This article on the pros and cons of a Family Investment Company covers some nuanced issues around accounting and tax. It will not be relevant to the finances of 99%+ of readers – though we expect many more of you will find it interesting, and anyway we want the 99% to understand what the 1% are up to. The article is certainly not personal guidance. You should not act on ANYTHING in this post without seeking professional advice. This article is for entertainment purposes only.

Can you avoid dividend tax by investing through a limited company – specifically by investing via what’s sometimes called a Family Investment Company (FIC)?

And with the pending cut in the dividend allowance to £500, is it worth setting one up, pronto?

I’ve been running a Family Investment Company for nearly 20 years. In that time I’ve made many mistakes, and been asked many questions about the structure.

Today I’m going to answer (nearly) all of them.

It’s a long one. Grab a coffee. Maybe pack some sandwiches.

Family Investment Company 101

Here’s a somewhat idealised scenario for a potential Family Investment Company owner:

- You’re an additional rate taxpayer and you expect to remain so for the foreseeable.

- You have a £1m portfolio of dividend-paying equities held outside any tax shelters. 1

- Your £1m portfolio yields 5%.

- That’s £50,000 a year of dividend income.

There currently exists a £2,000 dividend allowance (falling to £500 soon). At the additional rate tax band you pay a 39.35% dividend tax rate.

- (£50,000 – £2,000 allowance) * 39.35% = £18,888.

Subtracting that tax from your £50,000 of dividends leaves you with £31,112.

Why is this portfolio so exposed to tax?

In this scenario you’ve already used up all the other tax-efficient wheezes.

You already fill you and your spouse’s ISAs every year. You’re both over the Lifetime Allowance (LTA) in your pensions. You’ve paid off the mortgage. You’ve maxed out the kids JISAs. You have £50,000 worth of premium bonds each. You’ve realised VCTs are a rip off…

…you get the idea! You’re out of options for sheltering your investment income.

If you do have any of these other options left, then you can stop reading right now. A Family Investment Company is going to be much more hassle.

However if you are out of alternatives, then you could use a limited company to defer – and perhaps avoid that dividend tax.

But before we dig into how it works, there’s a couple of things you need to be familiar with.

UK corporation tax for limited companies

UK companies pay corporation tax (CT) on their profits (at 19%) and pay dividends to their shareholders after tax.

Corporation tax is rising to 25% in April 2023 (to pay for Brexit). But that doesn’t matter for us from a FIC perspective, because our limited company doesn’t intend to ever pay it.

Companies don’t have to pay corporation tax on dividends that they receive from their shareholding in other companies.

Why? Because the company that made the profits has already paid the corporation tax. The exemption avoids double taxation.

Realised capital gains on those shareholdings, however, are taxable at the corporation tax rate. And this has serious implications that we’ll come to later.

Directors’ loans

Directors can lend money to their company. If there’s no interest charged on the loan – and as long as the company owes the director money 2 – then there are essentially no tax consequences, for either the director or the company.

By simply keeping a spreadsheet of loans and repayments, you can just wire money in and out of your limited company.

That’s all the tools we need to make the Family Investment Company route potentially attractive.

Enter the Family Investment Company

In our stylized example:

- We set up the FIC with, say, £1 of share capital and ourselves as sole director.

- The company is furnished with banking and brokerage accounts.

- We lend the company £1m.

- And then transfer that £1m to the company brokerage account.

- We buy a magical share that pays out a 5% dividend yield and has absolutely no price volatility. (Let me know if you find one!)

- Every year the company receives £50,000 of dividends and uses that cash to repay the directors loan.

The cash flows look like this (with costs ignored for clarity):

Your company receives £50,000 a year in dividends (tax-free), and uses the full £50,000 to repay the director’s loan. You therefore receive £50,000 per annum from your £1m invested instead of £31,160. Saving yourself £18,888 per year – or £377,760 over 20 years – of tax.

(I ignored the change in dividend allowance, again, for simplicity).

Getting the million back… after tax

At the end of 20 years – with the director’s loan having been paid off with the dividends – you’d obviously like your £1m back, please.

How do you do that?

The company sells its shares (for zero profit, so no corporation tax), and pays out the £1m cash as a dividend. On which, of course, you need to pay 39.35% dividend tax, so approximately £393,500.

Hence you’ve not actually avoided any tax at all! (Nor mitigated tax, which is a better way to think these days).

We didn’t even include the various costs to pay. In fact we seem to have gone to a great deal of trouble to simply enrich our accountant.

And this is the main objection to this structure. Because whatever you may have heard, a Family Investment Company does not necessarily avoid dividend tax at all, but merely defers it.

Is deferral useful? Well… it depends.

My Family Investment Company

Let’s move beyond our stylized example, and get down to the nitty gritty.

But first an important reminder and disclaimer:

Wealth Warning You should not act on ANYTHING in this post without seeking professional advice. This post is for entertainment purposes only.

What’s the point of deferring tax?

Once money is gone it’s gone. Obviously I’d rather avoid the tax altogether, but I’ll take deferral if that’s the only option.

The Family Investment Company structure essentially enables me to choose the timing of the tax incidence of the dividends. And the FIC decides to pay me dividends when I’m paying the 8.75% rate, rather than the 39.35% rate.

I’ve enjoyed a feast-or-famine career – years when I’ve earned a great deal of money, and years when I’ve earned nothing at all. Dividend payments from the FIC can be stuffed into the lean years.

I have no DB pensions (sadly), so I can control the timing of withdrawals from my SIPPs. There will potentially be years in retirement when I can engineer being a lower-rate taxpayer.

Unfortunately, obvious wheezes like moving abroad for a year don’t work – there’s a specific anti-avoidance rule for ‘close companies’ in this situation.

Winding up the FIC at CGT rates may be possible. But I’ve never done it, so can’t attest to the process.

What if taxes go up?

You can certainly make a reasonable argument that deferral is bad – because taxes in the future will be higher than they are now.

My personal experience is taxes only ever go up. The dividend allowance cut itself is a case in point.

- Allowances are cut, or withered away by inflation, or ‘tapered’, or ‘withdrawn’.

- Reliefs are removed, restricted, or ‘means-tested’.

- Lifetime ‘Allowances’ are introduced, where before you didn’t need to be ‘allowed’ at all.

- Taxes are ‘simplified’ in a supposedly neutral way, and then the motivation is quietly forgotten and rates ratcheted up a few years later.

- The indexation allowance is removed because we no longer have inflation.

And so on. It only ever gets worse.

Given that the only escape from this is economic growth – something both the UK government and the opposition now appear to be ideologically opposed to – there’s every reason to expect taxes to continue to rise. Indefinitely.

In which case you’d be better off paying taxes now rather than later. And not bothering with a FIC.

How is my Family Investment Company structured?

I’m the sole director. My wife is the company secretary. I own about 30% of the shares. My wife 25%, my children the remaining. My wife and I therefore control the company.

One of my kids is an adult, the other is not.

We have ‘Alphabet’ share classes. Different individuals own different mixes of share classes.

There is some flexibility around paying different levels of dividends on different classes. Lower tax-rate shareholders may happen to enjoy larger dividends than other shareholders. This is slightly complex to set up and the consequences of getting it wrong can be severe, but it does provide some flexibility.

For example, family members may be having a career break, or be in full-time education.

We didn’t pay dividends to non-adult children though. In the opinion of my accountant, this is generally treated as parental income for tax purposes.

How does a FIC compare with setting up a trust?

I’ve no idea. I Googled around a bit and I didn’t think there was much in the way of tax benefits to trusts. That seems to be more about control of assets.

I would say that the directors of a company, if the articles are drafted properly, have a great deal of flexibility to do whatever they like with respect to taking risk. That would not necessarily be appropriate in a trust where there are fiduciary duties.

Does the FIC open up inheritance tax (IHT) options then?

Not obviously. Unfortunately shares in the FIC don’t qualify for IHT Business Property Relief.

Also – and inconveniently – gifting shares in the FIC is a disposal for the giver and are therefore subject to capital gains tax (CGT). Especially inconvenient with the CGT allowance also being cut soon.

My accountant is happy with the value of the shares being the proportional NAV of the FIC at the time, for CGT purposes. So you can do this early on, before the company has accrued much value. But giving away more than 50% potentially introduces control issues.

And don’t be thinking you can just fiddle with the rights associated with each share class to make the kids shares ‘worth’ more. The tax man will see straight through this.

There’s nothing to stop you setting up a second Family Investment Company and giving 49% of the shares to your kids on day one. But then you’re doubling your admin and costs.

Our (loosely held) plan is that once the next generation are proper adults, we (or perhaps grandparents) can subscribe for shares, at NAV effectively, and gift them immediately to the (grand) kids. These are a Potentially Exempt Transfer (PET) under the IHT rules

Our intent is to do enough of this to pass majority control to them during our lifetime. We’ll then leave the minority shareholding to the generation after in our wills. (Yes, subject to IHT).

Someone has suggested holding the FIC shares in a trust… but my head hurts already.

I personally would prefer to just live forever.

Which broker do you use?

Most brokers offer a company or corporate account. We use Interactive Brokers (IBKR).

Why do we use IBKR?

Cheap margin loans. As any Private Equity associate will tell you, debt interest is tax deductible for companies. So if you’re going to apply leverage anywhere in your portfolio then the FIC is by far the best place to do it.

There was a good decade when my FIC was borrowing money from IBKR at about 2% (tax deductible), and repaying my directors loan so that I could use it to offset my mortgage (costing about 3%, not tax deductible).

You probably shouldn’t have one of these structures if you still have a mortgage though.

If you think Interactive Brokers is for you, then please DM me on Twitter for an affiliate link.

How much leverage do you use?

Lots! Between 50-100%. (Where 100% means the FIC owns £100 of stocks for every £50 of capital)

When interest rates were very low – and the interest is an allowable expense to offset against capital gains – why would you not run it hot?

How do I manage the leverage?

In theory the size of the margin loan never exceeds cash that I could feasibly access at close to zero notice and lend to the FIC as a director’s loan. We keep an effectively un-drawn offset mortgage against our Principal Primary Residence (PPR) for just this purpose.

In reality this rule has been ‘passively breached’ on one occasion, when I had to draw down the entire mortgage at the peak of the COVID slump. That was, as they say, ‘squeaky bum’ time.

(For quants-only: I also ensure that there are always sufficient available free funds in the brokerage account to cover the max of the parametric and historical two-day 99.9% Expected Shortfall.)

We’re reducing leverage now that interest rates have risen.

Which bank do you use?

Pretty much all banks offer a business account. Turn up with your incorporation documents and ID, and you should be good to go.

I’ve heard from others that banks don’t like FICs. I’m not sure why this would be, or what would cause the problem. It’s not something I’ve experienced.

If you’re only used to personal banking, then you might be annoyed to learn they could expect you to pay for things.

We use a Santander business account and don’t pay any fees, I guess because we don’t do the things you might pay fees for. (Paying in cash would be an example).

This was not an active choice. We used to use Abbey National, and it merged. Possibly our free account was grandfathered in.

What stocks do you own in the FIC?

This is my most favourite question, because anyone familiar with my stock picking skills would think I was the best person in the world to answer this question.

We’re looking for stocks that don’t go up – something I do appear to be an expert on!

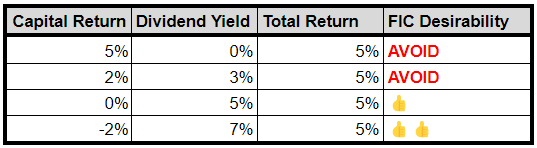

Actually, we’re looking for stocks where most, if not all, or even better, more than all, the returns come from dividends.

This is because dividends are tax-free to the FIC and capital gains are not. So we want lots of dividends and the minimum capital gains – or even capital losses.

For example, all the assets below deliver the same returns, but the tax consequences are very different. (RIP Modigliani & Miller).

Stocks with high yields that never seem to go anywhere are what we want.

Why do you want to generate capital losses?

The FIC pays corporation tax on any realised capital gains, although we can offset expenses and losses.

Effectively we try to avoid ever paying corporation tax by ‘sterilising’ gains. That is, by only realising them if we have sufficient offsetting losses in some other stock, or running costs.

For this reason we want a portfolio of stocks and not just a high-yield dividend-focused ETF like Vanguard’s VHYL, for example. We’re after some dispersion of returns.

This does still lead to some shareholdings being sufficiently ‘in-the-money’ that it’s hard to have the tax capacity to sell them.

When you see the portfolio in a minute, there’s some stuff that’s been held for a very long time for this reason that is no longer particularly high yield.

Any other constraints on potential stocks?

Yes. It’s very important that the dividends are actually tax free to the FIC. There are some specific examples of cases where they are not. The source of the stock has to be a ‘qualifying territory’ on this list.

Tempted to stuff the FIC full of London-listed infrastructure or renewables trusts? Large capitalisation, high-yield, low volatility – perfect, right?

I’m afraid not. They are pretty much all domiciled in Jersey or Guernsey, and guess what? The Channel Islands are not on the list.

But most proper countries are, including, importantly, Ireland (where most LSE-listed ETFs are domiciled) and the US, with over 50% of global stock market capitalization.

However, and I’m sorry about this, but we need to talk about dividend withholding tax before we go any further.

A word about dividend withholding tax (WHT)

Explaining dividend withholding tax fully is beyond the scope of this post.

But in summary…

Most countries level a withholding tax on dividends. This means you don’t get the dividends ‘gross’. You get them ‘net’ of withholding tax.

For example, the Netherlands WHT rate is 15%, so if a Dutch company pays a €1.00 dividend, you will receive €0.85.

As an individual UK taxpayer you may be able to use the 15% as a credit against any dividend tax you owe in the UK. But as a limited company we can’t, because we don’t pay (UK corporation) tax on dividends anyway.

In theory, the tax treaty may say we can get a reduced rate. But good luck getting your broker to take any interest in that. “Sorry they are held in ‘street’ name”.

You could also ask the foreign tax man for the money back. Good luck with that, too. “Sorry, your broker shouldn’t have withheld the tax in the first place”.

So what does WHT mean for a FIC?

It is a long way of saying that we only really want the FIC to hold stocks domiciled in countries that don’t levy dividend withholding tax.

Significant countries where this is the case are the UK, Hong Kong, and Singapore – plus funds in Ireland.

Hong Kong is, of course, not on the qualified territories list, and Singapore is not very interesting.

So this leaves us with… UK-domiciled companies and Ireland-domiciled ETFs. Although we may break this rule if the (post-WHT) yield is high enough.

The ETF / fund structure doesn’t avoid this issue, by the way, it just hides it. (There’s the exception of ‘swap-based’ ETFs tracking US indices. Maybe we’ll cover that another day.)

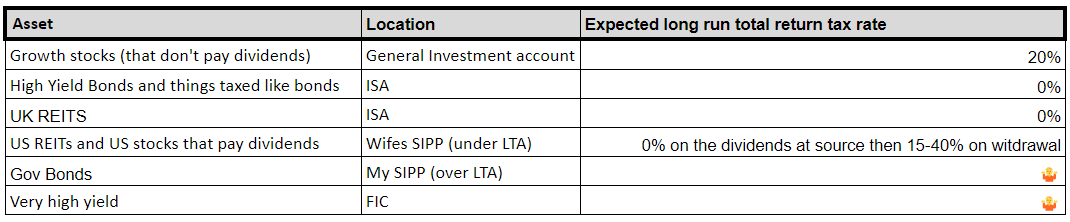

Individual US stocks that pay dividends should be held in your SIPP, where you should pay no withholding tax.

We also want to avoid things where the distributions are interest not dividends, because interest is taxable for the FIC.

So we might buy preference shares – although they are usually not marginable – because they pay dividends. But not AT1 bonds, because they pay interest.

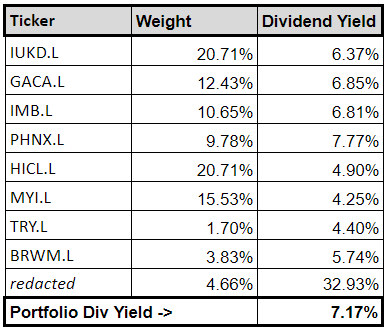

Great, but what have you actually got?

I just alluded to another, personal, constraint – I want my stocks to be marginable at IBKR. Which means big and liquid.

I’d also prefer they were denominated in GBP and paid their dividends in GBP because otherwise it complicates the accounts. This is not much of an additional constraint given the dividend withholding tax issues above.

I’m left with a portfolio that looks very much like the sort of thing a classic UK equity income investment trust might own.

What can I say?

GACA is the only non-marginable share. And I think we can all agree there’s not much danger of these stocks going up much.

Aren’t you letting the tax tail wag the investment dog?

Yes, absolutely, I am. But look at it this way – maybe my portfolio outside the FIC is the global market portfolio minus these stocks in these weights?

I mean, it’s not, obviously, but it could be.

We’re aiming for this:

How actively do you trade this portfolio?

I have an ambition to go a whole year and not do a single trade. I’ve not succeeded yet. We do a handful of trades a year, but some of these positions haven’t changed in at least a decade.

Do companies still benefit from the ‘indexation allowance’ on capital gains?

Sadly not, this was quietly removed in 2017. In my opinion it made the FIC structure substantially less attractive.

What other expenses can I get away with charging to the FIC?

One way of essentially withdrawing money tax-free is to have the FIC pay expenses that you would otherwise have to pay yourself. (‘PA’ as they say).

These effectively get you, as an individual, ‘tax-free’ money out of the company, and are tax deductible for the company. A double win.

The extent to which you can do this appears to be down to the judgement of your accountant. You have to be able to make the case that it’s for legitimate business purposes.

We don’t do as much of this as we should, probably. The company pays for the occasional bit of computer equipment. “It’s for managing the portfolio!” This is depreciated over three years, so basically we get a laptop every three years.

We could probably expense the Financial Times subscription and our mobile phones, but we don’t.

I once tried to persuade the accountant that the FIC should pay from my MBA, but failed.

Can I expense my accountant’s bill for my personal tax return to the FIC?

No. I guess you could come to an ‘understanding’ with your accountant. One where they overcharge you for FIC work and under-charge you for your personal stuff. But I don’t have that kind of accountant.

Do you hold UK REITS in the FIC?

No. This could be quite a good idea, because the FIC should receive the Property Income Distributions (PID) gross. Although PIDs are taxable.

It might work if we have sufficient expenses. However Interactive Brokers don’t pay the PIDs gross, regardless of what the tax rules say.

Attempting to reclaim them from HMRC is theoretically possible, and something my accountant would be delighted to help me with – at a cost.

We don’t really have enough tax-capacity to make this worthwhile.

Can you have direct properties (buy-to-lets) in the FIC?

Actually, yes! We have one, un-mortgaged, rental property in the FIC. We sold it to the FIC in early 2016. Just before the extra stamp duty for companies came in.

The income from the property is, of course, taxable, but it is tiny. We run enough general ‘management’ expenses to offset the income.

I have thought about moving one of my other buy-to-let properties into the FIC, but I’ve not been able to make it make sense.

To be honest if I’m going to sell it – with all the (personal) tax and hassle – I’d rather sell it to some other mug.

Do you have any other assets in the Family Investment Company?

We once did quite a bit of peer-to-peer lending. You know the sort of thing: Lendy, Archover, Funding ’Secure’.

At least it provided us with a deep well of tax-deductible write-offs.

Could I just use the FIC for all my shares?

You could, but it would likely be a bad idea, especially now that the indexation allowance has gone.

Your minimum tax rate on capital gains is 19% (rising to 25%) – and it could be as high as 54.51%. (The company pays 25% tax on gains, then you pay 39.25% on the dividend to you. That’s: 100 -> 75 -> 54.51%).

You’re much better off just holding those assets in your own name and paying 20% CGT.

This all sounds like a great deal of work. Is it?

I spend less time administering the FIC every year than I spent writing this article.

The ongoing obligations are:

- File a ‘confirmation’ statement with Companies House every year. (Takes five minutes. It’s nearly always the same as last year’s).

- File accounts with Companies House every year. (The accountant does it).

- Prepping the information for the accountant and checking their work takes about as long as it does to do our (again, fairly complicated) personal tax returns.

- Filing a tax return with HMRC. (Again, the accountant does it).

- There’s a bit of other admin, like renewing your Legal Entity Identifier periodically. (Interactive Brokers does that for us.)

How much does it cost to run?

It costs us about £2,500 per year. This is almost all accountants’ fees.

I know, I know, it should be less than that.

The costs are proportional to the nature and volume of transactions. But they are essentially fixed with respect to the size of your balance sheet.

(That said, I suspect an accountant would charge the £10m company a bit more than a £1m company, even if they did the same amount of activity).

How much do I need to put in to make this worthwhile?

Well, you know the costs now . You do the maths. Maybe £1m, if you’re starting from scratch?

It might be less if you’re using an existing company, or setting up a FIC that has a relationship with your trading company. I’ve never done this though. Once again, seek professional advice.

Can you recommend your accountant to help me set up a similar arrangement?

No.

Does this cause a problem with your employer?

Potentially. My employment contract explicitly forbids me from owning more than some percentage of a company, or being a director of another company, without my employers ‘written permission’.

The key here is to ask for the ‘written permission’ in good time.

I simply asked, by email, for them to confirm there was no problem with the arrangement in the same email I accepted their job offer. I have done this four times now and it’s never been a problem.

This sort of arrangement is a lot more common than you might think. Human Resources have seen it all.

In jobs where I was subject to compliance ‘personal account dealing’ rules, the FIC was obviously subject to the same rules.

Again, never a problem, if you follow the rules.

While we are talking about transparency…

Anyone can go to Companies House, click ‘Search the Register’, put in your name, find the company you are a director of, and look at the accounts.

There is nothing you can do about this. If this is going to cause you embarrassment, then a FIC probably isn’t for you.

Can I pay pension contributions for directors?

Yes, you can, but I’m not sure why you would?

These are ‘employer’ contributions that are made gross to the scheme – and are a tax-deductible expense for the FIC. You’re saving the company 19/25% corporate tax on the contributions, but you’ll pay anything from 15%-55% on withdrawals (from tax-free amount and basic rate all the way up to the LTA charge). So is there any point?

Again, this is a deferral of tax liability, more than an avoidance. It might be worth considering if the FIC is otherwise becoming liable for corporate tax and ‘needs’ some expenses, and if you have directors who are unlikely to get to the LTA and will be basic-rate tax payers in retirement.

But, again, if you’re rich enough to make this structure worthwhile, you probably don’t have those people in mind.

Can I pay salaries to the family members instead of dividends?

Yes. You could make the kids (once they are adults) directors and pay them a salary – although there’s quite a bit of paperwork involved with having employees that I could do without to be honest.

The advantage over dividends is obviously that their salaries are tax-deductible for the FIC – and you’re just using their nil-rate allowance. (I’m assuming you’re only doing this while they are students, basically).

Into the weeds

Can the company pay interest on the director’s loan?

I believe so, but you do have to do some withholding / filing with HMRC. It’s a bit of a pain – and, again, why would you do this? Presumably the last thing the director wants is taxable income?

Can I convert a regular trading company into a FIC?

I get this question quite a bit.

The classic case is the 1990s/2000s City IT contractor type who contracted through a pre-IR35 personal service company. They now have a few hundred grand sitting in their limited company and don’t want to pay dividend tax to get it out.

Be very careful here. There are some reliefs associated with being a proper ‘trading’ company that you may jeopardise.

This, as with every other word in this article, is something you should take proper professional advice on.

How does a FIC compare to some sort of ‘offshore’ arrangement?

I have a high level of confidence that the FIC structure is 100% above board and has zero retroactive compliance risk from HMRC.

This does not mean that the rules won’t change to make some aspect of it not ‘work’ any more.

The only thing I’m confident about with offshore arrangements is that they are expensive to set up.

In any event, it’s not trivial. You can’t just set your FIC up in the Caymans and pay no tax. HMRC will treat any company that is ‘controlled’ from the UK as if it were UK domiciled and tax it accordingly.

I do know people with offshore companies that they don’t ‘control’ – but are controlled by a chain of shadowy proxy entities that they also don’t ‘control’.

I am sure this is all completely legit, the way they’ve done it. But I also don’t have the sort of money that makes this level of risk or complexity worthwhile.

Is a FIC a ‘close company’ and does this matter?

Yes, most likely your FIC will be a close company. There are a few anti-avoidance measures that target close companies specifically – for example, targeting manoeuvres such as you moving abroad for a year and paying yourself a big fat dividend.

Unless you’re trying to use those avoidance methods, being a close company shouldn’t really make much difference.

There have been different tax rules for close companies in the past. This is certainly a potential vector for the government if they wanted to attack this sort of structure.

Is there anything you haven’t mentioned?

Yes – there are a few other tricks that I don’t want to discuss openly on the internet!

Thanks to Foxy Michael, who met Finumus on Twitter and was kind enough to review this article for gross falsehoods. If this Family Investment Company FAQ has whetted your appetite, visit his site. You can also read more from Finumus in his archive, or follow him on Twitter.

Comments on this entry are closed.

I wonder if the deal-breaker for many would be having that £1m in cash to lend to the FIC. This seems a good approach for investing an unexpected windfall, but beyond that most other sources of the personal lending to the FIC would involve paying CGT on the way in.

Interesting article, and definitely food for thought.

When you moved/sold your BTL into the FIC, was it as a direct ownership or as it’s own Ltd company / SPV? i.e. making the FIC act as a holding company?

I’m assuming the FIC should be able to get a mortgage on the property which would then provide some additional liquidity/leverage but guess the bank is going to be duly diligent on this sort of arrangement.

“Yes – there are a few other tricks that I don’t want to discuss openly on the internet!”

Maybe not the smartest thing to post in a forum that might well have a few senior Inland Revenue employees visiting it …

@ Alex

I’m not the article author but have investigated incorporation for my BTLs.

Moving property into a FIC is treated as a market value transfer and would crystallize personal CGT, and usually Stamp Duty also. Incorporation relief is potentially available (if the transfer counts as being a ‘business’ – normally single BTLs can’t be transferred in this way) which would defer the CGT (the gain is rolled into reducing the base cost of the shares acquired).

FICs can mortgage the property but at commercial / Ltd Co BTL rates which are currently >6% with 2% lender fees, so not cheap at all.

Great article, many thanks. I run my own FIC, and still learnt a lot.

I didn’t know about pref shares, so thanks for that – I had wrongly assumed them to be interest income.

I think that Luxembourg is on the ok list – a fair few funds and ETFs are based there.

I also understand that UK based investment trusts can be interesting where the dividend yield is maintained at high levels – such as for the JP Income and Growth range, and others where capital is used to pay dividends.

Any disagreement?

I would love to know the “few other tricks”. Feel free to drop me a line, and swap ideas!

Even though the FIC is written from a high net worth point of view, I find that business owners can benefit much more from this structure.

That’s because it’s much easier to invest the company profits into a FIC (loan or holding co) than having to take the income home *and then* invest it via a company (expensive). It can have certain tax implications so definitely take advice and learn about it.

But it can be anyone with a LTD co really and can be very profitable if you don’t *need* the money right now. Marketing agencies, doctors, IT contractors, flower shops etc.

Also BTL company investing has become popular lately. One can always build a property portfolio in a company. You can treat the mortgage interest payment as a business expense while taking into consideration the great points Finumus made about FICs. Share classes, expenses, dos and donts for inheritance etc.

@Alex We owned the property directly, and we sold it to the FIC (the FIC already existed, so it’s not an SPV). I did my own conveyancing – LOL. We paid CGT when we sold it to the FIC, but allowances and losses covered it. It didn’t have a mortgage, and it doesn’t have a mortgage now in the FIC – so I have no idea what appetite lenders have for providing a mortgage to a FIC. TBH it’s too small to be worth mortgaging, given the fixed costs, and how much lower margin rates are (not that these are equivalent by any means)

@Neverland – LOL – I’m not doing anything illegal – I just don’t want to draw attention to some stuff.

Nice article. Specifically, as an investment vehicle what are the obvious benefits over an offshore life insurance bond? I can see it’s marginally cheaper to run (say 0.25%/million vs 0.45%/million) and good for dividend equities. By comparison, the bond can hold pretty much any fund whether it produces a dividend or not and pay zero tax whilst in the wrapper. So 100% gross roll up.

I suppose you pay dividend tax on a distribution in the FIC vs. income tax on the bond but the difference is getting more marginal. Plus the bond has top-slicing relief but I don’t see that with the FIC.

TL/DR hypothetically, is a FIC suitable for IHT mitigation on an estate of say 3m ish?

I feel you’ve answered this above but my pea-size brain isn’t digesting it on first pass.

The £1m that is loaned to the company and paid into the brokerage account comes from investments outside a tax shelter, so presumably you have to suffer capital gains to liquidate? In specie asset transfer not an option? If you have cash or invested cash in an existing Ltd Co, presumably the same is true, it has to be liquidated as dividend payments to access and transfer to the FIC? Also does having an FIC if you already have a trading Ltd company affect the threshold for small company tax rate for your trading company?

Hi,

Thanks to everyone at Monevator. This site has pretty much taught me everything that I’ve needed to know about investing.

Finumus, I’d be really interested to see another version of this article with more of a focus on capital that is injected from investing excess profits from an existing business?

Specifically around how this should be done…

e.g businessA owns investmentSpvB or using a holding company structure?

I should add to my comment above that this is of course an area where professional accountancy advice is always going to be needed.

However I always like to learn the basics before engaging the professionals!

Great article. I toyed with setting up an investment company several years ago, but not for long. The only potentially beneficial feature I could see was the indexation allowance, now gone (frozen as of Jan 2018) as you have pointed out. The whole thing just seemed like I would be creating an annoying long term tax problem and I already have enough of those with conventional investments outside tax shelters.

I would be interested to know how you think your returns may have compared had you instead invested the whole lot into a global tracker and reinvested the after tax income, which is essentially what I did, although I invested in separate ETFs, including a US listed ETF for US shares to take advantage of the WHT credit. ie has all the extra complexity been worthwhile? I guess if you have been using high leverage during the bull market the answer is likely to be yes it was worth it, but you could have applied leverage with tracker ETFs instead.

I appreciate that this may be an incredibly difficult question to answer!

Do you ever rebalance at the total portfolio level (across all account types)? What benchmark do you use? I’d venture a guess that your allocation to UK dividend shares is higher than most benchmarks (if they ever include this as a sector).

Very interesting article. I think 20 years of experience offer a unique perspective, it would be great to read more about how things have evolved over time.

Great post 🙂

One could presumably set up a FIC as an unlimited company, which means you don’t have to file annual accounts.

Also I imagine it’s generally not considered a great idea to have FIC that directly owns rental property. What if the roof caves in on your tenants and your FIC gets sued?

Really interesting article. What are the audit requirements for an FIC or is it the same as for any other Ltd co?

A FIC is unlikely to have employees or material turnover, so if net assets are less than either c.£300k or c.£5m then respectively micro or small company accounts are normally permitted. In either case a director enters a few basic figures confirming the assets and the liabilities, which are entered online for Companies House. The same unaudited data is provided to HMRC to confirm the amount of corporation tax.

If the FIC is for a long-term buy and hold of share investments, receiving dividends, and annually paying some dividends out and reducing the director debt liability, then the assets would be the value of the investments plus any cash in the company bank account, and the liabilities would be the remaining amount still owed to the director after any dividend payments. It’s not even clear whether any accounting package would be necessary, a spreadsheet may be all that’s needed to keep track of the value of the share investments, cash, and money in and out the company. In this situation where does the need for the accountant come in? Are there other complexities or specific obligations on FICs? If audit fees can be avoided and director prepared figures are OK, then the FIC is potentially a lot more attractive.

Whilst I could never envisage needing such a vehicle it is interesting to read about, so thank you for the article.

I was one of those IT contractors in the 90s and again in the 20-teens, though I cashed out in 2017. It is remarkable in hindsight how generous the mid to late 1990’s tax regime was, pretty much pay your minimum NI stamp, quarterly ACT (Advance Corporation Tax) at 20% and bank the rest.

+1 on Great Article. & as you say, more good stuff on the same theme @ Foxy’s site too, thank you.

Re Property Income Distributions (PIDs), has anyone heard of anyone having any success in claiming their (effectively paid twice) tax back? In theory HMRC should be open to this? Asking, you know, for a friend..

Re Pension Contributions to Directors, this could be increasingly useful as inflation pushes nominal prices up? Presumably over time IUKD etc will inflate too, creating ‘profits’ liable for Corporation Tax at 19%+. If you or your partner isn’t close to the LTA, a SIPP contribution would save the 19% + also the dividend tax (you’re not having to take the money out of the company in the future, paying from 8.75% up to 39.95% or whatever). It could then compound up tax free in the SIPP (including US ETFs etc) before hopefully paying out a 25% cash free lump sum and the rest at income tax rates? Unless you’re both close to the LTA that sounds pretty compelling?

Firstly thank you very much for taking the time to pen such a detailed and well thought out article. I’ve been mulling over a FIC for a while.

I’ve been put off by the fact there is no indexation allowance as highlighted by Naeclue.

No doubt you are better read than I on this subject but I understood that IHT was one of the main purposes. You transfer in the assets to the FIC on day. Your offspring are shareholders. They therefore benefit from the growth without any IHT issue assuming you live for >7 years (PET transfer). You can keep control of the dividends through different classes of shares and the repayment of the loan. Feels a very flexible structure here.

My understanding is you have a unlimited company (note unlimited liability…) the filing requirements are even less

https://www.saffery.com/insights/publications/family-investment-company/

I actually bought this book to read and would recommend anyone else. I don’t have it with me but in it they seemed to cast some doubt on whether the loan structure would work. i.e. that the loan potentially could not be paid back tax free. As I say I’ve never implemented one

https://www.amazon.co.uk/Bloomsbury-Professional-Tax-Insight-Investment/dp/1526524694

I would though be interested in why you think this structure is better than an offshore bond, which seems possibly better I think per a comment above as the assets grow tax free, 5% back tax free a year – like the loan repayment I suppose and then repaid at your marginal rate at the end.

Now that CGT relief is being eliminated I suspect I’ll end up down one or more of these routes.

Would be great to hear from anyone else who has these structures – pros and cons.

Also the irony of this post and the last post around surviving with no heating wasn’t lost on me – monevator caters for a broad church!

@Naeclue: Dividend investing vs global tracker in a company is an interesting one. In fact, I am writing a case study on it. Without looking at the numbers, my gut feeling is it depends on your exit strategy, after the X years of accumulation. If you wanted all money out, then corp tax + income tax would sting. But taking it gradually can mitigate both.

If you want to make an apples-to-apples comparison you need to pick 2-3 different exit strategies and then compare based on that. Because how you plan to “exit” can dramatically affect the outcome post-accumulation.

Also, corporation tax is ONLY on profits, not on the whole lot. This makes it easier to offset expenses such as salary for the family, director’s pension and other business expenses in the same company tax year.

@Vroom I agree with you, a pension contribution can work wonders if you have taxable profits. With pensions one has to be careful though – They are a form of remuneration. Like salary, the compensation has to be ‘wholly and exclusively’ for work you did for the business.

@MNW Yes, having a FIC and another limited company would affect your small profits rate thresholds because the companies are Associated. So the thresholds would drop by half and you’d pay more corporation tax. Not a deal breaker in the grand scheme of things but not zero either.

Also, the loan from your trading co to a FIC / investment company would be a non-trading asset for the trading company. It can affect your ‘trading status’ if you do it in a big way. It depends on the company assets as well – a software company might be light in hard assets and sit on cash, but there’s intellectual property and things you can do.

I explained the company lending and the holding company concept in more detail here: https://www.foxymonkey.com/how-to-invest-your-company-profits/ and here

https://www.foxymonkey.com/invest-company-cash/

I stand by my statement: Business owners can benefit a lot from ‘unlocking’ their company capital, despite the April 2023 tax rules.

Michael @FoxyMonkey – I am so grateful you popped along to this comment section else I would never have stumbled upon your invaluable post. About 75% through the comments on your post & its so enlightening.

@MNW – We don’t seem to need an audit, we file smaller company accounts. We basically just do what the accountant tells us we need to.

@Vroom – re. Making directors pension contributions. I agree it’s certainly worth considering if you’re other alternative is to have to pay CT. The life time-allowance is the big problem here really – and I don’t want my wife / kids in a situation where they could be avoiding 60%+ tax on their employment income in the future because the FIC already filled up their pension at an effective 25% tax saving. The LTA seems to be fixed forever at £1.07m in nominal terms – in a few decades that’s going to be nothing.

@SeekingFire + others mentioned “offshore bonds” – I have no idea of the relative merits – it’s perhaps remiss of me, but because they are a thing that ‘wealth’ advisors tend to push, I have always assumed they are very bad value, and never really done the work of checking them out. I too would be interested in such a comparison.

Hi, I love your writing and based on what you write about, I think you are a very smart person.

I have some considerations:

– either you are running a suboptimal allocation overweighting those names: would not be better to have an optimal asset allocation that would generate higher expected returns, even if they are taxed today instead of tomorrow? [I see dividend stocks as a poor proxy for the value factor]

– either you park the right amount in this vehicle, which means you have what, at least 10 to 15 mil outside of it? Given that you “already won”, it continuously comes to my mind that meme “men would literarily do this instead of going to therapy”. London is not exactly California, wouldn’t it be better to try to be subject to an entirely and less nonsensical tax system than trying to fight this one? I guess this comes more from me being a European angry at Brexit than anything else but…worth a try?

– either there are a lot of advantages in this structure that for obvious reasons you do not want to describe here in the open and this is just a teaser to push people to do their own research and find the hidden treasure.

Anyhow, great post as usual

Very insightful and well written article. Thanks for this.

Something I wanted to ask was around this piece:

>In jobs where I was subject to compliance ‘personal account dealing’ rules, the FIC was obviously subject to the same rules.

Does that mean you had to go through the typical compliance approval step when intentioned to buy/sell shares of stocks/ETFs/etc?

Did you find this particular restriction more generally something you would rather not have, to have freedom of choice for the things to trade in your portfolio?

Thanks

Redacting the ticker for the 33% dividend-payer is just.so.cruel.

Onedrew – I am guessing the redacted 33% dividend payer is some sort of wheeze involving a private company whereby Capital gains losses are created by paying out excessive dividends.

Very interesting but we have nowhere near enough to make an FIC worthwhile.

Interesting as ever @Finumus. I agree with @Nicola sentiment, you make an argument that this is part of a larger picture of asset allocation, but I imagine the firewall means its tricky to rebalance? I’m wondering whether the analogous ideal high growth no dividend index tracker into a GIA is just simpler – and liable to CGT at currently much better rates. Deal with income production in the tax shelters?

Very enjoyable and entertaining article.

For what it’s worth my 20 years old ‘FIC’ holds rental property from which my wife draws a wage. Yes we pay NI/Income Tax…shock horror….equals Full state pension down the line. However she has been furloughed (paid by the state as we play with a straight bat), had a SIPP pension built for her and a VCT portfolio. I have double dipped on the tax reliefs available courtesy of the income tax she has paid.

Lot of work but I actually enjoy it.

@Nicola – These are good questions you raise. I agree this is mostly a (poor quality) value tilt portfolio. Well I didn’t disclose how much I have in the FIC (or indeed outside it) – but your point is well made. It does skew the asset allocation – and this is likely suboptimal from an asset allocation POV. But here we are. I’m not wealthy enough for it to be worth trying to escape the UK regime – I’m not sure I would even if I was (baggage) – and, as you observe, that’s anyway been made much harder by my compatriots.

I guess you’re hinting at the question I didn’t answer explicitly – “is it worth it? Would I set up this structure now if I didn’t already, have it?”. The honest answer to this is probably ‘no’ – and the clincher is the removal of the indexation allowance – which has motivated the extreme skewing of the asset allocation to high yield trash.

@Jon

“Does that mean you had to go through the typical compliance approval step when intentioned to buy/sell shares of stocks/ETFs/etc?” – Yes, I did. Obviously I’d rather not be so constrained – but the rules are the rules.

@Calculus There’s not really any such thing as a ‘no dividend index tracker’ – you’re aware that just because a fund is “accumulating“ – you don’t receive the income but you still have to pay income tax on it? And…. that then massively complicates your CGT calculations?

@Finumus: Yes I had an idea of that! – its the target Im describing, as you have done in notional no capital gain/loss stocks. Which one is more difficult to keep track of I’m not sure, but I’d have thought there’s enough people doing GIAs that there will be some automation to help. Long bonds would be another vehicle that can potentially be set up for tax free CG and next to no income.

It’s too difficult for me to work out, but wonder if there is something to be done using dividend options/futures or indexes (e.g. FTSE Custom 100 Synthetic 3.5% Fixed Dividend). Also if there is some tax benefit to employee share plans (provided to family members).

@Vroom To claim tax back on REIT payments use this form: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/373948/uk-reit-dt-company.pdf

Not a pleasure, but not impossible!

@Daz Have you ever claimed the 20% PID back from REITs domiciled in Guernsey? Many of them are based there.

@Foxy. No, only GB. I think I have only ever seen a couple of GG REITs though, majority are GB.

I use the domicile field to make sure my watch list is relevant. On the whole though even GB REITs are a hassle I prefer to avoid for my FIC. But it is doable.

@ Daz – That’s brilliant, thank you.

@ Foxy – Going through last years company return (with my friend) there are 6 GB REITs (AEWU, SIR, RESI, LXI, PRSR, BBOX), 0 Guernsey and 1 Jersey (SLI, now API). Worth a go with that form…

It is worth considering the default position before going down the road of FICs, offshore investments, Trusts, etc. to compare the investment drag you are likely to experience with each. If you invest in something like a World tracker, your income yield will be about 2%. The dividend tax rates are going to be 39.35%, 33.75% and 8.75%, implying investment drag of about 0.8%, 0.7% and 0.02%.

CGT is optional and with something like a global tracker it is very unlikely that an a corporate action will dump an unwanted capital gain on you. Even if selling for consumption, you don’t have to crystallise all the gain in one year and you only pay CGT in the year of disposal. The tax on the as yet uncrystallised portion can continue to stay invested, paying dividends and participating in growth until crystallised. When you do crystallise, you may be able to do that within the 10% band, but even if you have to pay 20% that is still better than the 25% corporation tax you would have to pay with a FIC, plus dividend tax to liberate the money from the FIC.

0.8% investment drag on the income is high, but not disastrous. Many people are happy to pay comparable amounts or even more on expensive actively managed funds and wealth managers.

I chose not to go for a FIC or any other measure (offsore/trusts were more expensive options), partly because my wife and I were intending to stop paid work soon anyway, 3 years max. After that the investment income was going to fall out of additional rate rate tax with most of it falling into the basic rate band and some even into the personal allowance.

CGT is a pain and we have reached the position where we will be unable to fund our ISAs without crystallising some taxable gains, but that is very much a nice to have problem.

@Finimus “There’s not really any such thing as a ‘no dividend index tracker’ – you’re aware that just because a fund is “accumulating“ – you don’t receive the income but you still have to pay income tax on it? And…. that then massively complicates your CGT calculations?”

Actually there are a few no dividend trackers. For example, an inexpensive equity swap based S&P 500 tracker (I500) was launched by iShares a few years ago that does not pay dividends or have any excess reportable income. I have a feeling it may not pay anything equivalent to dividend withholding tax either as it has outperformed the 2 other iShares S&P ETFs over the last 2 years.

I think “massively complicates your CGT calculations” is a little extreme by the way. Subtracting the notional income from the acquisition cost is hardly rocket science 😉 Something anyone should already be doing with excess reportable income in any case.

@Naeclue – Well – thanks for bringing that to my attention (the ‘no-dividend’ US tracking ETF) – That is exceedingly interesting. I was aware of using the swap structure to avoid US WHT – but I hadn’t twigged that this turned dividends into capital gains. Makes you wonder why they don’t do more ETFs like this, I’d love to see a swap based global tracker that did this with all the income (and avoided US dividend WHT in the process). Txs!

@Naeclue, @Finimus

I echo Finimus’s comments. Many thanks.

I have started trawling through the swap based etfs.

Any other similar no excess income etfs Naeclue?

Ishare don’t have any others. Amundi and Invesco didn’t have anything. Nor Vanguard.

The Invesco DM world etf looks to have avoided withholding tax except for in a couple of smaller European jurisdictions – but does sadly have excess income to declare.

Will report back with anything I find…

@Daz, I have come across other swap based S&P 500 ETFs in the past that I think avoided withholding tax, but cannot remember whether they avoided dividends entirely. They had higher management fees though. The iShares one is interesting because of its low TER of only 0.07%.

Some swap based ETFs closed down or switched to replication after the GFC when they went out of favour.

Swap based ETFs lack the transparency of replication based ETFs. They should be fully asset backed, marked to market daily and so free of additional credit risk, but opaque structures have blown up in the past. I would hesitate to put all my eggs in swap based ETFs even though I cannot precisely put my finger on where any additional risks might be hiding.

@Finimus, I thought the iShares ETF might avoid dividends by just holding non-dividend paying S&P 500 shares, which it then swapped with a US based counterparty for the TR of the S&P. But the list of constituents definitely includes dividend payers, so I am unsure how it actually works.

@Naeclue Many thanks again.

Agree, I have historically kept swap based etf exposure to low levels. Too many memories of swap based products blowing out on counterparty risk in the gfc.

S&P 500 Swap. Indeed very interesting. Looking at Ishares it appears it has no reportable income. Also appears that it tracks the index albeit the history is only a couple of years.

The constituents though don’t seem to make much sense to me

The risk is I think with the counterparties….

I copy the below from the prospectus

Think for additional rate tax payers this is pretty interesting though

As is Berkshire Hathaway albeit the grim reaper risk must be sooner rather than later in that case

iShares S&P 500 Swap UCITS ETF

Investment Objective

The investment objective of the Fund is to seek to provide investors with a total return, taking into account both

capital and income returns, which reflects the net total return of the S&P 500 Index.

Investment Policy

In order to achieve this investment objective, the investment policy of the Fund is to invest in FDI, in particular

unfunded total return swaps, which will seek to deliver a return which reflects the performance of the S&P 500 Index,

the Fund’s Benchmark Index. When using unfunded total return swaps, the Fund will invest its cash in global

developed market equity securities (the “Substitute Basket”) and will pay the return of the Substitute Basket to

the counterparties under the swaps, which will enable the Fund to deliver exposure to the Benchmark Index. The

swaps with counterparties will be entered into on such terms and in such manner as determined by the Investment

Manager.

Where investment in total return swaps is not possible or practicable, the Fund may also gain exposure to its

Benchmark Index through investment in other FDI such as options and non-deliverable futures, through investment

in units of collective investment schemes, and / or through investment in a portfolio of equity securities that, as far

as possible and practicable, consists of the component securities of the Benchmark Index.

There is no guarantee that, through the Fund’s investment in the total return swaps, the Fund’s returns will track

exactly those of the Benchmark Index.

In accordance with the provisions of European Market Infrastructure Regulation (EMIR) and the terms of the

documentation governing the relevant swaps entered into by the Fund, each of the Fund’s counterparties are required

to provide collateral to the Fund (and vice versa) to cover the net mark-to-market exposure in respect of the relevant

swaps entered into between that counterparty and the Fund. Pursuant to the terms of such documentation, collateral

is transferred to the Fund by the counterparty (or vice versa) if the relevant mark-to-market exposure exceeds the

minimum transfer amount (the purpose of which is to avoid de minimis transfers). Pursuant to EMIR, the minimum

transfer amount shall not exceed €500,000. In cases where the Fund has uncollateralised risk exposure to a

counterparty, the Fund will continue to observe the limits set out in paragraph 2.8 of Schedule III. Collateral

transferred to the Fund will be held by the Depositary

@Finimus and @Naeclue, thanks for the excellent article and additional comments. On swap based S&P500 ETFs the fly in the ointment is that the swap party is not benchmarked against the gross TR index but only delivering based on the net TR index benchmark after deducting notional dividend WHT. There may still be a tax benefit of receiving capital gains rather than dividends, although in some cases such swap based ETFs still seem to trigger excess reportable income.

Could a Ltd company borrow the £1m to invest in the FIC that has the same shareholding structure as the Ltd company?

Excellent post, thank you very much for putting all this together.

This is very timely for me as I just started a personal investment company (not FIC in my case because the rest of my family are US citizens (I am not!) and it’s better to keep Uncle Sam out of this). The purpose for me was not so much to invest money currently outside companies but cash built up in my and my wife’s personal companies (consulting), via inter-company loans.

I also considered injecting equity to the PIC in a personal capacity as well. The main motivation being dividends, taxed at 39% outside wrappers, but not if paid to a company. Even if you eventually take them out and you are still at 39% div tax rate, the compounding of reinvested dividends until then could make the whole operation profitable in the long run. Here’s a basic model (for additional cash contributed as equity or debt from a person, not a company, to the PIC):

In reality, cashing out from the PIC will be when personal div tax rate is significantly lower, which makes it even more attractive to invest via PIC.

The benefit of investing via PIC is greater the higher the percentage of equity returns are in the form of dividends. For this reason I was planning to hold higher yielding UK/European ETFs (VUKE, VEUR) in the PIC while continuing to hold US ETFs (VTI) in my GIA.

An additional reason for not holding the US part of equity allocation in the PIC is to avoid the div tax withholding being lost. At least in the GIA I can use it as a credit against the UK div tax liability.

And then I read Naeclue’s comment re: the I500 ETF, which makes it even better to hold US exposure outside a PIC (no div tax leak at all). Depending on the size of existing unrealised gains and whether there’s available CGT allowance, it may even make sense to switch existing positions to i500. For large gains it’s probably not worth it. If unrealised gains are 50% of original investment, break even is about 20 years, if 20%, 10 years:

But the very existence of i500 sealed the deal for me on whether to bother with using the PIC as investment vehicle for money that is currently outside a company, and the answer is no. I will use the PIC to invest the cash built up in existing companies, but for anything outside corporate structures that is not already tax sheltered, i500 and (mostly tax-free) UK Gilts will do just fine.

I noticed that the embedded links in my previous comment didn’t make it, so trying again.

Here’s the model for investing via limited company versus in a personal capacity:

https://docs.google.com/spreadsheets/d/e/2PACX-1vSmRwi34WnwYKrvG2f2jhYpyh_co9o9nvSnXEcbSFEqlvUunVswummbMXVkZEPbLj9Tl-Pp2kJ5VWZU/pubhtml

And here’s the calculations for switching from existing position in VTI with unrealised gains to a new position in i500 ETF:

https://docs.google.com/spreadsheets/d/e/2PACX-1vRsky8xF_11KKnzbm1QlHQLys__NehK8xnm8O-pdShJrJyMSJ48l9-Q_ptyPnbneGZco2D5zexNfyhr/pubhtml

The eagle-eyed may notice that I used 25% in div tax leak instead of 39%. That’s because most of the times I partially defuse them by temporarily switching to another ETF prior to ex-div date and rebuy a few days later, therefore the dividends turn to capital gains charged at 20% (benefitting from the 30 days B&B rule, therefore the preexisting gains are not taxed).

More on the i500 ETF: there’s another swap based S&P500 ETP, ticker is SPXP, ISIN IE00B3YCGJ38. It has 5bps TER (compared to 7bp for i500) which would make it slightly better, provided that it does not have excess reportable income.

I searched here: https://www.kpmgreportingfunds.co.uk/Home/PublicInvestor for it, and the latest information is from 3 years ago for distribution in May 2019 for reporting period ending in Nov 2018. Does anyone know if this means that there was no excess reportable income for subsequent periods (and presumably going forward), thus making it a good choice for long term holdings that we don’t want to be taxed on received dividends, or is it simply an omission on the website and the fund still has excess reportable income?

Hi MP

I had looked through the Invesco etfs, so know the answer! Report for 2020, showing excess reportable income:

https://etf.invesco.com/sites/default/files/documents/Invesco%20Markets%20Plc%20-%202020%20Investor%20Report.pdf

So sadly seems not 🙁

Thanks Daz. I500 it is then (for new purchases – not worth paying CGT to switch existing positions).

Interesting article. I’ve been wondering about an FIC for years.

I’m curious about some of the no-growth portfolio. MYI, TRY, and BRWM all seem to have delivered quite a bit growth in the share price over the long run. MYI has grown 300% in 20 years.

Are they only viable because of the mystery 33% div yield investment, which presumably has a share price that declines, so this offsets the growth in the other three?

An earlier post suggested that using an unlimited company for the FIC would mean no accounts have to be filed. That’s right, but I think the company would still need to produce accounts for its members. So, would this significantly reduce accountancy fees? Those fees will primarily be for preparing the accounts, not for pushing a button to file them.

Or, can you just use a simple P&L and Balance sheet, without all the notes to accounts? If so, then many people could probably manage without an accountant and save a fair bit of cost.

Thanks. Really interesting stuff.

I use a limited company structure to aggregate riskier lending so that capital losses can be offset against performing loans.

I haven’t used it for equities because I thought listed securities would need mtm treatment and I didn’t want to deal with a dry tax charge. Is there a particular exemption being employed here in delaying CT until realisation in the same way as CGT or have I misunderstood this requirement?

Hi J.

There is no MTM for tax on equity and equity related instrument.

There is however for debt or debt related instruments. (This includes funds with over 60pct in debt at any point in the year).

Thanks Daz

If you were in big bucks territory – three rather than two brackets as in example – then running own FIC as professional (salaried) office holder (CIO and/or CFO) would be a cost effective ‘trust fund’ job:

https://www.financialsamurai.com/trust-fund-job/

As long as it was wholly and exclusively for the benefit of the FIC (and, therefore, a genuine role that needed doing), and renumerated at an arm’s length, fully commercial rate; then it may perhaps be an allowable expense of the FIC in its CT profit computation under GAAP (s. 46 CTA 2009) and for the purposes of CT more generally (s. 54 CTA 2009). In any event, take independent advice from relevant qualified specialists (i.e. in tax law, company law and accounting) before either deciding to do or not to do anything in this complex area.

A salary is an allowable expense anyway, which makes sense considering that the total tax+NI paid (employer and employee) is more than what the corporation tax would be.

As the post you linked to says, the purpose of this made up job is primarily to create a façade and show some purpose for the employee to external observers, and not any actual economic benefits.

the latest report for i500 (to 31/3/23) shows significant ERI at a rate that seems equivalent to the S&P500 yield. For the year to 31/3/22 it was zero. Something seems to have changed.

https://www.ishares.com/uk/professional/en/products/314989/ishares-s-p-500-swap-ucits-etf-fund

I always mused that the perfect FIC holding would be a world index that cannibalised itself for a high yield each year, well, JP Morgan and Blackrock have both recently launched active ETFs that aren’t quite doing that, but could be a very good match – JEGP and WINC.

They both use an MSCI world benchmark and advertise an extremely high yield (7-9%), achieved by using covered calls in addition to global equity holdings.

It’ll be very interesting to see how popular these become, their launch has come about due to the wild popularity of JEPI in the US, which follows a similar strategy but tracks the S&P500. I’ve already reworked our FIC holdings to try out a small amount of JEGP, I wouldn’t be surprised if they become core holdings for many people relatively quickly due to the high ‘tax free’ income, but ability to still get fairly close to a global growth tracker portfolio.

My 2 favourite FIC holdings are now JGGI (JPM Global Growth & Income – promises 4% of NAV as dividend) and JEPG.

Thanks for the comment.

I have tried a bit of WINC, but hadn’t heard of JEGP. Will buy some with this month’s dividends.

My largest position in my FIC is also JGGI. Plus some infrastructure trusts, some pref shares, some very dull income trusts, and a splattering of single names.

Thanks for the article. Very interesting read. I am currently researching setting up an FIC despite the cons. Just wondering how did you set up the bespoke memorandum/articles of association and shareholder’s agreement?

Fantastic article – I expect it to get a lot more traffic given Labour’s now revealed intentions.

When you mention not being able to dividend out if spending a year abroad I assume that restriction would not apply (at least under current legislation) if one permanently emigrated as the recapture would be on the individual rather than the company?

Actually I have stopped being lazy and answered my own question.

RDRM12610 Guidance on temporary non residence does seem to indicate if non resident for 5 years or more per the residence tests then this would cease to be an issue.

So I guess if the dividend roll up continues to work then there is a tax free extraction method in the long term if retiring to the right jurisdiction…!

Missed the original question. That is absolutely right. Possible niggles:

1. A capital gains exit tax is a risk. Talked about, denied, but possible. And Reeves has advocated for it in the past.

2. The 5 years used to be 1… in the olden days a final 12 months working in HK was the norm for many a high flying banker.

I realize this thread is from 2023.

Great article – thanks

I wanted to ask – what is the SIC code for a family investment company?

I use 64991 – Security dealing on own account

Ever considered super HY extreme deep value plays for the FIC @Finumus?? E.g. Petrobas and Ecopetrol give 15%-20% p.a. on P/Es of 5x-8x and EV/EBITDAs of 3x-4x.