People get muddled when they think about their own home in financial terms. This extends to a repayment mortgage used to buy a property.

Mental accounting – also known as ‘bucketing’ – is what causes this discombobulation.

Fact is we tend to think about the value of money differently, depending on where it comes from and where it ends up.

Mental accounting involves putting money into different mental accounts – or buckets – as a crutch in our financial thinking.

Bucket or bouquet?

For example, a 40-something friend tells you they have “no savings”.

Worried, you make plans to run the London Marathon dressed as a muppet on their behalf.

But then you discover they’ve been paying into a pension for 20 years.

Your friend discounts this substantial pension asset, probably because it can’t be accessed for another couple of decades.

Ignoring a pension like this is a mental shortcut. And to be fair it’s true that your friend can’t get cash from their pension if the boiler blows up.

It might also be easier for them to mentally treat pension contributions from their salary as more like a tax than savings. Filing such payments under the same ‘Inevitable’ label as taxes may help them stay committed.

Perhaps the thought that they have no savings could motivate them to build an emergency fund, too.

But still, the statement dramatically misrepresents their true financial position.

If they genuinely had no savings they’d be on-course to rely solely on a state pension in retirement. They’d be well-advised to take action – yesterday.

Or maybe someone decides to work out how to split their saving between their ISAs and pension – perhaps with an eye on early retirement.

When they do their sums their pension assets will suddenly appear in a ‘Live and Very Real’ bucket in all their glory. Previously they were clouded in a mental fog of their own creation.

The property puzzle

My favourite example of dodgy mental accounting is how even financially literate people think the home they own is somehow not an asset or an investment.

You can strive for hours to illustrate with logic and counterfactuals that their home is most definitely an asset AND an investment.

But this is a mental wall that Fred Dibnah would struggle to blast through.

Again, such self-delusion can be helpful.

Maybe because they don’t think of it as an asset, most people don’t trade their property or fret about small price moves. That helps their own home become the best single investment the typical person ever makes.

That’s the case even though their thinking is wrong! Oh the irony.

Admittedly the situation with a repayment mortgage is a bit more subtle.

Save your repayment mortgage

I was reminded of the confusion about repayment mortgages by comments on The Treasurer’s recent article on the savings rate.

Many – perhaps most – people tend to think of a repayment mortgage as a monthly expense.

They know they will own their home outright at the end of the mortgage term. (Weirdly even then most won’t consider it an asset. Harrumph!)

But along the way they see mortgage repayments as an expense that they mentally bucket just as they would rent.

They therefore don’t consider their repayment mortgage to contribute to their savings rate.

However repaying a mortgage is a very different proposition to paying rent, at least from the perspective of the person living in the house (as opposed to any landlord in the mix).

That’s because your monthly repayment mortgage direct debit consists of two parts.

- One part sees you pay interest you owe to the bank for lending you the money (via your repayment mortgage) to buy a home in the first place.

- The other part involves paying off some of the outstanding loan. These are the payments that will eventually reduce your mortgage debt to zero, and see you own the property outright.

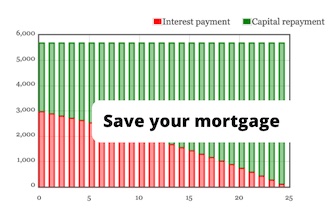

The following graphic from our repayment calculator breaks down these two parts of a repayment mortgage:

This shows a £100,000 repayment mortgage charging 3% paid down over 25 years.

You can see how in the early years you’re paying off more interest than capital. Towards the end though, capital repayment – effectively savings – makes up most of the payment to your bank.

Cutting the expense account

Strip out the mental accounting, and the two components of your monthly mortgage payment are two different kinds of money transfer:

- The interest payments are an expense. They are the cost of having a mortgage.

- The capital repayments that reduce your outstanding mortgage are savings. They reduce your debt and increase your net worth.

Incidentally, to nip another bit of mental accounting in the bud, the market value of your house as prices fluctuate has nothing to do with any of this.

Your house is an asset and an investment that is worth whatever someone will pay for it.

This is true however you financed it – with cash, an interest-only mortgage, a repayment mortgage, or by blackmailing the previous owner with saucy photos extracted in a sting operation involving a sex worker with a knack for hidden cameras.

Your repayment mortgage in contrast is a debt that you are paying off over time. Nothing more and nothing less.

Same difference

Still not convinced? Let’s illustrate further by thinking about someone like me who has an interest-only mortgage, rather than a repayment job.

As the name indicates, every month with my interest-only I pay interest (only…) to the bank.

I am not repaying any of the outstanding loan.

Don’t worry, my bank is well aware of this! The deal is I’ll repay all the debt I owe in a couple of decades time. Until then, I simply pay the interest.

For the sake of argument, let’s simplify and imagine I have a £100,000 interest-only mortgage as well as £10,000 in a cash savings account.

My situation:

- Cash savings: £10,000

- Interest-only mortgage: -£100,000

- Balance: -£90,000

Now let’s imagine Monevator wins a prize for Most Waffley But Charming Financial Blog of the Year. Along with the bronze gong that I ship to my co-blogger because I hate clutter, I get £10,000 sent to my current account.

Let’s say I have just two choices as to what to do with this £10,000. (I’m too boring sensible to spend it on bubbly and financially loose playmates).

I could put the £10,000 into my savings account.

Alternatively, I could make a one-off payment to my bank to reduce my outstanding mortgage.

In the first scenario, I add £10,000 to savings:

- Cash savings: £20,000

- Interest-only mortgage: -£100,000

- Balance: -£80,000

In the second scenario, I make a £10,000 payment to reduce my mortgage:

- Cash savings: £10,000

- Interest-only mortgage: -£90,000

- Balance: -£80,000

As you can see can see, in both instances I end up with a negative balance of £80,000.

Indeed you can think of an outstanding mortgage as a savings account that starts deeply in a hole. As you save money by repaying your mortgage, you move this ‘negative savings account’ towards breakeven.

Save as you go with a repayment mortgage

How you think about a repayment mortgage is not just pedantry. It can sway the financial decisions you make.

For example, if you think of a repayment mortgage balance as another form of savings account, then you can compare the interest rates between it and your conventional cash savings accounts.

Say your mortgage charges 2.5% and your cash savings pay 0.5%.

You don’t need a calculator to see that on those numbers you’re better off paying down your mortgage with any spare cash allocated towards savings.

On the other hand, a mortgage repayment locks your money away. (Unless you have an accessible offset mortgage, which makes explicit the link between savings and mortgage repayments).

Remembering this you might not make a mortgage repayment with that cash windfall, because you want to bolster your emergency fund instead.

Of course, this being Monevator many of you will be thinking you’d invest any spare cash into the stock market.

And of course that’s an option – but it’s a different kind of saving.

Like your own property (and as opposed to your mortgage), an index fund, say, is an asset and investment. Treat it accordingly.

Happy saving!