with your State Pension – and so what shortfall you face, especially as a later starter.

You can always further refine your numbers as you go.

Sensible ways to get your pension plans back on track

So you’re on the wrong side of those Sensible Sarah versus Spendy Samuel spreadsheets?

Let’s look at your main evasive action options, with links to further reading.

Save more

By far your best remedial action is to put much more of your salary into your retirement pot. Ideally in the most tax-advantaged way.

Every penny you save rather than spend today is more income for your future self.

Also, by getting used to a leaner household budget now, you may be happier making do with less when you do retire.

Crucially, your savings rate is one lever that’s mostly under your control – unlike say investment returns or how many healthy working years you have left.

Remember there are young FIRE-seekers who are targeting retirement in their 30s or early 40s by saving hard and investing.

To some extent you can flip that script, copying their tactics to catch-up late.

Another sure winner. Every year you stay in paid employment is (a) an extra year to put savings away, (b) another year for your pension pot to compound, and (c) one less year in retirement that your pension has to pay for.

Working for longer is probably not the most appealing prospect, but maybe you can make lemonade out of lemons and enjoy a late bloom at work? Or pivot to a second career?

Our final years in work are usually extra-valuable because earnings are higher at the end of our careers than at the start. (Though professional footballers and lap-dancers may need to pursue a different tack).

Normally we think it’s a good idea to save into both an ISA and a pension, given they are both tax-efficient wrappers.

That’s because money in an ISA is much more accessible – which can be a huge benefit if you need it.

But saving into a pension usually has a numerical edge due to tax-bracket arbitrage, salary sacrifice, and the tax-free lump sum you can withdraw on retirement.

As a late starter, ISA savings may be a luxury you can’t afford. Run the numbers to see if you’re better-off throwing everything you can into your pension in your precious remaining work years.

Maximise your employer’s pension match Your employer is obligated to chip in 3% of your qualifying earnings into your pension under the workplace pension rules. You must contribute 5% of your earnings (though this will cost you less in take home pay terms, after tax relief) for a total minimum contribution of 8%. Some employers are more generous though, and will match further contributions you make up to some limit. This is effectively a hike to your salary, albeit a pay raise that you must put into your pension. Contribution matching is an unbeatably cost-effective way to turbo-charge your savings rate, so you should almost always try to maximise your employer’s contributions. (Ideally via salary sacrifice).

Locking more money away for decades probably won’t come easy if you’ve been a spender all your life.

At least as an oldie you’re closer to the age where you’re allowed to get your hands on the money again…

“Earn more money so I can save more money. Why didn’t I think of that?”

Understood. But it’s worth a second reminder that how much you can feed into the hopper of your retirement investing engine is what will largely determine what you can spend in retirement.

Maybe you planned to coast as a team leader rather than pushing hard to become a department head?

Or to stay in a steady public sector job, rather than following your former colleagues into the tougher but more lucrative private sector?

Obviously I don’t know your work situation. The permutations are endless.

My point is just that easing up and retiring early isn’t on the horizon for you. So maybe knuckle down and work harder instead?

Think of it as the bill coming due for all that spending you did 20 years ago…

Okay, we’re heading into more controversial territory. But if you can stomach the extra volatility, then it might be worth running your portfolio a little hotter in the hope of bigger gains.

For example, instead of the industry standard 60/40 portfolio split between equities and bonds, perhaps you’d go 75/25 instead.

In theory, you can expect (but not be certain) to earn higher returns over the long term with a higher allocation to equities.

The price you’ll pay will be a bumpier ride – and the potential for unlikely but possible lower final returns. (Here’s how that could happen).

Remember: the market doesn’t care about your pension predicament nor your hopes for higher returns.

Markets will certainly crash from time to time – in the worst case right as you retire – so do keep the riskiness of your portfolio under review as you get older and your pot grows.

This is even riskier again, and definitely not for everyone.

But if you find yourself in your early 40s, say, with inadequate pension savings when your ‘What About My Retirement?’ lightbulb goes off, then gunning for expected equity returns of 6-10% (hopefully) and tax relief in a pension may make more sense than paying off mortgage debt costing you 5%, say.

There’s a panoply of options here, from choosing not to make overpayments on a traditional mortgage to switching to an interest-only option, to remortgaging to extend your mortgage term.

All these paths have downsides. Such risks are what ‘pays’ for the potential upside from getting more money growing in your pension for longer.

I’ve written a lot about these pros and cons before. And like I did then, I’ll stress again that paying down a mortgage ASAP is also a fine strategy – even for late starters. You can always go on a massive savings push once you’ve cleared the mortgage. Even if it’s not the financially optimal path, clearing your debts may be more motivational for you. That matters!

I’d certainly urge you to reject any other kind of debt when borrowing to invest.

Mortgages are low cost, they buy you somewhere to live, and they’re not marked-to-market, so you won’t face a sudden cash call during a stock market rout.

Other kinds of debt are much more expensive and/or risky.

Is amping up the conventional approach not moving the dial for you?

Have you left it so late – or are your ambitions are so big – that you need more money than 20 years of diligent plodding can possibly deliver?

Let’s run through a few more disruptive alternatives.

Keep working in retirement

Maybe you can’t hack the rat race anymore in your late 60s, but you could live with doing a few more years of lower-stress work?

So-called ‘BaristaFIRE’ involves earning a bit through the sweat of your brow or muscles to top-up the income from your retirement portfolio.

Like this you can survive with a smaller retirement portfolio.

It takes a six-figure capital sum to generate £3,000 to £6,000 a year in retirement (a wide band to reflect the vast range of starting points, end points, and all the rest).

So earning say £10,000 a year from part-time work can make up for a lot of missing invested money.

But I probably wouldn’t work at a coffee shop or similar, if I’d been a high-earner in my main career and money was my main BaristaFire motivation.

Most Monevator readers should instead pursue part-time or consulting work in the same vein as their lifelong profession. Doing so will maximise the kerching!-to-effort ratio.

I believe everyone has a passion, hobby, aptitude, spare bedroom, or the free time to make £5,000 to £20,000 a year to supplement their main income – without the risks of quitting work to start a business.

You may disagree, which is fine but is also perhaps why you’re behind on your retirement savings…

The truth is options abound and I can’t list them all here. Be creative, test and iterate, and back yourself.

The better pushback is that for a high-earner, it’s not worth messing around with side hustles for £10,000 a year when they are earning £100,000+ in their day job.

And I agree. Such people are probably better off getting promotions or doing more overtime.

But for the average earner on £35,000, say, the extra cashflow of £5,000 from a side-project can go straight to the bottom line to massively boost your pension savings.

Risky business

Of course if you want to make really big bucks then starting a proper business is one of the best ways. Perhaps the only way for most for us.

But that doesn’t mean it’s easy – or in fact less than unlikely or near-impossible. (Beware survivorship bias!)

The risks vary. If you’re trying to create a start-up software business, say, or to launch a restaurant, then your chances of success are low.

But if you’re an established architect wanting to set up your own practice doing what you already do and with an existing book of contacts, for example, then there’s surely less risk of outright failure.

Either way, your workload goes through the roof when you run your own business.

By all means be an entrepreneur if it’s your life goal. But I wouldn’t quit work to start a business to try to fix my pension pot.

Some active investors do beat the market. A handful even over the long-term.

Warren Buffett, I’m looking at you.

You’re not Warren Buffett and you haven’t got much chance of finding the next Buffett, either.

But if you can – or if you have edge yourself and so can pick your own stocks to beat the market – then by definition this will increase your long-term returns.

Perhaps there’s a case for investing into a few previously proven but out-of-favour active funds that might recover over the long-term, if you really want to roll the dice. Say with 25% of an otherwise passive equity allocation.

Examples as I write could be investment trusts like Scottish Mortgage, Finsbury Growth & Income, Pershing Square Holdings, and RIT Capital Partners. These funds have all compounded money very well over the long-term but are more or less in a funk right now. And they all sit on big discounts.

To be clear though, there’s zero guarantee that these or any other active funds will beat the market again in the future.

And needless to say you should not take my top-of-head list as any sort of investment advice. Do your own research!

Remember: you’ll probably do worse if you invest actively. You’re unlikely to beat the market and you’ll pay more in fees for trying.

But there’s always a chance… so onto the list it goes.

Some ways of making money sit between investing and running a business.

Moves like investing into a family or friend’s franchise business, running a multi-unit buy-to-let portfolio via a limited company, or reserving property off-plan in the hope of flipping it for a profit later.

These are idiosyncratic investments where the outcome will be about your aptitude – and luck – rather than what the S&P 500 does.

Again, possibilities abound. I’d suggest looking at areas close to your own professional expertise. You might have some kind of edge or insight there.

For example, if you’re a dentist then perhaps you know there’s a need for a new multi-practice building in your local area? You could be part of a consortium that gets it built and occupied.

There’s no end of other high risk, high reward ‘opportunities’ out there.

And yes – I’m lifting my fingers off the keyboard to put ‘opportunities’ into air quotes because one person’s reasoned speculation is another person’s reckless gamble. If not a borderline scam.

Into this bucket we might put everything from punting on cryptocurrencies to extreme concentration into just a few company stocks (putting it all into nVidia, say) to investing more than a small percentage of your net worth into a handful of private or crowdfunded start-ups.

I would define this category as anything where if a hundred of us have a stab, 90 of us will lose some or all our money – or at the least lag the market in the case of listed shares – but 5-10% might see huge returns.

So as the man once said: “Do you feel lucky, punk?”

Personally, I would again at most ring-fence a portion of my assets for such antics. Maybe a maximum 10% allocation.

That way if I did pick a winner it would meaningfully move the dial, but if – as is most likely – it goes tits up then I’m not too far further behind on my goals.

If you say “No way, not touching this stuff with a bargepole” then I can only applaud your good sense.

We all know other ways to get rich that aren’t written about on worthy websites like Monevator.

And as an upstanding citizen I don’t recommend any of them. Besides the moral issues, do you really want to risk your reputation or your liberty for the sake of a slightly comfier retirement?

Perhaps marrying rich is the exception. But I’m the wrong person to ask about marriage, as I see mostly risks…

For some of our regular readers, this post will have seemed like one long ‘obviously’.

Such people began saving and investing when they were very young maybe, or they’re on the other side of work already and enjoying the fruits of their labours.

Good for them!

However I do regularly hear from people with proper jobs and responsibilities who’ve no idea where they stand or what to do about their pensions – and they’re sometimes only ten to 20 years from retirement.

If that’s you, then don’t panic. Follow the links in this article, learn more, and begin to create your plan.

For most non-investment crazed would-be retirees, I’d suggest stick mostly (or entirely) to the sober tactics, with maybe an added side hustle.

Beyond that you could perhaps make a modest 5-10% allocation to a few out-of-favour trusts or to very carefully chosen long-shot bets in the hope – but not expectation – of faster gains.

I’m sure I’ve missed out a few possibilities above. Let me know in the comments below – and do tell us your story if you closed the gap in your retirement savings later in life yourself!

The UK government has exempted investment trusts from onerous cost disclosures in a move analysts believe will boost the £260bn industry and could support trusts’ share prices.

In a joint statement this week, the government and Financial Conduct Authority said investment trusts will be excluded from European regulation that affects how their charges are reported.

The rules on packaged retail and insurance-based investment products, or Priips, meant that investment trusts appeared more expensive than other types of financial product.

This is because institutions such as wealth managers and private banks would have to include the cost of investment trusts in their “ongoing charges figure” for clients, while shares and other types of investments were excluded from the fee.

Investment trusts were brought into the Priips regulation a decade ago. But this has deterred institutions from buying them due to having to report artificially higher costs, analysts said.

Will this tackle the wide discounts that have plagued trusts for the last couple of years?

It can only help.

But trusts have suffered from a pile-up of other problems too – not least the bear market for British shares since late 2021, and more widely all things not-Big-Tech.

Still, the industry seems ecstatic.

One manager, William MacLeod, compared the rule change to the Big Bang of the 1980s. MacLeod is quoted in This Is Money as saying:

“What’s happened today is a lot less dramatic than the big bang in the 80s, but for those of us in the sector and all investment company investors, it is no less seismic.

“It is momentous breakthrough that is long overdue.

he campaign group – helped immensely by the support and dedication of Baronesses Bowles and Altmann – has worked tirelessly for these changes for a number of years now and today is a day of both relief and celebration.

“Righting this wrong is profound for the UK market, the sector, and investors of all sizes.”

There’s plenty more jubilation where that came from, and elsewhere:

Christian Pittard, head of closed-end funds at abrdn, said:

“The new Government has made boosting economic growth – by channelling capital into areas like renewable energy and infrastructure– its raison d’etre.

“These funds already invest billions into these areas – delivering crucial economic growth projects.

“However, cost disclosure rules, which have amounted to a distortive ‘double counting’ of costs, have negatively impacted investor sentiment, therefore choking flows into investment trusts. They have been a key cause of these three lost years of infrastructure investment.”

Made in the UK

Most Monevator readers are (rightly) passive investors, so you may meet this excitement with a shrug.

But even if it doesn’t affect your investing directly, trusts are important for the British stock market – with their £260bn in assets representing 30% of the FTSE 250 index – and arguably for the UK economy, by funnelling capital towards infrastructure, renewables, property, and other investment.

Trusts still have 99 problems – everything from the shift to indexing and consolidation among wealth managers to recent poor returns – to overcome.

But at least cost disclosures now ain’t one.

As I wrote in Mogulsa while back, there’s seemingly value on offer with many investment trusts.

Some have since recovered, but many extra-wide discounts persist. Perhaps this move on disclosures will be a catalyst to reverse things?

Read the press release from the FCA (if you’re having trouble sleeping)

How to back Monevator versus the robots

Talking of hidden value, it’s been a while since I did a housekeeping note on our membership service.

Monevator member numbers are still inching higher.

But we do seem to have hit a newsletter industry-wide plateau that predicts a maximum percentage of free email subscribers will pay the minimum £3 a month we ask for.

Nevertheless, we’re still thrilled so many of you have signed up!

Which is why I want to remind members again that:

If you’re having any kind of log-in problems as a member, it will almost certainly be a cookies issue. Please clear your cookies (at least the Monevator ones) and make sure you allow third-party cookies. Also turn off ad-blocking for the Monevator website. Logged in members see an ad-free Monevator anyway! The cookies are needed for the software to show you member content. If you are fanatically opposed to all cookies, you can still read our member content via the emails…

…on which note if you’re not getting member emails despite being subscribed to free Monevator emails – and you’d like be emailed both – then please let me know in the comments below or use the contact form to tell me. There’s a couple of dozen members not getting member emails, and I can change that if I know who you are and what you want.

Rise of the robots

Again, please do consider signing up to at least our Mavens member tier if you’ve not already done so.

There’s more than a year’s worth of Mavens and Mogul articles ready for you to tuck into.

Meanwhile, Google is now inserting huge AI summaries at the top of all its search results in the UK.

This means Google gets to sell advertising to web searchers without those searchers ever seeing the work of the people who actually put the knowledge online.

It’s early days, but I could see us eventually paywalling the whole of Monevator.

Obviously as someone who has shepherded two to three free articles a week on to this website for the past 17 years, that’s the last thing I want to do.

Our whole modest mission was to do our bit for everyone’s financial savvy, as best we could.

But I’ll be damned if I’m going to slave to keep training a robot to parrot my stuff while Monevator visitors dwindle to zero.

It may ultimately be futile to resist the AI-era, but if it comes to it we’ll try writing only for the real flesh-and-blood people who value us most, not for a mega-corp’s bottom line.

Sorry for the downbeat note, which is hopefully over-pessimistic.

A few years ago I wrote about market efficiency and investing edge – and about how you don’t have it.

But let’s dig deeper into why this is true.

You often hear from retail punters and professional investors alike that passive (or index) investing makes markets less efficient.

Their argument is that this inefficiency is what justifies active management.

Well, they’re wrong – but not in the way you might think. The reality is more nuanced.

Let’s do a little maths to explain how passive investing actually makes life harder for active managers, not easier.

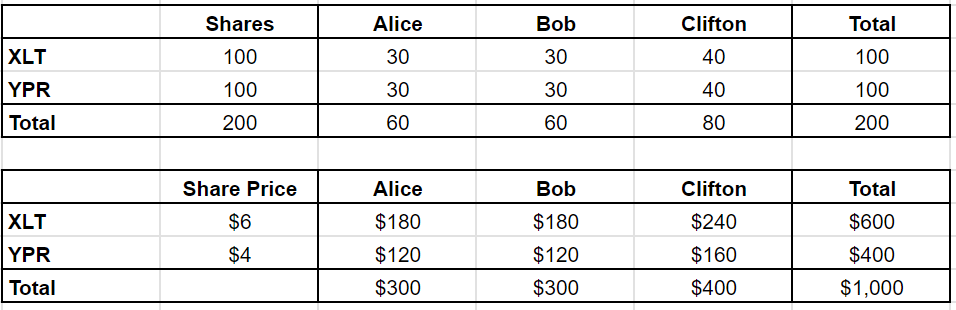

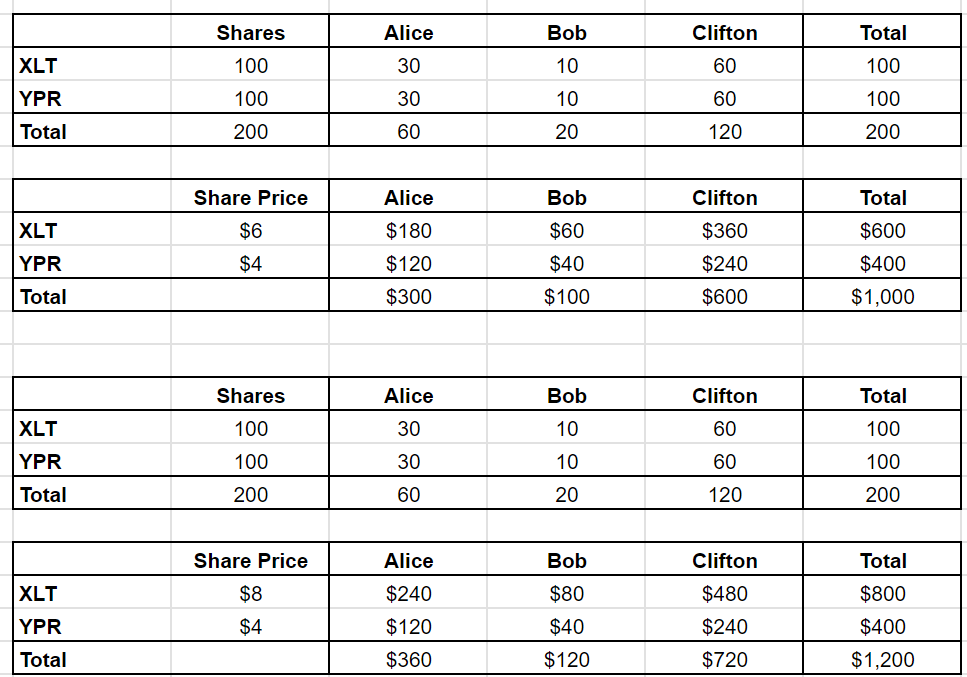

Model market: Alice, Bob, and Clifton

Imagine a market with two stocks, XLT and YPR, and three investors: Alice, Bob, and Clifton.

The total market capitalisation is $1,000.

Between them, Alice, Bob, and Clifton hold portfolios that add up to that $1,000.

There are no other companies and no other investors – we’re keeping things simple – but the ways in which this model is ‘wrong’ are not really material to the point today.

Alice and Bob each hold $300, while Clifton has $400.

XLT and YPR each have 100 shares outstanding, with XLT priced at $6 per share and YPR at $4.

(Yes, this is starting to sound like GCSE maths, but stay with me.)

In other words:

Now, Alice, Bob, and Clifton all hold market weight portfolios. This makes them passive investors by default.

Ideologically though, Clifton is your classic index fund investor – passive through and through.

Alice and Bob, on the other hand, are active traders. They are willing to take a punt if they sense an edge.

So this market is 40% passive (Clifton) and 60% active (Alice and Bob).

Dumb passive money?

One common misconception is that passive investors blindly ‘buy expensive stocks’ when prices rise.

Let’s expose this myth with an example.

XLT releases stellar results before the market open, and Alice decides she’s bullish. She calls Bob to buy some of his XLT stock, knowing that Clifton – the passive guy – basically does not trade. (Clifton doesn’t even bother going to the office till after lunch!)

Here’s how their conversation goes:

Ring, ring…

Alice:“Hey Bob, I’m in the market for XLT. What are you offering?”

Bob:“Hmm, I saw their results. Strong stuff. I’d have to start with an 8…”

Alice: “I was thinking more like $7.95.”

Bob:“LOL, nope. I’d buy from you at that price. $8.05 – final offer.”

Alice:“I’ll leave my bid on Quotron. Call me if you change your mind.”

Bob:“Catch you later.”

When Clifton finally gets into the office – sometime after his tennis match and a long lunch at the club – he logs onto his Quotron and sees that XLT has jumped 33% to $8.00.

A news headline reports: XLT Surges on Blowout Results – Light Volume.

Pleased with his morning’s ‘work’, Clifton updates his portfolio to reflect the new prices.

So note that nobody did any trading at all here. Alice and Bob just sort of agreed that $8 was a reasonable price for XLT, and so, by proxy, did Clifton.

This is how most price moves in the stock market happen. You don’t need trading to move prices.

The alpha chase

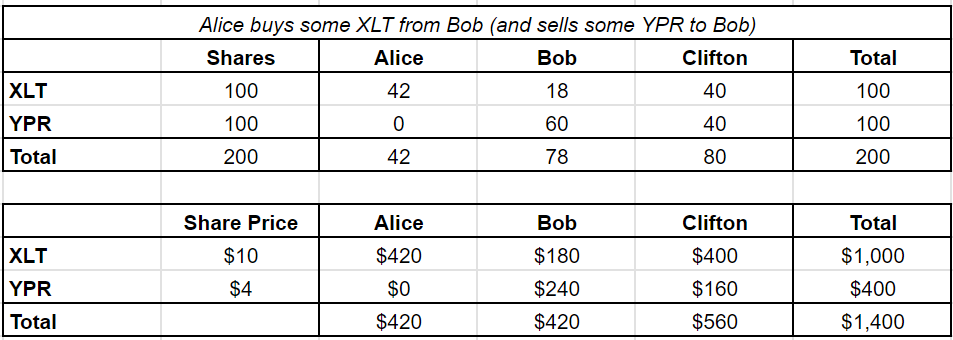

Fast-forward a few weeks, and Alice gets some inside info on XLT – let’s say from a friendly round of golf with its CEO. The company is about to secure a major government contract.

Alice tries again to buy from Bob, who smells something fishy. He agrees to sell her some XLT shares – but at an even higher price, $10 per share.

Since this is a closed system, Alice needs to sell YPR to raise the cash to buy XLT. And guess who she has to sell it to? Bob. They agree to swap their stakes.

Alice is now all-in on XLT, while Bob holds more YPR. (For convenience we’re ignoring that Bob would probably demand a discount on the YPR he’s buying, as well as a premium on the XLT he’s selling – Alice’s ‘market impact’).

Here’s a status check:

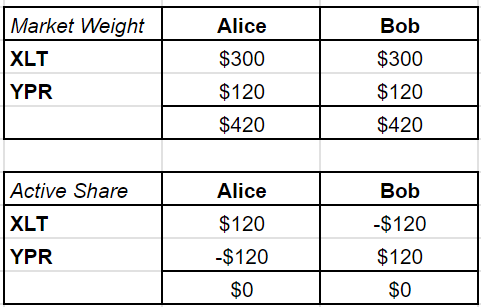

And here’s the kicker: for Alice to overweight XLT, Bob must underweight it. Clifton, as the passive investor, doesn’t change his positions at all.

This is a zero-sum game. Every dollar of ‘active share’ that Alice holds has to be offset by Bob’s:

None of this has changed their relative portfolio values – but it will.

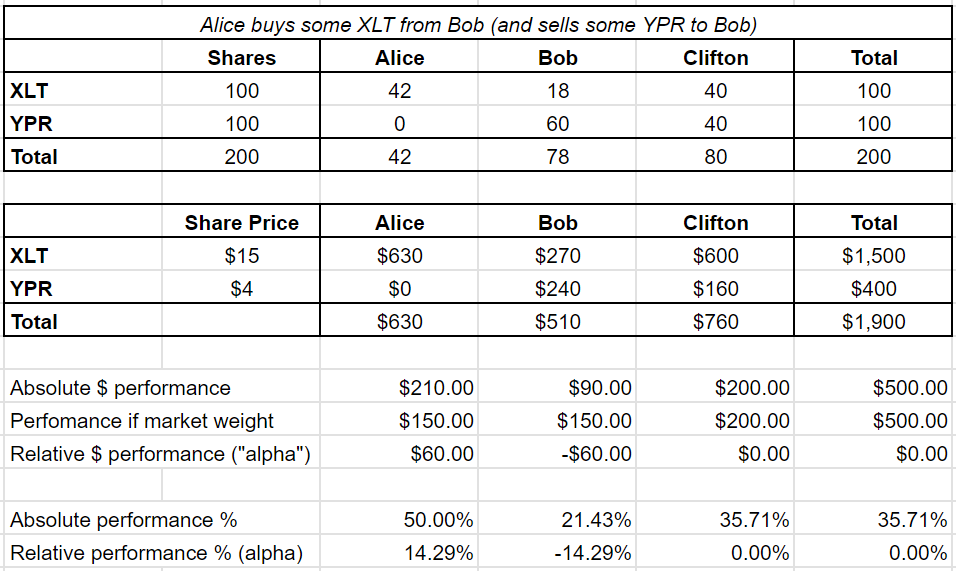

When XLT surges 50% on news of the contract, Alice makes a $60 profit.

But Bob? His loss is the exact mirror of Alice’s gain:

Since anyone can just buy the market, what matters for active investors is outperformance.

Alice’s outperformance (aka alpha or profit) of $60 is exactly offset by Bob’s underperformance of $60.

Bob still made money. Just less money than he would if he’d stayed market weight.

I know I keep making the same point, but it’s important: Alice can only make her $60 alpha at the expense of Bob.

Now let’s imagine that Clifton, our passive investor, controls more of the market than before.

Let’s say the market has shifted so Clifton now runs $600 of the total $1,000.

Meanwhile Bob only has $100 to manage while Alice’s capital stays the same at $300.

The passive share of the market has grown from 40% to 60%. Let’s re-run that first conversation between Alice and Bob that bumped up the price of XLT to $8, to see where it gets us.

Ring, ring…

So far, nothing changes. However when Alice returns from golf with XLT’s CEO and tries to buy more shares, things get trickier.

Bob doesn’t have enough shares to sell her all that she wants. Now Bob only has ten shares of XLT, priced at $10 each, for a total of $100.

Alice has $120 worth of YPR to sell, but she can’t buy as much XLT as she would have liked:

As passive investors like Clifton take up more market share, Alice’s strategy runs into a brick wall. She can’t go all-in on her insider tip because there aren’t enough active participants to trade with.

And that’s a major problem for her alpha.

In fact let’s check what it’s done to everyone’s alpha compared to our previous example of 40% passive market share:

It’s got worse for everyone except Clifton!

Alice’s alpha has reduced.

Bob’s negative alpha, in proportion to his capital, is now even worse.

Clifton doesn’t care either way.

The passive doom loop

Let’s imagine that Alice keeps getting lucky – or inside information – and Bob consistently underperforms.

Eventually, some of Bob’s investors will redeem their money. Diehard believers in the quest for outperformance, they would like to hand it to Alice – but they can’t.

Why not? Because Alice’s strategy is capacity-constrained.

Alice can only make money if she can trade against someone else, like Bob. But if Bob’s investors leave him and put their money into Alice’s fund, she’ll have fewer people to trade with – meaning she can’t deploy the capital effectively.

Bob’s redemptions have to flow to Clifton.

And so passive money grows, and active managers like Alice and Bob have ever fewer opportunities to beat the market. As passive share increases, active management becomes harder and harder.

It does not matter how good Alice’s inside information is. Her ability to monetise her edge is limited by the supply of suckers she can trade against.

This is where the so-called doom loop comes in.

As passive investing grows, active investing gets tougher, which drives more money to passive funds, which makes life even harder for active managers… and so on, in a vicious cycle.

Who’s Alice?

So, how do you spot a bad hedge fund?

Easy. They’re the ones willing to take your money.

The true hedge fund giants – names like RenTech, Citadel, and Millennium – won’t even let you invest.

Why? Because their alpha is capacity constrained.

These guys often can’t even compound their own money.

If you’re an investor with RenTech – which means you’d have to work there – it cuts you a cheque for the profits every quarter. You don’t get to leave the money in there compounding for the long-term.

Such funds have already soaked up all the market inefficiencies their strategy has unearthed.

They can’t let just anyone in – in fact they need suckers on the other side of their trades, so why not you.

Don’t be Bob

Finally – who is Bob?

Bob is anyone willing to underperform for long periods without having the money taken away.

For years, this was the underperforming active mutual fund manager.

Now? Increasingly, it’s retail investors.

Why do you think hedge funds, prop shops, and market makers will pay brokers to trade against their retail order flow?

*Cough* *cough* – I mean, provide ‘price improvement’ services!

Incidentally I hope our model market makes it obvious, if it wasn’t already, that Alice’s insider trading is not a ‘victimless crime’. She is taking money directly from Bob.[↩]