One of the most frequent questions I get on Twitter/X is: “Which investment platform do you use?”

I don’t really know why people ask this in a world where the excellent Monevator comparison table exists.

Disclosure: Links to platforms may be affiliate links, where we may earn a small commission. It doesn’t affect the price you pay nor how we judge the brokers.

However there are a few real-world issues that are out-of-scope for the table’s aggregated roundup.

So today I’m going to treat you to a tour of every investment platform (or ‘broker’) that I use and why.

Disclaimer: I will be stating my opinion based on experience. I do acknowledge though that I may have made mistakes, been misled, or that I could be confused about things. I’m happy to be corrected in the comments. None of this article is a recommendation to use (or a recommendation not to use) any particular investment platform. Brokers are also welcome to DM me for clarification. Especially if it means they’ll sort out some of the things I’m complaining about.

Behind the scenes at the Finumus family office

First off, why do we use more than one platform?

There are a couple of reasons:

- No one platform does everything we want

- We don’t want all our eggs in one basket:

I’ll only be discussing platforms that I have direct experience of using on a fairly frequent basis. These are:

- Hargreaves Lansdown

- AJ Bell

- Interactive Investor

- IWeb (essentially the same as Halifax Share Dealing)

- IG

- X-O (part of Jarvis)

- Interactive Brokers

Yes, that’s quite a lot of platforms. There used to be even more! Platforms we’ve previously used but that we no longer do include:

- iDealing

- Barclays

- Charles Stanley

I’ll let the reader draw their own conclusions from my change of heart.

Finally, when I say “we” I mean the Finumus ‘micro family office’. This is a portfolio of ISAs, SIPPs, and so on that I nominally manage holistically across three generations of our family, along with our Family Investment Company (‘FIC’).

Family linkage

Our micro family office set-up raises the first feature we like to see – some sort of ‘family linkage’ capability.

Both Hargreaves Lansdown and AJ Bell make a reasonable go at this. Account holders can nominate another account holder to manage the investments in their account. The managing account can then log in as themselves and flip to the other person’s account – without needing to share credentials – and without access to payment capabilities.

This is very useful to me for looking after the accounts of parents and children in a secure way.

Good as it is though, the family linkage is slightly hobbled. A prime example is that you can’t take any of the so-called Appropriateness Tests for things like complex products by proxy. Which is particularly annoying when you’re trying to rebalance into something that the investment platform has arbitrarily decided is ‘complex’.

You’re left having to phone Grandma to talk her through the test. If she’s on a six-week cruise at the time you can forget about it.

However, even when hobbled, these options are much preferable to those investment platforms that don’t offer this facility at all – which is every other one on my list.

Whatever the platforms’ reasoning for the lack of any family linkage, in the real world it leaves you having to insecurely share credentials – which is far from ideal – and in some cases having to call family members for a 2FA code every time you want to login.

Investment platform costs

We are less bothered about annual platform costs than we are that they should not scale with our AUM 2.

So we like fixed or capped costs.

All our accounts are already over the value where the cap is kicking in. For example, Hargreaves Lansdown charges 0.45%, capped at £45 p.a. 3 while AJ Bell charges 0.25% capped at £42 p.a. 4 (as long as you don’t hold funds). That’s just £45 and £42 respectively fixed, as far as we’re concerned.

All told, our annual platform costs range from £0 (XO, IWeb) to a couple of hundred pounds (at Interactive Investor – but that’s for an ISA and SIPP) per platform, per person.

I don’t have anything else to add on this subject beyond what you’ll find over at the Monevator comparison table.

Does your investment platform charge extra for funds?

Perhaps because the regulator banned kick-backs from the fund managers to the platforms, some of the latter seem to have decided it’s okay to replace the revenue by charging customers higher fees for funds.

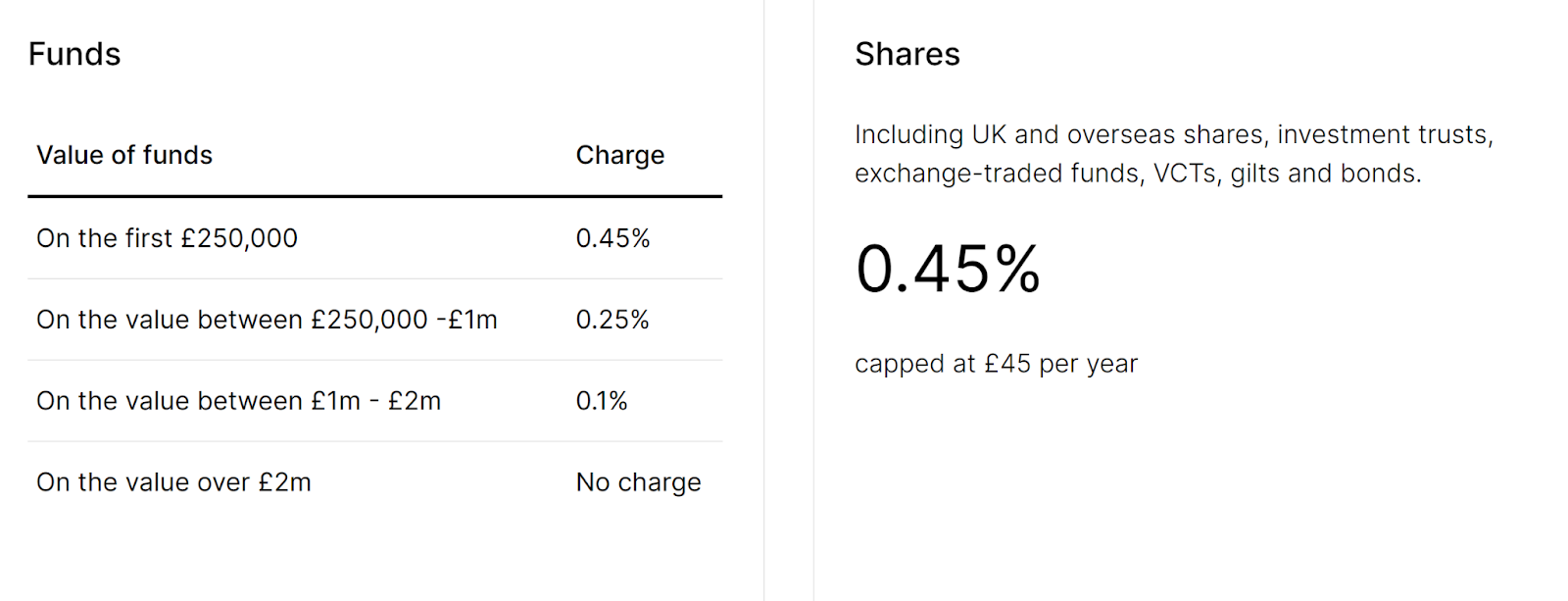

Here’s HL, for example:

Source: Hargreaves Lansdown

Right… Owning £2m of an ETF costs me £45 a year, but owning £2m of the same fund in an OEIC (Open-Ended Investment Company) costs me £4,000 a year.

What extra work is Hargreaves Lansdown doing to earn that £4,000? Absolutely nothing as far as I can tell – as evidenced by the fact that platforms like IWeb and Interactive Investor charge zero to hold that same fund.

Source: Dilbert

Because we don’t really believe in active management and there are equivalent-cost ETFs for nearly everything we want, we only own one OEIC type fund.

And – duh – obviously we hold it across the investment platforms that don’t charge extra for it.

Note that none of the above applies to ETFs. Even though they have ‘fund’ in the name, ETFs are treated as stocks on platforms that charge high fees for funds.

Dealing costs

We don’t trade particularly frequently, so we’re not very sensitive to dealing costs.

That said, Hargreaves Lansdown charging £12 a deal doesn’t feel very 2024 to be honest.

The £5 that IWeb charges seems more reasonable. It’s notable too that AJ Bell is reducing its dealing fees from £10 to £5 in April 2024.

Again, see the Monevator comparison table to stay across all this.

Foreign exchange (FX) fees

If you’re not careful, FX fees can really cost you.

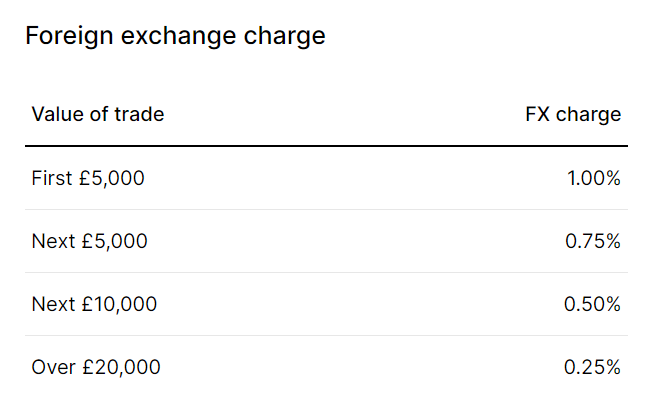

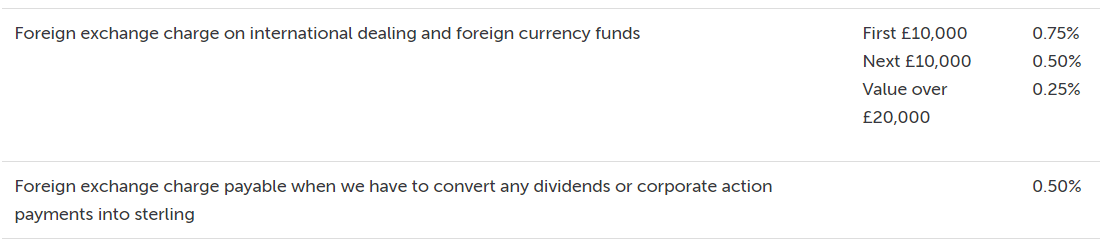

Here’s IWeb on the subject:

Source: IWeb

The example on IWeb’s website features a notably sub-sized £1,000 trade. Perhaps because 1.5% on a more sensible £5,000 – £75 versus £15 – would seem like quite a lot?

A shame, because IWeb is such good value on every other vector.

To illustrate how much of a problem high FX fees can be, let’s switch £100,000 worth of Microsoft stock into Apple. A trade which – given the liquidity of US markets – you’d expect to cost a few basis points.

Here’s the deal:

Generously, the platform doesn’t charge commission. So the switch will cost me a mere £2,977 – or 298 bps of the notional.

Maybe let’s not bother doing the trade after all, eh?

Costly foreign adventures

There are two problems with high costs for foreign exchange.

One is when the FX fees are high, obviously.

The other is when you have to settle everything into GBP 5. Our example switch above saw two rounds of FX pain, because we can only hold GBP cash in the account.

Now, in the case of ISAs, this is not the platforms’s fault. It’s what the ISA rules mandate.

But still, a platform doesn’t have to charge an FX spread you could drive a bus through.

In contrast, here’s the FX fee over at Interactive Brokers:

Source: Interactive Brokers

Interactive Brokers is a full 50 times cheaper than IWeb when it comes to FX fees.

Let’s math out that same switch in an Interactive Brokers ISA:

The trade costs us £63 (6.3 bps). Quite a lot less than £2,977.

Naturally, it’s still not good enough for me though. What I really want to do is keep the proceeds in the base currency of the instrument traded, usually USD 6. That way I don’t need to pay any FX fees when I switch between assets in the same currency. Why should I?

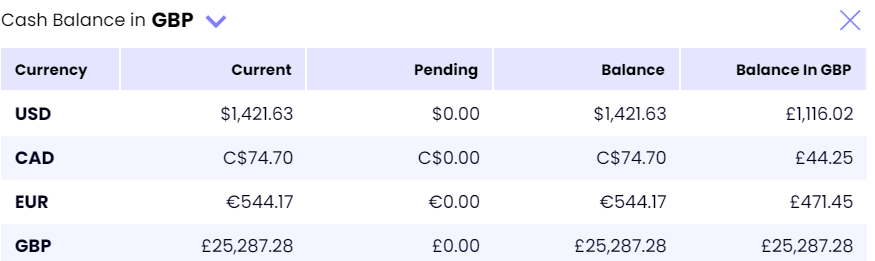

Outside of an ISA you can do exactly this with several platforms. But a grand total of two brokers in my list enable you to do this in a SIPP: Interactive Investor and Interactive Brokers.

Here are the current cash balances in my Interactive Investor SIPP:

See all those lovely hard currencies?

It’s something of a happy coincidence, because US stocks are best held in a SIPP. So this way you do not have to pay any dividend withholding tax on your US dividends, at least not with sensible platforms.

(In theory the withholding tax exemption should also apply to Canadian stocks. In practice it doesn’t.)

Both Hargreaves Lansdown and AJ Bell are big behemoths. They have the wherewithal to support multiple currency balances and settle trades in the instrument’s underlying currency within their SIPPs.

Yet they choose not to. I can’t imagine why?

Source: Hargreaves Lansdown

And for completeness:

Source: AJ Bell

Whose money is it anyway?

One way to avoid sneaky FX fees is to only buy ETFs for overseas exposure, and to always buy the GBP share class.

This way, your FX exchange happens inside the ETF wrapper at a much better rate / lower spread.

Since the underlying currency of most ETFs is naturally not Sterling, you should buy the Accumulation units to further reduce FX friction. Otherwise your dividends will be paid out in USD, which will then be FX-d into GBP at the platform’s spread and so bleed out another few bps of cost.

For instance, let’s say we wanted to track the MSCI World. We could buy the iShares Core MSCI World UCITS ETF USD (Acc) – whose base currency is USD – and specifically the GBP share class to avoid egregious FX fees:

Source: JustETF

Beware: a cunning trick sometimes deployed by platforms is to act like the GBP share class doesn’t exist.

You look up the ETF in its interface, you’ll only find the USD share class.

And when you complain, it’ll give you some blather about liquidity, or tell you that it “can only carry one share class of each ETF” – presumably because some numpty decided to use ISIN as the Primary Key in the investment platform’s product database.

Cock-up or conspiracy, limiting choice like this leaves you paying the platform’s FX fees.

Investment platform says “no”

Which instruments each platform allows you to trade and under what circumstances is both highly variable between platforms, inconsistent across time, and hard to predict in advance.

Something you bought yesterday, for example, might not be available to buy today. Likewise, something that was previously not deemed ‘complex’ now is. This changeability can make rebalancing very messy.

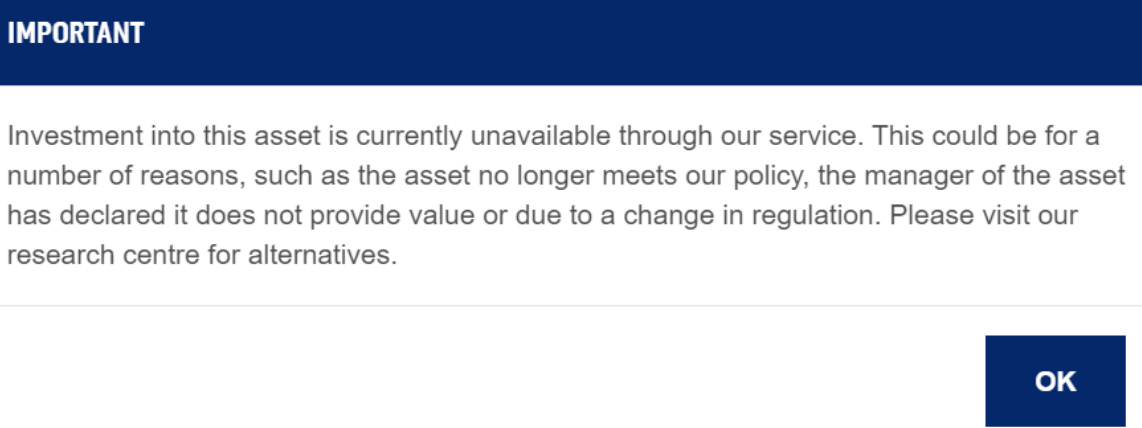

Let’s say you own some Blackstone Loan Financing (Ticker: BGLP.L) in your IWeb ISA, and you want to buy some more with the spare cash in there.

Bad luck:

Source: IWeb

Now what do you do? Well, you could sell a different stock in another ISA on another platform and buy back that same stock on IWeb. This way you free up cash in the other ISA to buy more BGLP with – but at the cost of you paying two lots of transaction costs and slippage en-route.

In theory you could transfer the cash from IWeb to the other platform, while sending the other stock across to IWeb (perhaps if you were worried about overall platform exposure). But in practice this takes weeks and can cost money so it is not really an option.

Rule changes can also leave you in a weird situation where you own this stock, but if you sell it, you won’t be allowed to buy it again – creating a random hysteresis function in your rebalancing decisions.

Low no-go

Arbitrary restrictions abound in the weeds on the investment platforms.

Another common one is to simply not support the lowest cost ETFs in a category.

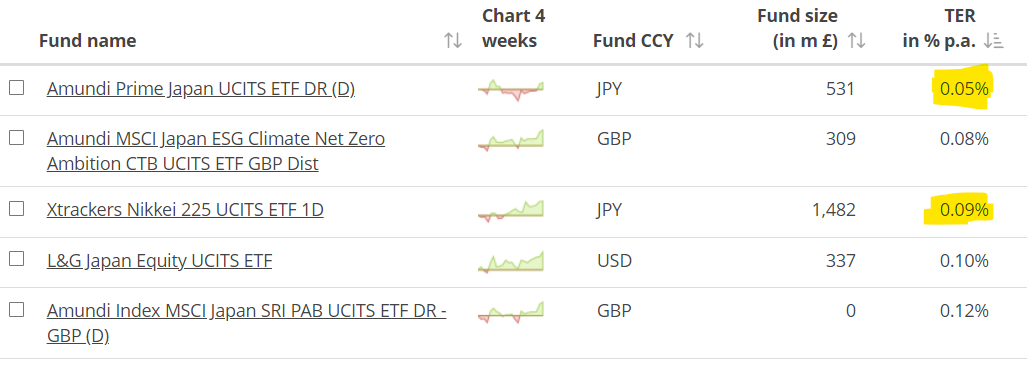

Want to increase your Japan weighting a little? A fairly normal process would be to go to JustETF, filter by ‘Japan’, sort by TER, and then buy the cheapest one:

Trackers gonna track, so the ETF we want is clearly the cheapest 5bps one from Amundi. Yet most brokers don’t carry it, and if I ask them to add it they won’t.

Hence I end up paying nearly twice as much (9bps) for the Xtrackers’ one.

Call me old-fashioned, but at the very least anyone who holds themselves out as any sort of stockbroker ought to offer dealing in any London listed security, at a bare minimum.

Another difficult area is leveraged ETFs, which many platforms just won’t go near.

And all this is before we even get to the shit show that are the regulations around Packaged Retail and Insurance-based Investment Products (PRIIPs):

Source: AJ Bell

The KIIDs are not alright

In short, PRIIPs is an EU rule that says you can’t buy US-listed ETFs.

We might have left the EU but – completely unsurprisingly – the one single EU rule that was a personal inconvenience to me has not been repealed, and hence most UK investors still can’t buy US listed ETFs.

This is a shame, because for US markets, US-listed ETFs are cheaper, better, more innovative, and (if held in a SIPP) highly tax-efficient.

In theory, if you are a high-net worth or professional investor you can opt out of PRIIPs and then be allowed to buy US-listed ETFs. This is your ‘MiFID status’ in the parlance.

In practice, the only broker that actually enables this is Interactive Brokers. (IG says it does but, in my experience anyway, it doesn’t work, in that it still won’t let you buy US-listed ETFs, at least not in an ISA).

Because the PRIIPs rules require the platform to have a KIIDs on file for every fund you want to buy this can even hobble buying London-listed stuff, if the broker doesn’t have its systems properly sorted.

There’s also some uncertainty as to what counts as a ‘fund’.

AJ Bell and Interactive Investors enable you to buy completely different sets of US-listed Business Development Corporations (BDCS) because they’ve each made completely different decisions about which ones are funds under PRIIPs.

Which seems a bit… random.

Margin lending

Our Family Investment Company’s account is held at Interactive Brokers. The major advantage of which is very competitive margin lending rates:

Source: Interactive Brokers

Since interest is tax-deductible for a FIC, we concentrate most of our leverage there.

The other brokers don’t support leveraged trading, aside from some white-labeled CFD offering perhaps.

IG obviously has CFD / spread betting. But given its high financing spreads, that’s not really an offering that appeals to me.

Flexible ISA

Why don’t more platforms offer flexible ISAs? IG is the only one (on my list) that does.

As a result I end up carrying higher balances with IG than I would otherwise like to, from a platform risk perspective.

Pet peeve #1: Interactive Investor

It’s a small thing, but a special groan for Interactive Investor for not being able to take SIPP platform charges directly from your SIPP, but rather making you pay them separately from your bank account.

Doing so likely increases your effective post-tax platform cost by between 25-67%, because you’re paying fees from outside the SIPP with post-tax money, rather than from inside with pre-tax money.

I’ve complained to the platform several times. Maybe some of you could complain too? It would cost Interactive Investor nothing and it would save us all a few quid from the tax man.

Pet peeve #2: Interactive Brokers

I have a bit of a soft spot for Interactive Brokers. It is great value and I have a SIPP, ISA, General Investment account and the FIC account over there.

The platform stands out for offering MIFID professional status, low FX fees, multi-currency accounts, and being able to trade Options (long-only in the SIPP) and futures (in a general trading account).

However, it is not all sweetness and light.

To start with, Interactive Brokers’ interface is something only a grizzled institutional equities trader from the 1990s could love. Your Nan won’t be using it to buy a few hundred shares of M&S. The learning curve is steep.

The other thing to note – for people who trade UK stocks – is that Interactive Brokers doesn’t have any Retail Service Providers (RSPs).

RSPs are the institutional traders who get you those ‘inside the spread’ and ‘price improvement’ prices that you see with other platforms.

Interactive Brokers basically only offers Direct Market Access (DMA). If you trade UK stocks, particularly mid caps, this may be a problem for you.

My overall view of the investment platforms

Source: Finumus ‘Vibes’, based on personal experience.

Right, let us know what you think in the comments below. And do check out the fine print in the Monevator broker comparison table for more on each platform.

If you enjoyed this, you can follow Finumus on Twitter or read his other articles for Monevator.

Useful article, thanks.

Would you / do you ever use any of the app-only newcomers, e.g. T212, Freetrade, Lightyear etc?

I think T212 is great at what it does, but I would be reluctant to put too much (e.g. a SIPP) in there.

Off topic a bit, but I quite like the LISA offered by Dodl, the AJ Bell app.

Separate

The point about II not taking fees from the SIPP has another angle too: for someone who has FIRED early (or isn’t working for any other reason), and cannot yet access their SIPP, paying it from their bank account increases their monthly living costs. If the fees could be paid from the SIPP then the cost, in effect, ‘vanishes’.

Nice!

On pet peeve #2 (IB), I was wondering recently why when I trade AIM shares with them, it’s so difficult to get a quick deal compared to HL…

Also with IB, they don’t allow OEIC / UTs right? (so e.g. can’t even buy Vanguard Lifestrategy… not that’d ‘d want to).

Just to clarify, if you get ‘MIFID professional status’ with IB, you can buy US listed ETFs in ISA/SIPP ?

Very useful article.

There a few corner cases where HL is cheaper than IBKR etc.:

HL doesn’t charge fees for Junior ISAs, so holding an index OEIC is very cheap for these accounts.

IBKR charge a proportional fee for U.K. stocks so for large GBP trades the flat HL fee is lower.

Thank you for the article. My biggest issues with Interactive Investor is lacking important features: 1. I would pay for producing a capital gain/loss statement for making my taxes easier, they have all the info and they can easily charge 100 pounds like SwissQuote charges 100 CHF to produce one. But they don’t offer this option. 2. Transaction history view and export into CSV lacks the data, like commission charged or spot price I can’t precisely remember, but it’s not possible to simply put it lets say to http://www.cgtcalculator.com to get it sorted, so it’s all over the place. 3. even downloading statements by naming everything is document makes a lot of manual labour.

I do like multi currency accounts, but not sure if you can actually withdraw in US dollars to avoid any conversion fees.

Their new interface also no longer shows loss/gain if you have multiple assets like US/GBP funds/shares, used to work sometime ago, and the mobile app is nice, however why not offer giving more info like factsheet links when looking at funds/etf? And yes, every feedback you send to them gets fully ignored.

I also have AJ Bell for SIPP, cause it was simpler to sign up than others and they support employer contributions (Vanguard doesn’t for example) it’s pretty simple and their team seems to be quite responsive.

I should really try Interactive Brokers, but since they not regulated in the UK, can this be a problem?

Overall, we have too many trading platforms here in the UK and none meet trust/quality of what US have as an example.

Thank you again for the article, very insightful.

This article is great, thanks Finumus!

This prompted me to check that the ETFs I hold are the GBP share class versions. InvestEngine claim to charge no FX fee on the basis that the only ETFs they list are the GBP versions; but then when clicking through their website to the linked Key Information Documents for HMWO and VWRL, these seem to be the USD versions. Have asked for clarification…

Interesting article, thanks.

A deeper dive into the platforms has been on my list to review for a while, currently have:

– ii for S&S ISA (majority is VG LS80 and some investment trusts)

– AJ Bell for SIPP (mostly funds)

– older HL account for smaller holdings in a LISA and another SIPP, all funds (and the one most up for review)

Partner holds a chunkier portfolio with Charles Stanley – who to me seem to charge a lot for not doing very much.

Mostly happy with ii for my main holdings, cheap, flat fees, just reduced trading fees, although wish they would do an easier way to display income, like HL do. Haven’t noticed too many negative changes since the Abrdn takeover, prehaps that is what they want!

Great write-up. I like IBKR as they tick most of the boxes. Also they offer a higher protection in case of a disaster (£500k) although I wouldn’t want to rely on it. Still, they’re huge well established, public company etc.

And yet they haven’t figured out how to pay REIT dividends without withholding 20% tax in an ISA or LTD company account. Which is embarrassing to say the least.

With all your abilities, can you please

1. lobby Interactive Brokers to make ISA Flexible?

2. UK Govt / FCA to allow retail traders to be able to trade US ETFs?

Some great insight there – thanks.

On pet peeve 1, have another bash at them. I’ve persuaded II to take the SIPP platform charge directly from GBP cash in my SIPP account. That said, I have no other accounts with them so perhaps that made my argument stronger.

I pay ii SIPP account fees (£12.99 a month) for the pension builder account (no ISA / GIA etc held) directly from SIPP cash to get the tax relief. I simply messaged them and they set it up.

Re. II:

ISA –> want to pay fees from bank account

SIPP –> want to pay fees from SIPP

Presumably they have a consistent fee model, rather than what is taxation-optimal for the customer. Is this why they charge in this way?

Is anyone using more than one platform to reduce platform risk? I personally use two platforms in case of complete platform failure (and I have no faith in FSCS scheme payouts on reasonable time scales), fraud, platform technical issues (if you want to trade/withdraw etc.). Just like I have more than one bank account…

@Algernond

“if you get ‘MIFID professional status’ with IB, you can buy US listed ETFs in ISA/SIPP?” – Yes. Although, ideally you’d want to hold them in an SIPP because of WHT

Thanks @Foxy Michael for pointing out the PID issue with IBKR.

@Genghis

Paying ii SIPP fees from SIPP – thanks – I’ll give it another try then!

Great article, thank you Finumus!

A few wrinkles/observations…

– SIPPs only are optimal for US stocks *that pay dividends*. That is not many of the ‘best’ US stocks in my book (!).

– IB does multi user access very well – you can specify what rights/access each user has – great for familys/FICs. This is its heritage – being something of a wholesale platform used by hedge funds / funds of funds / similar who then give their retail / end users access

– II SIPP fees – personally I like the fees NOT coming out of the tax sheltered funds – especially with ISAs – which enables cash to be reinvested to compound up tax free, instead of being squandered on fees – useful for those of us who are at our contribution limits. So I’m interested by your remonstrations to the contrary.

– Capital gains reporting. You don’t cover this, but platforms differ wildly on this. Many do NOT give you capital gains tax reporting at all. Sigh.

Good article, there are so many wrinkles…

Interactive Investors charge £40 for an ETF purchase of £100,000+

they deal in $ for what appears to a £ denominated ETF and is traded as such on HL (IBTS.L from iShares, that was a costly mistake on a buy and sell!!!)

Interactive Investors treat a crystallised and uncrystallised SIPP as one account and one set of fees versus HL where its two sets of fees, ( HL are generous and have removed most of the extra fees for SIPPs)

@Investor Geek –

“SIPPs only are optimal for US stocks” – yes of course, have I outed myself as a ‘value’ investor?

Thanks for pointing out that the IBKR multiple logins is basically the same as “family linking” – I’ve not really had cause to investigate this too much – it’s not like my mum is going to be using TWS!

Interesting article, thanks.

One thing I find annoying with HL is their management of cash in the separate Capital and Income accounts. Dividends drop into the Income account but they’re not available to invest, you have to push the money over manually to the Capital account or wait until they do the monthly transfer. Quite often I invest accumulated dividends and find cash lurking in the income account I overlooked – doh! The app doesn’t help you manage this either – it has to be a web login.

Also, the cash in the Income account doesn’t seem to attract any interest – if some big dividends drop you should transfer it to the Capital Account right away if you want to sit on it for a while, otherwise it can be up to a month with them pocketing all the interest – crafty! Not a big deal until the last year or so. Also I don’t get why their SIPP Drawdown account gets higher interest on cash. Maybe their interest rates on cash will improve after recent wrist-slapping exercises from the regulator?

Thanks for this article!

Can I ask which SIPP administrator you use with IBKR?

I’ve used AJ Bell since transferring from Halifax about 10 years ago. Although they were effectively the same platform AJ Bell charge less and have a better range of investment possibilities IMO.

I invest passively in UK shares and EFTs. In my view UK shares are a passive investment as after the dealing costs there are no other charges if the portfolio is over a certain value. Diversity is achieved by holding a wide range of shares. I tend to buy and hold to keep the charges down. I do tend to hang onto losers a bit to long.

Just as a follow up to my earlier comment 6, apparently KIID documents are usually published to the main share class of a fund and are not specific to a particular currency. It is therefore common to see USD as the main share share of an ETF hence why most KIIDs will be in USD; even though InvestEngine only offer the GBP versions.

@Robbo

Yes, I use atsipp.co.uk I’d be interested to hear of anyone using anyone else, I’d like to have more options.

Pet peeve with AJ Bell, Hargreaves… not allowing LISA transfers (as opposed to new accounts) over age 40.

This issue is affecting ever more people as time goes by. The system locks you in for years with one provider. I don’t think this is true of SIPPs or any other ISA type.

Interesting article, thanks.

I think it makes sense to split platform risk for the reasons the article and @Captain Underpants mentioned. The FSCS does little for ISAs and SIPPs because of the low limit, and only UK-domiciled funds are covered. So there’s a trade-off between higher fees for funds and some FSCS coverage.

I like AJB (SIPP) and iWeb (ISA) except for the Fx fees.

IB is a mixed bag in my experience. Very low fees, access to stuff that other platforms do not offer, and a very useful multicurrency account. On the other hand, the ISA is much more limited (no funds, no bonds, and obv no multicurrency); the system is labyrinthine and they have a knack for creating jargon-filled bureaucracy; and customer service is utterly useless.

Can anyone recommend another low-Fx ISA, mainly for foreign stocks? IG’s 0.5% fee is still quite high.

The advantage of paying SIPP fees from outside the SIPP is that if you are investing the maximum allowable, the full amount plus tax relief is available to invest – you are not losing a slice to fees. That said, a choice would be helpful, as HL offer.

@Robb0/Finumus

I have 2 DC pots a was thinking of moving them to II this year.

Is a SIPP administrator needed in Addition to II?

Thanks

@ramzez Sadly it is not possible for any broker to produce a capital gains statement. They would have to have knowledge of all your transactions which they don’t have because you might have holdings in other accounts. Also they won’t have details of transactions if you have transferred to them.

Thanks for the super clear/informative piece @Finumus.

It’s a game of snakes and ladders between what is and isn’t available on the different platforms and with trying to navigate the gamut of different charges and costs.

>”[ii] not being able to take SIPP platform charges directly from your SIPP, but… making you pay them separately from your bank account”<

SIPP with ii (moved from HL using the Monevator link), but ISA/GIA still with HL. Now slightly worried as how have I been paying the ii SIPP fees this past year? ii have one set of DD details for monthly SIPP contributions, and they’ve only ever taken those contributions using it, and have never used it to take any SIPP fees. Kinda just assumed that they would take the fees from the sliver of uninvested cash in the SIPP left in there for that very purpose. Better now check what they've actually being doing instead.

Good article, I currently use HL, AJ Bell, iWeb and IG. I also have a small position with InvestEngine, which I am trying out. They seem fine, my only concerns are with the HMRC kicking up a fuss over fractional shares and the fact that they seem too good to be true (no fees, no FX fees to convert dividends).

I have professional investor status with IG and have used the account to invest in a couple of US listed Vanguard ETFs (VTI and VOO). Cannot say I have experienced a problem, but it has been a few years since I last purchased. Just tried to set up a buy order all the way through to placing it and it looked OK. IG charge 0.5% FX fee which is a bit steep. The good thing about the ability to buy US listed ETFs is that you get a tax credit for the 15% US dividend withholding tax, which you cannot get with European listed ETFs.

If you can acquire professional investor status through IG then you also get improved terms for spread betting. Initial margin is much lower than with their standard account, eg 0.45% for index futures and options, 4.5% for ETFs. You can use ETFs and other investments to cover, subject to a haircut, this initial margin as well. Unfortunately, you do have to put up cash to cover variation margin and IG pay no interest on this cash. Fine when rates were right down, not so great right now. However, any gains from spread betting are tax free!

One thing not covered and hopefully not experienced too often is what happens when somebody dies. Some brokers will lock up an account until probate is obtained, which is not so good if you need to sell investments to pay IHT. If you don’t pay the IHT you cannot get probate. There is an option to delay paying IHT pending a property sale, but that does not apply to investments.

I have had to go through this a few times and have had the best experience with HL. On reporting a death they produce an Estate Application Pack. This is a document which values all investments in precisely the form that HMRC requires, including accrued interest on bonds and dividends for XD stocks due to be paid. They also provide the option of allowing investments to be sold to pay IHT (so you can get probate) and allow an ISA to be passed to a surviving spouse without having to sell everything and transfer as cash.

Something I have been meaning to do is find out what other brokers do when somebody dies. I did try to ask iWeb what they do, but getting correct and relevant information from them is like getting blood out of stone.

Has anyone else had experience with the way brokers handle customer deaths?

Ok. ii have been taking the monthly platform fee from the uninvested cash inside the SIPP wrapper. That’s great, especially as I’ve no record or recollection of asking them to.

For an alternative margin account you might want to look at Degiro. I have an account with them but have not used it for a few years. Margin works slightly differently with them. The standard margin rate for GBP is now 6.9%, but if pre-allocate a margin loan this is reduced to 5.25%. I cannot remember in detail how this works, but thought I would mention it for those interested in a margin account.

Degiro cover a range of investments, including futures and options. Fees are competetive as well. Much simpler than IB too.

Edit:found the help page on margin. Allocating margin and so getting the lower rate requires committing to the loan over longer periods. Looks as though you can only adjust monthly.

https://www.degiro.co.uk/helpdesk/money-transfers-and-handling/what-allocation-and-how-does-it-work

@syrio that simply is not true, swissquote provides one. I believe last time I asked AJ Bell also did. They only need to provide me with capital gain/losses for the account I have with them, it’s my accountants job to consolidate all of this. it’s the same story with interest/dividend tax certificate which they providing. It’s understandable not to provide one if they don’t know purchase price of course, but commonly I would think people didn’t transfer funds, but definitely should be available as additional charge.

also I quite like how other platforms show me how my portfolio performance over the years, I know I can use x-ray but somehow I have a feeling it doesn’t track transactions. either TWR or TWRR would be nice to have.

@ramzez, @syrio is totally correct. A broker cannot get your capital gains calculation right if you hold the same security across multiple accounts. Another source of error is with investments you have transferred from one broker to another (or between husband and wife). I don’t know what your accountant is doing, but you really should ask questions if he/she is just using broker statements.

Another thing brokers frequently get wrong is the handling of bond interest. All too often they overstate the interest because they fail to deduct accrued interest paid when the bonds were purchased (which could be in the previous tax year).

I completely ignore broker statements and work everything out from the trades and cash flows across accounts. Fortunately in our case, that doesn’t involve a lot of work.

Great post as usual.

Regarding FX costs within ISA, I think IBKR is even better than what your example shows, because the FX conversion bank to GBP happens at the end of the trading day, so if you sell one stock to buy another, the cash proceeds stay in USD in-between, and you only pay the 3bps once

Hi,

Do GBP versions of HMWO , VEVE pay out distributions in usd $?

(HMWO factsheet states ‘dividend currency USD$.’)

In which case the platform would presumably charge fx rates to pay out in GBP£?

Gary

FX fees: in what other industry would two identical items differ (and be allowed to differ) in price by 50 fold?

FX exchange is a fungible service.

At least at 0.45% p.a. for OEICs HL could try and claim it offers better service than say Vanguard at 0.15% p.a., but FX is FX is FX.

If I went to the supermarket and found a tin of beans at £1 and then next to it one of the same brand, size and expiry date at £50, I’d be pretty perplexed. Yet we seem to accept this in Financial Services. Why?

If it actually costs 3 bps each way on the main currency pairs, then platforms should be charging that, and not 150 bps.

BTW: the FCA has published proposals for an Overseas Funds Regime. I think that this might possibly end up superseding the pointless and self defeating PRIIPs regulations, which came in during 2018.

Basically, funds domiciled in those jurisdictions which the FCA deems to be functionally equivalent to the UK could then be marketed to retail UK investors.

The FCA has issued a consultation on this running until 12th Feb. Might be worth making views know to them as the PRIIPs needs to be reformed or removed.

The FCA announcement make no mention of foreign ETFs specifically though. Let’s hope that they’re included.

Thanks for another great article.

The Fidelity approach to fees is attractive: as I understand it, one cap of £90 per year across ISA and Sipp if you stick to ETFs and ITs

But I’m not sure whether their platform compares well to options like HL or AJ Bell on other criteria. Would be interested if anyone here has direct experience of using Fidelity

@Gary Cooper, “Do GBP versions of HMWO , VEVE pay out distributions in usd $?”

Yes, unfortunately they do and your broker converts them to GBP, unless you use a broker that allows multi-currency cash holdings. By far my biggest gripe with HL is the 1% they charge to convert ETF dividends. That charge costs us far more than their £200 SIPP fee. I put up with it because in all other respects I find them very good.

You can mitigate if you invest in accumulating ETFs, but our biggest positions are in US listed ETFs (for the withholding tax advantages), which all pay out dividends.

Great post.

Apart from a column in the Comparison Table the post is silent about X-O.

Is there anything else you wish to share?

The only thing I could think of was X-O is unlikely to ever be considered “too big to fail”.

Thanks.

FWIW I have been using x-o (among others) for a decade or so (first for my ISA and then also for my wife’s SIPP) without any issues. Perfect for what I wanted: no ongoing charges and low execution fees. A simple interface that hasn’t been updated since forever, but one that works as intended, and if you need help, someone always answers the phone.

There was only one inconsequential incident once: I bought something for ~£50,000, but they somehow mixed the pounds and pence and only deducted ~£500 from my cash. I waited a bit thinking it would be corrected, but it wasn’t by the end of the day, so I called to let them know, and then they corrected it. I’m pretty sure that it would have been corrected overnight anyway, but it may still be indicative of inadequate systems.

But again, that’s not really a complaint, I have been very happy with the platform.

@Al Cam

On x-o, as @Mp says, cheap, basic, responsive (regularly have to ask them to add ETFs, and they usually do it within an hour). I agree they are small enough-to-fail, we don’t keep enormous balance there.

Vanguards ISA is flexible.

I find it infuriating more S&S ISA’s are not flexible.

I’m leveraging a cash ISA and transfers for this purpose at the moment. I have a cash ISA primed in negative contribution territory ready for my annual bonus payment in March (house purchase hangover)

@BillD, one of the joys of life is doing a manual income sweep for my H-L SIPP. I usually beat the monthly automatic job to it, but that is due to the bad habit of logging in too often.

My whole portfolio is in distributing ETFs and Investment Trusts so I don’t find H-L fees to be too bad at all, miniscule with the cap once you have a half decent sized pot.

I usually reinvest manually any accumulated income on a quarterly basis into a single asset buy, but sometimes I get impatient so can’t last more than a month before wanting to put cash to work if it has been a particularly juicy month for dividends.

I do like the fact they at least pay some interest on cash. This means there wouldn’t be much cost to maintaining a 1 year cash bucket/buffer when in drawdown, and not worrying about lumpy dividend flows.

And maybe it should stop me overtrading in the meantime, knowing I am getting some interest on cash.

HL make no charge for holding shares in their Fund and Share account.

And apologies if someone has already mentioned this.

CSD allow me to hold and link multiple childrens’ accounts.

@Algernond

You can buy OEICs on Interactive Brokers per the mutual fund list on their website (which includes Vanguard Lifestrategy) for £4.95 per trade. There are no holding fees. The amount you can borrow against them for margin purposes is also more stable than for ETFs (where volatility is more readily observed).

@Naeclue

The fractional share issue was addressed in the latest Budget. “The government intends to permit certain fractional shares contracts as eligible ISA investments and will engage with stakeholders on implementation.”

@Haphazard

AJ Bell allows LISA transfers if you are older than 40.

One thing to note is that IWeb doesn’t charge their FX fee when receiving USD dividends, they only charge it when buying/selling securities in USD. That’s important when buying the GBP share class of an ETF that still pays dividends in USD. I don’t think they explain this anywhere on their website, I had to ask them to find out. I wonder if this is the case with any other broker too.

Great article Finumus and great points in the comments.

I managed to get Hargreaves Lansdown to reduce their fees on funds over a year ago. Whilst they are still expensive compared to other platforms, they changed the fund fees for me to 0.25% for up to £1m and free thereafter.

I know that Hargreaves Lansdown are expensive but I put some value in the quality of their mobile app / website and also that their call centre is UK based and manned by capable individuals. Personally my money feels safer with them.

@platformer – I’m curious if you have actually managed to buy mutual funds on IB?

I tried in my ISA. The funds comes up by ISIN search, but when placing an order an error message says “You do not have permissions to trade this contract. You can request permissions in account settings.”

Typically for IB, there isn’t actually any such option in the account settings.

Their customer service says funds aren’t available in the ISA. But they are generally clueless, so it may well be for another reason or a system bug.

Is it possible to deposit a paper share certificate to an ISA/SIPP in any of these providers ?

Would like to take benefit of direct “deposit” rather than a sale and invest.

I have Mrs V’s and my SIPPs with AJ Bell, and dealing and ISA accounts with iWeb.

Like Finumus I hold some funds and so pay a higher, uncapped charge, currently about £20/mth, to AJ Bell for these. A couple of months ago I wrote and asked them if they would mind capping the charges on Funds also, or I might move the SIPP. They replied saying that they could not, but that this is under review and I should “Watch This Space”. They also offered me £250 as a “loyalty” bonus to stay – and I have been with them for about 20 years – which I accepted as its terms require me to stay for 12 months, and the £250 will cover the charges over that period.

My SIPP is way over £85k and the counter-party does make me slightly nervous. Perhaps I will eventually move it to iWeb on the flimsy grounds that Lloyds is even less likely to be allowed to go tits than is AJ Bell …

@naeclue, @I_hate_fees .

Two different answers to my iweb fx fees on dividends .

@I_hate_fees trading 212 also charge fx fees for buying and selling, but not on dividends.

Gary

@platformer

As per @Sparschwein, IBKR also do not allow me to buy mutual / OIEC funds in my ISA.

Is it that we need to get the ‘MIFID professional status’ to be able to do it ?

@49/53

I have been able to buy funds but in a GIA outside an ISA. Not sure what their issue with funds in an ISA might be. You could check if you have completed the product suitability questionnaire for mutual funds. I’m not MIFID professional.

Whatever you do, do not use first direct. absolutely shambolic, we opened them up, as I had a few accounts already and was looking to diversify into a ‘too big too fail product’.

The interface is appalling, you can’t buy any funds and most crucially, I’ve been finding out over the last few days that you can’t search back more than 12m for a trade.

This means that if you want to go back through your records, you need to pay £15 per quarter for them to send you a new statement. Shockingly bad.

@Sundar, “Is it possible to deposit a paper share certificate to an ISA/SIPP in any of these providers?”

Not with SIPPs, but I believe it is still possible in limited cases with ISAs. The shares must be newly issued shares and there is a strict time limit to transfer the shares. The option does not apply to shares bought in the secondary market. Back in the privatisation days this was used a lot to get privatisation shares into PEPs (predecessor of ISAs).

Otherwise, the best you can do is a “Bed and ISA” or “Bed and SIPP”. These are services offered by some brokers to sell and then rebuy the shares in a ISA/SIPP. Initially the shares must be deposited into a general stocks and shares account with the broker. It can work well, better than selling and rebuying manually. For example, I did a Bed and ISA with HL for about £20k of Mondi shares in an account I look after for a relative. HL only charged for one side of the deal (£11.95) and there was no spread between the buying and selling prices. I was still charged stamp duty on the buy side though and £1 P.T.M Levy each side. The way HL do Bed and ISA transfers mean you end up with less shares in the ISA than you started with, 1531 in my case compared with 1541, but this is still better than doing a manual sell and buy, saving on trading fees and the spread. You don’t have to pre-fund the ISA either.

@Gary Cooper, I was under the impression that iWeb did charge to convert dividends, but I could and hope I am wrong. I will try to get an answer from iWeb on this.

Thanks for the helpful article.

Regarding your point: “One way to avoid sneaky FX fees is to only buy ETFs for overseas exposure, and to always buy the GBP share class.”

Isn’t this a currency exposure / hedging decision? I.e. The GBP class will be a hedged class whilst the dollar class will be an unhedged?

Your example seems to suggest so when I look it up.

Additionally I own VWRP.L for global unhedged exposure, and I didn’t think there was a GBP class unless I hedge it by buying something like IWDG.L.

Thanks

@DJBOND, “Isn’t this a currency exposure / hedging decision? I.e. The GBP class will be a hedged class whilst the dollar class will be an unhedged?”

The answer is no unless the ETF is currency hedged. Consider an investment in a S&P500 ETF, at $1.25 to the pound. Each share costing £1. The exchange rate moves to $1 tothe pound, but the S&P500 is unchanged. What happens to the price of the ETF? With perfect currency hedging the price will remain unchanged. It will be as though you were a dollar investor. For non-hedged though each £1 share got you $1.25 of underlying stock. Consequently the ETF price would rise to £1.25 because that is now how much each $1.25 of stock is worth when expressed in pounds. Let’s say instead that you bought an ETF with a share price of $1.25, so each £1 of investment would initially get you 1.25 shares. After the change in exchange rate, the shares would still be $1.25 each, but now that corresponds to £1.25. In other words, for unhedged ETFs it does not matter what the ETF shares are priced in, the outcome is the same when measured in pounds. However, if you buy the ETF with shares priced in pounds you do not lose out on FX fees charged by the broker.

@Finumus – thanks for the IBKR MIFID professional tip.

I got that now, and I see that I can buy US listed ETFs.

They still won’t let me buy the DBMF Trend Following replication ETF in my ISA though….. ’cause leverage!

@Finumus – message from Interactive Investor…

“You are welcome to pay fees from the cash balance in your SIPP – all you need to do is cancel your current Direct Debit. The quickest way you can do this is by contacting your bank/cancelling your Direct Debit through your banking app. Alternatively, you can let me know and I can get this cancelled for you. Once this has been registered as cancelled, we will attempt to take any future fee payments from the cash balance in your SIPP.”

Note that I only have a SIPP with them – so it is probably the case that if you have a SIPP/ISA then I suspect they’ll take the fees from the ISA.

@Algernond, don’t forget to check whether any US listed ETF you buy has UK reporting status, otherwise you will be liable for income tax on gains when you sell instead of capital gains tax.

You will find the list of reporting funds on th HMRC Web site.

https://www.gov.uk/government/publications/offshore-funds-list-of-reporting-funds

@Finimus,

Lots to think about here – a comment and a question already come to mind.

The comment is about all of the brokers being different in their SIPP withholding tax management. Over at the-international-investor.com they are pretty sure that AJ Bell and HL do the right thing and get it down to zero, but I’ve already found an iWeb comment about it still being 15% (and they have no foreign WHT reclaim service).

There’s an equivalent blunt comment I found eventually on ii (much too hard to find this!) :

”

For assets held in a Trading Account, you will be provided with an annual Consolidated Tax Certificate (CTC) summarises your UK and overseas income, and any tax on dividends and interest paid on shares for the period shown. You may be able to use this information as evidence to make your own application to the applicable tax authority to reclaim the difference between withheld rate and treaty rate.

No CTC is provided for assets held within a SIPP, ISA or Junior ISA. You will therefore be liable for all tax withheld at source and you may be unable to reclaim such tax from the relevant authority who required tax to be withheld.

”

I’m assuming here that the UK-US DTA means it would still only be 15%, but at least iWeb states this explicitly.

Similar info may be on all the others too, but I haven’t got to them yet! 🙂

The question is more straightforward. In your multi-currency dealings with ii, have you found a way to do any currency transfers without conversion to and from GBP. I’d far rather keep the currencies separate and do the FX myself.

Martin

An very informative article Finumus, thank you.

You wrote “Want to increase your Japan weighting a little? A fairly normal process would be to go to JustETF, filter by ‘Japan’, sort by TER, and then buy the cheapest one. Trackers gonna track, so the ETF we want is clearly the cheapest 5bps one from Amundi.”

You seem to suggest from this that cost is your main factor in choosing a tracker ETF. I’m not really that “au fait” with ETF’s but have been reading a little on them lately (including some of TA’s excellent posts) and they seem a bit more complex than just funds (unit trusts etc.) but many investing sites seem to suggest there are many factors to consider such as fund size, how close it tracks the index, how well established/big/safe the fund manager is, which index it tracks – as I understand MSCI/FTSE are the main ones and Solactive is newer but not generally considered as good as the others etc. etc.

So would you just always go with the cheapest whatever as this is the MOST important criteria or does JustETF consider these factors as well and only pick out the best of the bunch? (or does it bring up all of them – good/bad/indifferent?) I’ve not yet used JustETF myself. This is not a criticism of your methods at all – just intrigued how more experienced investors go about choosing them and what you consider important because finding the right ones on brokers websites that have all these attributes seems a bit of a swamp when you are trying to find a few decent ones (in my case global) and also an Accumulating version and whose trading currency is GBP to get around FX fees and domiciled Ireland considering WHT. Definitely more involved than investing in funds!

@Martin

They (AJB, HL, ii, IBKR) do get the US WHT right in the SIPPs. But they don’t get any other countries right. For example Canadian Dividend WHT should be 0% in the SIPP under the tax treaty, they all charge 15%. South Africa should be ~10% for UK (regardless of wrapper), but they all withhold at ~20%.

Personally I don’t know why there isn’t more fuss about this, the tax treaty, which is the law, says one thing, and brokers just shrug steal your money.

I’ve not found a way to avoid ii FX fees in my SIPP. Sorry.

@InVest & Pants

I focused on fees for the sake of brevity, and it’s the most important thing for me. But it’s certainly not the only consideration, the others you point out are all reasonable ones to consider

@platformer

> You can buy OEICs on Interactive Brokers

well, when I tried to search for Vanguard Lifestrategy 80% on Interactive Brokers with its ISIN code “GB00B4PQW151”, it does find it but does not let me buy it. It says it is “limited to professional investor only”… 🙁

Something to add to the article (and others dealing with broker comparison): Incredibly, on Interactive Brokers (IBKR),

I need a minimum notional of £1,000,000 to buy into the HSBC FTSE ALL WORLD INDEX HSBC UK fund of ISIN = GB00BMJJJG09.

Confirmed by IBKR live chat customer support who said they couldn’t do anything because it’s a minimum set by HSBC for this fund.

Nowhere in the public IBKR web site was indicated anywhere that there were such high minimum requirements for purchase of that fund.

This the income version of the HSBC tracker recommended at https://monevator.com/low-cost-index-trackers/ , which

says to [ignore] “an eye-watering minimum purchase figure (such as £100,000) to buy into a fund.”

Apparently IBKR didn’t read the Monevator article! Ahem…

I’m guessing IBKR is not much interested in fund trades since they make their money via %-based commission on exchange-traded products

and shares. It could be related to what the article says: “Interactive Brokers doesn’t have any Retail Service Providers (RSPs).”

Which would explain why an IBKR client such as myself, for purpose of buying a fund, would be seen as an institutional investor.

Context: I opened an account with Interactive Brokers ie IBKR to manage broker risk (I already trade on Interactive Investor ie II,

and my employer won’t let me just chose any broker for personal trading – IBKR was one of the only low-cost choices).

I suppose I could do purchases in II then transfer to IBKR but what a pain (also I am not confident in transfers retaining

book cost / cost basis information).