This article can be read by selected Monevator members. Please see our membership plans and consider joining! Already a member? Sign in here.

What caught my eye this week.

Once again we have disappointing economic data in the UK. And once again, the elephant in the room is missing from media chatter.

The Bank of England was split on its decision to cut rates by 0.25% to 4% this week – it had to vote twice to reach a verdict – with stubborn inflation making cutting rates riskier than it should be.

This despite a UK economy that is barely growing.

It’s not stagflation – not yet – but it’s a close cousin. No wonder there’s fewer people accusing me and others of talking Britain down these days.

I mean, it says something when a Coinbase ad mocking UK PLC – and our dumb acceptance of our lot – goes viral not because we’re outraged, but because we see the truths:

Now, it doesn’t seem like this ad was really banned, as some claimed.

And if it was steered off-air by the regulators, it’ll be for disclosure reasons, not because of Stalinist diktats from on high.

All the same, given that almost nobody else dares to speak of the economic ill that continues to grind in our gears, I’m sympathetic to the notion (not the reality) that ‘they’ are suppressing the truth.

Leave it out

Despite this near-blackout on Brexit, at least the public has woken up to its mistake.

A new poll for The Sunday Times showed only 29% would vote Leave again.

And no wonder!

Reminder: not only is the UK economy growing nowhere, but the government is said to face a £41bn fiscal ‘black hole’ which means taxes will have to rise again.

From the BBC…

NIESR said the shortfall in the government’s budget was in part due to weakening growth over the past few months, resulting in a lower tax take and higher government borrowing.

But the reversal of welfare cuts, which were originally designed to save £5.5bn a year by 2030, had also had an impact, it said.

…which is all true, no doubt. But the UK economy wasn’t born yesterday.

I know some are bored of me repeating it, but multiple independent estimates say that a ‘Remain economy’ would be at least £100bn bigger.

And that missing GDP equates to around £40bn of lost taxes.

So – once more with feeling – this £41bn black hole is basically due to Brexit.

My diagnosis: the State carried on with its pre-Brexit cruise control spending, but the economy to pay for it has leaked too much air from the tyres.

Sure things would be rough regardless. Covid happened. Ukraine. Trump and his trade wars.

But we lowered our baseline growth in 2016, and that all just made it worse.

A lot of little decisions add up

Counterfactuals and shades of grey seem hard for some people to understand.

So to give just one example, yes, the City of London has expanded after Brexit.

But it would expanded more quickly without it.

How do I know? Because the banks have told us so – and the wonks have backed it up with research.

Goldman Sachs’ CEO said this week that London’s position was “fragile”, noting:

“London continues to be an important financial centre. But because of Brexit, because of the way the world’s evolving, the talent that was more centred here is more mobile.

“We as a firm have many more people on the continent.”

EY’s Brexit tracker reported this week (paywall) that the five biggest investment banks have added 11,000 jobs in the EU in the five years since Brexit.

Most of those would have instead been high-paying and tax-generating jobs in London in a Remain timeline – simply because there would have been no reason for anything to change.

From the same article (my bold):

Michael Mainelli, the former Lord Mayor of the City of London who leads consultancy Z/Yen, estimates that 40,000 financial services roles have moved from London to the EU because of Brexit.

Meanwhile, the number of people employed in the City has grown since the 2016 Brexit referendum by around 130,000 to reach 678,000 at the end of 2024.

“The City of London has been growing and continues to do so,” he said.

“I remain bullish on London, but proportionately it is likely to have done better if it wasn’t for Brexit.”

Is the penny starting to drop at the back?

It’s not all or nothing.

It’s not depression or boom time.

It’s just a bit worse, year after year, which is more than sufficient to add up to the 4% hit to GDP that the OBR and others have estimated – and to create a £41bn headache for Rachel Reeves.

Dealing with it

Before anyone comments, yes the US-UK trade deal is slightly better than the EU’s.

The trouble is we sell almost twice as much in goods and services to the EU. Europe remains our lynchpin trading partner by far.

What’s more, the EU (and the world) will very likely get a new deal soon after Trump leaves office and economic sanity returns to the White House.

Whereas we’re stuck with our economically-damaging exile from the EU for at least a generation. (Sorry Ed Davey.)

An overnight crisis ten years in the making

Read the right-wing press – even a few sensible commentators who I know read this blog – and it’s implied that the UK’s travails are all Rachel Reeves’ fault.

As if we were all lounging in the sunlit uplands this time last year. Having our cake and eating it.

Look, I agree that Labour has done nothing much in its first year to improve matters.

Labour’s planning reforms should have helped, but so far we’re building fewer homes. And its better relations with the EU are welcome, but Starmer’s new deal was far from an Undo button.

Meanwhile the hike in employer’s National Insurance is hammering small UK firms, especially those in the service economy. I’m an investor in a few, and they all say it’s been another kick in the teeth.

And let’s not even mention Labour’s welfare reform farrago.

The only tough decision this government has stuck to so far is its foolish election pledge on income tax.

Nevertheless, pinning the UK’s malaise on Labour is rank hypocrisy. Not only do these elements shirk their responsibility for our national blunder, they seeks to stick everything on a one-year old administration.

He who smelt of it dealt it

Why do I still bring up all this ancient history?

Firstly because it’s not ancient. As I explained, we’re living with the consequences. Yet that obvious truth is absent from the prevailing narrative, and it infuriates me.

Secondly, because if we don’t know how we got here then we’ll potentially double-down to make things even worse and vote for Farage and Reform. Whereas that man should be unelectable for what he’s already done to our economy.

But I don’t really need to prove my point. The economy today looks pretty much how I said it would nine years ago, after we voted Leave – a bit worse than otherwise every year, which adds up. And obviously nothing fixed by leaving the EU.

Circumstantial evidence perhaps, but pretty on the nose.

In contrast the other side should have everything to explain. Because Britain in 2025 does not look anything like the nonsense they promised us in 2016.

It should feature in every economic analysis. Yet you barely hear a peep about it.

“Move on!” they cry.

British beef

Okay, so where does all this leave us as investors and savers?

Well, interest rates kept higher for longer for starters. The UK struggled with inflation for decades before it joined the EU, perhaps due to its small size and reliance on foreign trade. Like others, I see signs this disease may be re-emerging.

As for UK assets, it’s obviously incredibly tricky to judge – presuming you’re the naughty type who likes to speculate.

All things being equal the pound will be higher given higher rate expectations versus other currencies, but inflation can work against that.

Same with conventional gilts. Perhaps more reason to overweight mid-duration index-linked gilts in our safety cushions?

As for equities, UK companies continue to get taken out by foreign predators, mostly US. (If the fund manager who disputed my prediction of this in our comments a couple of years ago would like to update us, please feel free…)

So despite all the gloom, I remain very overweight the UK market.

Many UK companies still look reasonably priced, especially versus the US. And the liquidation of the LSE is a catalyst to unlocking their value.

Which is good for shareholders, even if it’s a sorry state of affairs for the LSE – and for the UK more widely.

Pips squeak

Presumably some taxes will have to rise, too. For good or ill more borrowing seems to be off the table.

I think Labour’s income tax pledge is foolish not because I love higher taxes from this level, but because I think endless speculation about where they can pinch and pilfer around the margins is more damaging than just a straight hike.

But really we’re taxed enough already by my lights. There are no good options, and I wouldn’t be surprised to see things get worse if more rich people flee.

There’s been a lot of debate and debunking as to what extent this exodus is actually happening, but I do judge something is going on. The collapse in London prime property prices is surely one eagle-sized canary in the coal mine.

Also before anyone waves a copy of Socialist Worker at me, understand this really matters for the welfare state that most of us – and Labour – care about.

Not only do the rich drive a lot of economy activity, but a mere 3% of taxpayers represent a huge chunk of income tax receipts:

Source: Four.Zero

Finally, it usually is darkest before the dawn and we’ve been in a fix for a decade.

Perhaps if something breaks soon it’ll be a wake-up call that could yet see off even worse in four years time.

Have a great weekend.

While most readers enjoy pulling up a stool and listening to these FIRE-side chats, we do sometimes hear that a particular story is a bit unusual compared to the usual work-to-retirement path. So this time I’m pleased to talk to ‘WeeScot’, who is on a conventional route towards a comfortable early retirement – very much still an achievement, and something we might all aspire to!

A place by the FIRE

Morning! How do you feel about taking stock of your financial life today?

I’m feeling reflective, which is why I offered to do a FIRE-side Chat. I’ve been a regular Monevator reader for many years. However I rarely comment on posts.

Over the years I have learned a lot from the site and wanted to share some of my experiences with other readers in the hope that it would be helpful.

How old are you and your partner?

I’m 54 and my wife is 57. We have been happily married for 30 years.

Do you have any dependents?

We have one daughter who is 28. She is an NHS doctor – the first doctor in our family – working in the highlands of Scotland. She is doing very well and we are both immensely proud of her.

Whereabouts do you live and what’s it like there?

We live in Glasgow. It’s a beautiful city with friendly people. The only downside is the weather – Deacon Blue’s Raintown is very apt if you’re old enough to remember the iconic album cover.

Do you consider you’ve achieved Financial Independence and why?

I wouldn’t say I’m financially independent just yet. I’m getting closer, but not quite there.

My goal is to retire before 60, not to hit a specific number. For me, it’s more about having time to spend with friends and family, which feels far more valuable than chasing a bigger bank balance. At this stage in life, I’m choosing to prioritise time over money.

So you’re obviously not yet Retired Early…

No, I’m still working and I enjoy my current job in financial services.

My wife retired at 55 due to ill health and is no longer able to work. This has significantly influenced my approach to retirement. Rather than working longer to provide more financial security, it’s inspired me to retire before 60 so that we can spend more time together whilst we’re both fit and able to enjoy life together.

For me, time spent with your partner isn’t the shared hours. It’s the ordinary moments that become your favorite memories.

When do you think you’ll call it FIRE?

I’m hoping to retire in the next five years or so.

Assets: pensioned-up and mortgage-free

What’s your current net worth?

Our combined net worth is around £1.7m.

What makes up your net worth? Are there mortgages or other debts, too?

Our main assets are:

- £500,000 family home in Glasgow

- £300,000 flat in Edinburgh

- £100,000 in a stocks and shares ISA

- £800,000 in pensions from various employers

- We don’t have any mortgages or debts.

The Edinburgh flat was originally bought as both an investment and a lifestyle choice. It made sense at the time, as I was working in the city and wanted to avoid a long commute

Ironically, I changed jobs about a year later and wasn’t based there anymore –such is life!

Fortunately, the timing worked out well though, as our daughter ended up studying at Edinburgh University and used the flat during her degree. That saved on accommodation costs. After my daughter graduated we rented it out to a couple who are friends of hers, though they’re due to move out soon.

The Edinburgh property market has performed well over the past five to ten years. But I’d admit any increase in value has been more down to good luck than careful planning!

What’s your main residence like?

We live in a three-bedroom detached house in the leafy suburbs of Glasgow. After making overpayments for many years we now own it outright and have been mortgage free for ten years.

Glasgow on FIRE: a characterful city to work and retire in.

What was your thinking with the early repayments?

My initial strategy was to overpay by £50 per month. Over time increased this to circa £500 per month as my salary grew.

This approach wasn’t driven by a particular date but instead by a desire to reduce the overall term of the mortgage and associated interest payments as quickly as possible.

Over the years I believe that this approach has saved us thousands in interest payments. More importantly it did not materially impact our day-to-day quality of life, which is equally as important.

It might not have been the best financial decision, as the money could have been invested elsewhere. However it does let me sleep well at night. I think that is also an important factor.

Do you consider your home an asset, an investment, or something else?

My wife and I consider this a home not an asset or investment.

We chose it initially because of good schooling for our daughter, not to make money. Enjoying where you live for us is more important than making money.

Earning: it helps to enjoy work

What’s your job?

I work in a change and transformation role for a financial services company, leading large-scale business and tech projects to improve how we serve customers and advisers.

After more than 25 years in this industry, I’ve gained deep experience with Life and Pension products and regulatory changes, which I believe ties in closely with the FIRE journey.

It’s not often we get someone from the industry on Monevator…

While financial services often get a bad rap – especially when things go wrong – there are many moments that show the human side, too.

For instance I remember a time when we paid out a life insurance policy early so a critically-ill woman could marry her partner at short notice. Technically outside the rules – but absolutely the right thing to do.

Is navigating all the complexities easier for you from the inside?

As a DIY investor and employee, I still find the financial world full of jargon and complexity – even from the inside.

Also, digitisation has made services more accessible, but it also tempts people to tinker too much. As Steven Bartlett joked in a recent podcast, forgetting your investment account password might be the best thing you can do!

When it comes to FIRE, I’ve found that a slow and steady approach – regular investments in passive funds – offers the best chance of reaching your goals with confidence and less stress.

It might not be exciting, but it works.

What’s your annual income?

My annual income is around £100,000.

How did your career and salary progress over the years – and was pursuing financial independence part of your career plans?

When I graduated from University I started out in a software development role with a starting salary of £12,000. It felt like riches to a wide-eyed 21-year-old.

My career progressed quickly as I gained more experience in different technologies and software languages. However I soon learned that I was better at managing projects and people than programming. Since then I have been predominately in change and transformation, working for different financial services companies over the last 25 years, which I’ve enjoyed.

Did you have any advice about building a career and growing income? Perhaps something that you wished you’d known earlier?

My advice is ‘be comfortable in the uncomfortable’.

Moving jobs and roles either within a company or changing employer is the best way to learn new skills and experience. If your current role feels too comfy this can often be a sign that you are not developing or stretching yourself enough.

Secondly don’t chase money – chase opportunity.

If you’re excited about the opportunity you are more likely to do a great job. Your company will recognise this and the money will hopefully follow.

Do you have any sources of income besides your main job?

No. I work full-time, which is my only income.

My wife took early retirement due to ill-health and has a small pension.

Did pursuing FIRE get in the way of your career?

No – and I have enjoyed my career in financial services.

I only started regularly hearing the term FIRE in the UK around ten years ago and I don’t believe I’ve been actively pursuing FIRE. However regularly reading Monevator and other sites like Quietly Saving, I may have been doing it subconsciously without realising!

Saving and spending: Scottish virtues

What’s your annual spending? How has this changed over time?

My annual spending is probably around the £30,000 to £40,000 mark.

This is typically on basics like food, transport, utilities – plus one or two nice holidays a year.

Do you stick to a budget or otherwise structure your spending?

I don’t budget monthly, but my spending habits are pretty steady and I’m not one to splurge.

Growing up in a traditional Scottish family, I was taught not to buy what I couldn’t afford – and that mindset has stuck with me. I only make big purchases when I have the cash to pay in full.

I have a credit card that I rarely use, and I always clear the balance each month to avoid any fees.

How would you describe that traditional Scottish family mindset?

Both my parents retired in their 60s and live comfortably thanks to their hard work. They were great role models who passed on a strong work ethic.

That has served me well – and I’m proud to see the same values showing in my daughter, too.

I’ve always believed that money you earn yourself is far more meaningful than money that’s simply given.

What percentage of your gross income did you save over the years?

In my 20s, saving was tough. My wife and I bought our first flat at 25. A few years later we had our daughter, so family came first.

I did contribute to a pension, but only at the basic 3–5% level. Thankfully, working in financial services meant I benefited from generous employer contributions of around 10–13%.

In my 30s and 40s, I gradually increased my pension contributions to about 10%, but hitting 50 was a wake-up call.

I’d read that your total pension contributions (yours and your employer’s) should be around half your age. Digesting this rule-of-thumb pushed me into action.

Nowadays I contribute 27%, with my employer adding 13% for a total of 40%. It’s made a big impact on my pension growth.

The lifestyle adjustments have been minor – cutting back on extras like holidays and car upgrades – but worth it to stay on-track for retirement before 60.

In hindsight, starting earlier would have helped, but I’m glad to be making up ground now. A few sacrifices feel like a small price to avoid working extra years. It’s a trade-off I’m happy with.

What’s the secret to saving more money?

Saving is a habit. I put money away into a different account as soon as I get paid. I don’t touch this for day-to-day expenses. This allows me to enjoy the rest guilt-free.

Do you have any hints about spending less?

Don’t buy what you don’t need and be careful with day-to-day spending habits.

That daily coffee from Costa may be nice every morning. However it could be costing you £600-£700 per year, which could be used for something more productive – or indeed fun!

Do you have any passions or hobbies that eat up your income?

My wife and I love live music and regularly attend concerts in Scotland and travel across the UK – or even abroad – to see our favorite bands.

One highlight was Adele in Munich last year. That was truly an amazing experience both musically and visually with a 220-meter screen.

We are also football season ticket holders and have been for many years. This has been a rollercoaster – thanks to events both on and off the pitch – but we still love going to home games on a Saturday.

Investing: towards simplicity

What kind of investor are you?

Well, a former boss once told me, “I want my money to work as hard for me as I did to earn it,” and that mindset really stuck.

So I’ve always managed my own investments and never used a financial adviser.

Over time, my approach has shifted. I’ve gone from trying to beat the market with active investing to preferring a more passive strategy, which suits me better.

I’m fully invested in equities, and now have less than 10% in active funds.

Do you use any of your fellow professionals?

Recently I had a call with a financial adviser through a free service from my employer to see if I’m on track to retire in the next five years.

The adviser was great, and after doing some personalised retirement modelling, it was reassuring to learn I’m on the right path. It was validating – and honestly a relief – to hear that many of my investment choices aligned with his own. Particularly after being a DIY investor for 25-odd years.

To be honest this experience has also changed my perception on paying for financial advice. I’d now consider looking for a financial adviser to help me set-up a retirement plan once I get closer to FIRE.

What was your best investment?

Property has been our best investment. My wife and I bought our first Glasgow flat in our mid-20s and moved a few times as our family grew. Each move brought a good increase in property value, which helped us move up the ladder – though we’d say it was more luck than strategy.

We’ve never focused on renovating to sell, but instead chose homes based on location over style. Fortunately, the areas we picked became more desirable over time. That boosted their value.

We know we’ve been lucky – especially with how much harder it is now for younger people to get on the property ladder. Many of our friends’ adult children are still living at home. They have little chance of buying unless they get extra help.

Did you make any big mistakes on your investing journey?

Definitely! Managing your own investments means you make mistakes and when it’s your own money you learn fast.

A few hard-won lessons come to mind:

Chasing winners – I used to jump on whatever active fund was flying high that month — only to watch it crash the next. I’ve since learned slow and steady wins the race. (No pun intended on your namesake portfolio!)

Panic selling and meddling – I’ve trained myself to ignore big market swings (like the Q1 drop this year) and stick to the plan. Too many people I know panic and sell the moment their fund dips 10%. I’ve also stopped constantly switching funds. It only adds stress and fees.

Avoid what you don’t understand – I tried crypto a few times and realised it felt more like gambling. Seems to me the only consistent winners are the platforms, who earn fees regardless of whether you gain or lose.

Emotional investing – I’ve held onto losing funds hoping they’d bounce back, only to regret it. Sometimes you’ve just got to cut your losses and treat it as tuition fees for learning the ropes.

What’s been your overall return, as best you can tell?

On average, my pensions and stocks and shares ISAs see around 9% annual growth, depending on market conditions. My best investment so far has been the Legal & General Global Technology Index Trust, which has grown by over 50% – a great return over the years.

I’m mostly invested in US funds, which have done well over the past decade, but I also make sure to include other regions to stay diversified.

It might not be the perfect allocation, but it suits me and I’m happy with the results.

When I reach FIRE, my plan is to use income drawdown from my pensions rather than buy an annuity, as it offers more flexibility. I’ll keep my ISAs as a backup or for topping up income if needed.

How much have you been able to use your ISA and pension allowances?

At present, I’m putting around £40,000 to £50,000 (combined employee and employer contributions) annually in my pension. This consumes about 27% of my salary.

I typically also save £1,000 per month into my ISA as a regular habit and try to fill up to £20,000 each tax year, if I have money available. However this isn’t always possible.

To what extent did tax incentives and shelters influence you?

As a higher-rate tax payer in Scotland I’m keen to ensure that my investments are as tax-efficient as possible. So I save heavily in pensions to reduce tax.

But I also save into the ISAs to provide some financial flexibility and protect me in case the government decides to change pension or ISA rules in future.

How often do you check or tweak your portfolio?

I check my portfolio weekly and track performance in a big Excel spreadsheet I’ve built over the years.

It’s something I genuinely enjoy. It keeps me motivated and helps me maintain a growth mindset, whether I’m seeing gains or spotting opportunities during a dip.

That said, I don’t have a specific investment target. It’s more about using the data as feedback and staying engaged.

I know weekly tracking might be too frequent for some, but for me, it’s a positive habit that keeps me focused and doesn’t do any harm.

Over the years I have developed good self-discipline and I avoid tweaking my portfolio too frequently. I occasionally make changes – once or twice a year – to rebalance. However I’ve sometimes gone a year or two without making any changes at all.

Moving the majority of my portfolio into passive funds has also helped me avoid making too many tweaks or changes.

Wealth: enjoying working towards a rich life

We know how you made your money, but how did you keep it?

Big trees grow from little acorns and even now I still regularly save and invest regularly as a habit. One challenge I recognise though is should you change this habit when you move into de-accumulation?

It would be great to hear views and experiences from other Monevator readers on this topic. I expect this to be an issue for me, having been in the saving and investing mode for many years.

Which is more important, saving or investing, and why?

Both is the pragmatic answer. But if you pushed me to choose one I would say investing is more important. Where you put your money can make a huge difference in the financial returns, particularly over the longer term. At my stage in life I’m laser-focused on where I’m invested and the performance of my assets.

I appreciate that this is not the norm. When I speak with friends and family about pensions and what funds they are invested in, they typically look at me like I’m speaking a different language. So I recognise that I am an outlier.

Do your goals have a timeline?

My goal is to retire in five years’ time.

Has anything unexpected got in your way on the path to financial independence?

Over the years I’ve experienced many twists and turns, both in terms of unplanned career changes due to market forces and investment mistakes. But I’m pleased with how things have panned out to date.

The journey is as important as the destination. I’ve learned to enjoy the ride so I feel contented.

Do you have any other financial goals?

My key financial goal is to be able to do what I want when I retire and not be restricted – within reason – by money. Having the freedom to be able to go out for a good meal with friends or attend the theatre without having to check my bank balance first is important and a nice feeling.

For me financial goals are about having the freedom to do what you want when you want. We can always have more money but never buy back time.

What would you say to Monevator readers pursuing financial freedom?

A few friends and colleagues have already retired, and through our chats, one message keeps coming up: having a clear purpose in retirement really matters.

It needs to be more than just holidays or hobbies. It’s about finding something meaningful that keeps you motivated once the daily work routine stops.

One of my close friends has embraced this brilliantly, spending his time writing children’s books in winter and creating an award-worthy garden in summer – all purely for the joy of it.

After working most of my adult life, I’m really looking forward to the freedom retirement brings. I haven’t fully figured out my own purpose yet. But I’m excited to explore that as my FIRE date gets closer.

Tidying up

When did you first start thinking seriously about money and investing?

I started reasonably early. I even took out a personal pension in the early 1990s before the introduction of auto-enrolment.

Since then I have always been interested in money and investing, which I think is a good Scottish trait!

Did any particular individuals inspire you to become financially free?

The contributors to Monevator and the community that engages in the comments are my inspiration, particularly as Monevator is focused on a UK audience.

It’s a reminder that you’re not alone. Many of us are thinking and feeling the same things.

Can you recommend any other favourite resources for anyone pursuing the FIRE dream?

I’m a big follower of Steven Bartlett. I regularly listen to his Diary of the CEO podcast when travelling to and from work. Many of the guest speakers on investing and more recently Artificial Intelligence have been fantastic.

What is your attitude towards inheritance?

I will start to consider inheritance tax more closely once I FIRE – I want to ensure that my wife and daughter are looked after.

The recent inheritance tax changes are frustrating and feel counterproductive for someone who has worked their whole adult life. However let’s not get into politics…

What will your finances ideally look like towards the end of your life?

My view is simple. Enjoy your money while you can! Life’s short, so make the most of it with friends and family doing what makes you happy.

And on that note… I think it’s your round, The Investor!

Indeed – my thanks to WeeScot for taking the time to share his story with us. It’s a good reminder that you don’t need to start a side hustle or run a business or move to the mountains to achieve your goals (not that there’s anything wrong with those either…) and that conventional wisdom is wise for a reason. Questions and constructive feedback are both welcome, but anything bad-tempered or nasty will be deleted. WeeScot is a long-time Monevator reader, but he’s not a regular commenter – let alone a battle-scarred blogger like me. Be sure to read our other FIRE-side chats.

With Trump tariffs feeding fears of a US economic slowdown and concerns rising about an AI-fuelled stock market bubble, now may not seem like a good time to invest.

Perhaps it’d be best to keep your financial powder dry? To wait until things calm down and the world feels a little more stable?

That makes perfect, intuitive sense – until you step back and look at the bigger picture.

In the long run, equities go up

The bigger picture looks something like this: the most reassuring chart in investing…

Data from JST Macrohistory 1, The Big Bang 2, and MSCI. August 2025. Real total returns in GBP.

The chart shows inflation-adjusted, World stock market returns surging through 125 years of upheaval, transformation, and occasional catastrophe.

Anyone who remained invested throughout that period would have earned 6% per year on average (over and above inflation).

That’s despite suffering the massive financial shocks that periodically interrupt the rise of equities.

The World’s worst stock market crash was the 52% real terms decline that unfolded during the 1973-74 Oil Crisis.

World War One and the Dotcom Bust inflicted similarly large losses.

But each setback was temporary. Progress resumed, just as it did after the Global Financial Crisis and Covid.

Investing is one damn thing after another

But what about now? Doesn’t the incessant drumbeat of uncertainty and looming peril suggest it would be better to stay on the sidelines for a while?

Time will tell. But the world is always troubled.

Here’s a catalogue of threats that menaced investors in the years that followed the Global Financial Crisis:

- 2010 – Greek bailout, The Flash Crash

- 2011 – EU debt crisis, double dip recession, US debt downgrade

- 2013 – The Taper Tantrum, US government shutdown

- 2015 – Chinese stock market crash

- 2016 – Brexit referendum, Trump election, Fed rate hike jitters

- 2018 – US-China trade war, quantitative tightening

- 2019 – Inverted US yield curve, Great Stagnation alarm

- 2020 – Covid, running out of Netflix shows in lockdown

- 2021 – Covid, Evergrande liquidity crisis, global energy crisis

- 2022 – Inflation surges, Russia invades Ukraine, the energy crisis deepens, rising interest rates prompt recession worry

- 2023 – Financial contagion fears triggered by Silicon Valley Bank collapse, stagflation warnings

- 2024 – US-China tensions, S&P 500 overvaluation disquiet, US election uncertainty

- 2025 – Trump tariffs, AI bubble anxiety, government debt concerns, currency debasement fears

Despite all that, World equities grew 251% in real terms from 2010 to 2024, and the market reached new highs in 2025.

Here’s how that looks if you bought and held a World equities ETF from 2010 until the time of writing:

Data from JustETF. August 2025. Nominal total returns in GBP.

(Note: the ETF chart shows nominal returns. The real return measures how much your wealth has grown after stripping out the impact of inflation.)

The World equities real return averaged almost 9% a year over this period. In other words, the past 15 years has been an incredible time to invest – even though you had to endure constant worries and some painful downturns to profit.

Stock market returns are often earned the hard way.

Pain is why you are paid

It’s because equities have proven resilient over time that long-term investors stay in the market, regardless of short-term wobbles.

Trying to predict the perfect entry point often means missing out on growth because there is never a ‘safe’ time to invest.

Indeed, many of the market’s biggest opportunities have followed its most dramatic falls.

Prices rocket when investors eventually realise they overreacted to the last shock.

But human psychology guarantees you’ll fail to grasp those moments if you don’t upgrade your mental firmware from the basic Fear & Greed 1.0 package.

Greed sucks us into rising markets. Think 19th Century Gold Rush or 21st Century Crypto Bubble. We’re like moths to the money flame.

Then we get burned. Fear takes over and instructs us to: “Freeze! Just chill for a while. Let’s wait and see what happens.”

And then all of a sudden the market marches on without us. We miss most of the rally…

…until eventually greed overwhelms our fear again. Dragging us back into the action, because nobody wants to miss the last train to Fat Stacks City.

This is the chimp version of scissors, paper, stone. Greed beats fear. Fear beats greed. We flip-flop in time to the market’s beat, but out of tune with the opportunity.

Playing the market this way only increases the risk of buying high and selling low.

But wading in when your instincts scream “Danger! Danger!” will increase your odds of buying low and selling high.

As Warren Buffett puts it: “be fearful when others are greedy and greedy when others are fearful.”

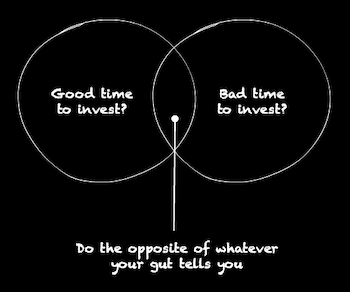

Is now a good time to invest?

Now is as good a time as any to invest because for the vast majority of people it’s time in the market that counts, not timing the market.

In retrospect, the historic traumas charted above proved brief downward squiggles on the great graph of historical returns.

Progress is not inevitable, of course. But we shouldn’t lament the lack of guarantees either.

Uncertainty is the gunpowder that propels our future returns. It’s exactly because of the risk of loss that investors demand the prospect of higher returns from equities.

No-one gets paid for betting on a sure thing. But buying a stake in the continued progress of humanity – and its main engines of productivity – has paid off for the past 300 years.

If you believe we’re not done for yet then owning a diversified portfolio of equities is a wise investment, alongside other useful asset classes.

Use techniques like pound cost averaging to work your way into the market gradually and to benefit from the dips.

Check out our guide on passive investing to develop a strategy that works for you.

Take it steady,

The Accumulator

p.s. This article updates an older version from a few years back. We’ve left the existing comments below, as they provide interesting perspective and context as time goes by. But please do check the dates before replying.

- Òscar Jordà, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor. 2019. “The Rate of Return on Everything, 1870–2015.” Quarterly Journal of Economics, 134(3), 1225-1298.[↩]

- Dmitry Kuvshinov and Kaspar Zimmermann. 2021. The

Big Bang: Stock Market Capitalization in the Long Run. Journal of Financial Economics,

Forthcoming.[↩]