This article can be read by selected Monevator members. Please see our membership plans and consider joining! Already a member? Sign in here.

This was to be a Mavens member post explaining how commodities work in a portfolio and why that time is now. But given how fast events are moving, we’ve pulled it forward to give non-members a taste of what’s behind our paywall. Please do consider signing up for more!

Is it me or are the 1970s back? Apparently Claudia Winkleman was spotted in flares, plus there’s an oil crisis inbound. (You might have noticed?)

Personally I can’t wait to queue around the block for petrol and use candles for lighting again.

But while it’s a bad time to be the owner of an ICE 1 car – or a leader of Iran – it’s an excellent time to be a commodities investor.

The vertical take-off vehicle in the chart below is the sight of a natural gas ETC 2 going up like an interceptor – once the missiles started flying. See the light blue line:

Chart from justETF. March 2026. justETF charts show nominal total returns (GBP).

The gas futures tracker is 92% to the good since 2 March (the first day of trading after the war began).

It’s as if people think bombing gas fields is gonna put up the cost of energy or something.

Whizzing along at a slightly lower altitude is Wisdom Tree’s Brent Crude Oil ETC (yellow line, 54% gain).

Finally, UC15 – my fave broad commodities ETF – flies under the radar with an 11% gain (green line).

Run for cover

The next chart contrasts the response of equities, gold, bonds, money market, and commodities to the current crisis:

Yes, every other asset class is retreating like a Dubai-domiciled influencer bar docile cash (orange blip) and the aforementioned commodities (the investment that loves it when physical stuff gets scarce).

But don’t worry, this is not a “Commodities Ra-Ra!” post.

The point is that DIY investors are naturally sceptical about commodities. The asset class is sickeningly volatile and many recall how it fell into a doom spiral after the Global Financial Crisis.

Yet the counterpoint is that commodities are often upstanding – and sometimes outstanding – when other asset classes hide under the table.

Especially during the supply shock crises that wrack the world periodically. Which – unless Trump steps off his golden escalator soon – is exactly what the current contretemps could trigger.

Hopefully sanity will prevail. But it can take a while before the hard-of-sanity see sense.

That’s why commodities deserve another look. Especially given how other assets struggle to cope with highly inflationary conditions. Gold may perform but it’s a highly unreliable bedfellow (as its current 12% drop-off since 2 March is currently reminding us…)

Commodities: the good, the bad, and the downright ugly

I’m not a stooge in the pocket of ‘Big Raw Materials’ who pay me in bushels of wheat for every new convert. Honest!

What follows is intended as a relatively quick and digestible account of the reasons why you might want to hold commodities as a strategic diversifier. It includes reasons why you might skip it as well.

Just so you know where I’m coming from, I don’t advocate dipping in and out of Brent Crude ETCs depending on how histrionic Pete Hegseth appears today.

However, I do hold a broad commodities ETF (Ticker: UC15) as a portfolio diversifier and bulwark against inflationary shocks.

BCOM again

Now, about that commodities bear market…

The commodities index I benchmark against (BCOM) has still not recovered the market high it achieved in June 2008.

From that perspective, the asset class has spent almost 18 years underwater! That’s absolutely hideous if you were sucked in by the Noughties’ run-up in commodities. (An ascent often attributed to the rapid growth of China and other emerging economies at the time.)

However commodities look perfectly respectable from other starting points.

For instance, here’s the annualised returns over the past ten years for the main asset class ETFs I charted earlier in the article:

| Asset class | 10-yr annualised return (%) |

| Gold | 14.6 |

| World equities | 12.9 |

| Broad commodities | 10.1 |

| Money market | 2 |

| Global government bonds | 0.3 |

Nominal annualised total returns (GBP) from justETF, 20 March 2016-20 March 2026. I’ve replaced iShares Global Government Bond ETF (IGLH) with XGSG because IGLH does not have a ten year track record. Both are GBP hedged.

On this view, commodities don’t look so bad. In fact, they’ve done extraordinarily well during a period in which gold and equities have been blinding.

Moreover, they’ve produced a great result for a diversifying asset. There’s not much point holding raw materials to deflect rogue waves of inflation if it’s a deadweight the rest of the time.

(Reminder: for real returns, subtract average UK inflation of about 3.5% for the period.)

Commodities for the long run

The long-term real return of broad commodities stacks up nicely, too:

Data from AQR 3, Summerhaven 4, BCOM TR, MSCI, Before the Cult of Equity 5, A Century of UK Economic Trends 6, Robert Shiller, The Big Bang 7, Bank of England, and ONS. March 2026. Monevator sourced returns in this article are inflation-adjusted annualised total returns (GBP).

World equities index – Pre-1970 World equities monthly returns are not available in the public domain. To facilitate long-term comparisons, I’ve used market-cap weighted UK and US monthly returns to stand in for World equities from 1900 to 1970. The MSCI World equities index covers the period from 1970 until the present day. The UK / US market cap varied from approximately 55% to 84% of World equities up to 1970.

The long-run view shows that commodities are not a basket case. Indeed, their average return is more than fine (and compares favourably with other defensive diversifiers):

- Broad commodities (blue line in chart above): 4.6% annualised real total return (GBP)

- World equities (red line): 5.9% annualised real total return (GBP)

My chart annotations spotlight commodities’ handy habit of peaking when inflation runs amok. Unsurprisingly really, because they’re the feedstock of the price index itself.

As such, the historical record shows that raw materials are the asset class most likely to beat inflation when it’s eating your purchasing power alive.

Two caveats though.

Firstly there are some enormous bears lurking in the commodities return undergrowth. We’ll wince at those shortly.

Secondly, the chart’s biggest commodity booms are associated with the early Twentieth Century industrialisation of the US (see 1900 to 1909 on the chart) and the double-hit of post-war inflation and reconstruction (1945 to 1950).

If you don’t think the transition to a decarbonised economy built around the electric tech stack will have quite the same impact, then we should discount commodities’ long-run average growth rate.

For example, fund manager Research Affiliates’ offers 3.1% as its 10-year real expected GBP return for commodities.

Either way, on balance I think it’s reasonable to believe commodities can make a positive contribution to the growth of a diversified portfolio.

Material gain

For my money, the real win isn’t the future return of commodities. It’s the damage limitation role they can play when equity performance is grim.

The next chart contrasts World equities and commodities returns during the biggest stock market routs of the past 126 years:

On average, commodities outperformed equities by 46.1% per bear. Remember that’s an inflation-adjusted return, too.

As you can see, commodities didn’t always produce a positive return. However, they did deliver a better return than equities. Every time.

The table below offers a quick summary of the action above:

Diversification score card

| Equity bear market performance | World equities | Commodities |

| Positive return | 0 | 4 |

| Better negative return | 0 | 5 |

| Best overall return | 0 | 9 |

Pretty compelling, eh? The table is telling us that commodities always improved portfolio performance when investors desperately needed a life belt to cling onto.

Indeed I think I should write up a post repeating this score card for the other key portfolio diversifiers available to us – and that can also be tested against a diverse range of economic conditions. Namely, cash / money market funds, government bonds, and gold.

Without checking, however, I bet the others will struggle to do as well as commodities. Simply because runaway inflation is the spark most likely to torch UK investors’ portfolios.

This is at odds with the US downside experience, which is dominated by demand-led recessions like the Great Depression.

That’s partly why commodities have been given short shrift. They don’t thrive when demand collapses.

You can see in the chart above that the clamour for copper and cows evaporates during Big League liquidity crises. Witness commodities’ negative returns booked against the Global Financial Crisis, the Japanese asset bubble implosion, and the slump-daddy of them all, the Great Depression.

Thankfully, government bonds usually ride to the rescue during those times of darkness.

But commodities were deemed unnecessary when DIY investing took off because memories of rampant inflation had faded. And Americans hadn’t suffered purchasing power cuts on the scale that scarred previous generations of Brits either.

Totally oresome

The next chart gives you the gory details on how often commodities have stepped up when equities have fallen down:

The red ravines represent the occasions that equities fell from their previous high – including the death plunges we saw in the previous chart.

The icy peaks show the subsequent rolling one-year commodity real returns.

Blue swells that rise above the 0% line show commodities actively counterbalancing equity drops with a positive return over the next 12-months.

But if the blue line tunnels down, then it exacerbates the situation if it bores through the red floor.

Otherwise, negative commodity returns reduce the drag factor so long as the blue losses don’t exceed the red.

The higher and more frequently the blue waves rise above the red depths, the better.

Once again, this is a sterling result, but the chart also warns us that commodities don’t always hedge your losses.

The hard stuff

As grizzled commodities investors know, this is an asset class that can batter you with devastating combos of negative returns.

The next chart retells the commodities growth story, but it highlights the warts ‘n’ all:

Obviously the angry red areas are the down years – or decades.

Not so bad? Not so fast!

The chart is based off softie nominal prices, because that best represents our lived experience as investors.

However, the next chart shows the real deal – because it’s inflation-adjusted returns that put food on the table:

Oh my! This is the ugly I mentioned earlier.

By this light, the history of commodities returns is dominated by nearly four double lost-decades. 8

In other words, commodities sunk deep underwater for around 80 of the last 126 years. So there’s that.

Shovel it

If the boom and bust nature of commodities puts you off for life, I don’t blame you.

Reader, I invested. Not because I love pain but because commodities can bulk up when equities and bonds wane.

My target asset allocation is 10%. However I only bought 5% initially, my plan being to take advantage of raw materials’ inherent volatility in the future.

That is:

- I’ll buy more when my commodity ETF plummets.

- I’ll sell when the ETF’s price rockets.

Hopefully that rebalancing schedule will enable me to turn a profit on my commodities exposure. Or at least recover more rapidly when the next equities’ bear strikes.

Super psyched

Incidentally, the mighty leg-ups on the commodities’ growth chart led to the development of the commodities ‘super-cycle’ theory.

The theory posits that commodities go on a tear during periodic transformations of the world economy. Whereas the subsequent slumps are the product of over-investment in solving commodity bottlenecks.

If that pattern holds then we’re still on the upswing from the depths of the last commodities’ depression. It began when easy money dried up during the Global Financial Crisis.

It’s a macroeconomic story arc that could help explain the excellent 10-year returns we saw for commodities earlier, and Research Affiliates’ chipper 10-year expected returns forecast too.

But what matters to me is that there’s something in my portfolio that reacts to inflation like Popeye on spinach.

When that happens I’ll sell up and buy breathing space for my equities to recover.

Take it steady,

The Accumulator

P.S. For more on commodities, check out our five-part series:

- Part one explained how commodities investing works

- Part two covered commodities’ long-run returns

- Part three examined whether commodities enhanced portfolio returns

- Part four investigated whether commodities really are a good inflation hedge for UK investors. [Members post]

- Part five delved into my ‘best commodities ETF‘ picks

P.P.S. “What follows is intended as a relatively quick and digestible account…” Yes, I failed. Again.

- Internal combustion engine[↩]

- Exchange Traded Commodity fund[↩]

- Levine, Ooi, Richardson, Sasseville. 2018. “Commodities for the Long Run.” FAJ.[↩]

- Bhardwaj, Janardanan G, Rajkumar, Geert Rouwenhorst K. 2020. “The First Commodity Futures Index of 1933.” Journal of Commodity Markets. 2020.[↩]

- Campbell G, Grossman R, Turner JD. 2021. “Before the cult of equity: the British stock market, 1829–1929.” European Review of Economic History. 25. 10.1093/ereh/heab003.[↩]

- Chadha J, Rincon-Aznar A, Srinivasan S, Thomas R. “A Century of UK Economic Trends.” ESCoE, NIESR and Bank of England.[↩]

- Kuvshinov D, Zimmermann K. 2021. “The Big Bang: Stock Market Capitalization in the Long Run.” Journal of Financial Economics, Forthcoming.[↩]

- During my research I discovered that a ‘vicennium’ is the noun for 20 year spans. But I’m relegating this knowledge to the footnotes, because anyone who bandies around words like vicennium needs to have a word with themselves.[↩]

What caught my eye this week.

Well he’s achieved what the simultaneous fears of an AI bubble and the fear that AI would take all our jobs couldn’t quite manage.

For a moment yesterday, US President Donald Trump had sent the Nasdaq market into correction territory:

Of course it’s true that markets – especially US markets – have been cruising for a bruising for ages.

But still, we haven’t seen a decline like this since Trump last took his agenda to the global stage, when he was throwing around (figurative) bombshells back in April 2025 on his ill-fated Liberation Day.

Most of the tariff hullabaloo has since been unwound, either by Trump’s own backpedaling or the intervention of the US courts. And the final bill for his economic illiteracy has largely been paid by the US taxpayer, in the form of US firms and consumers.

It would be nice to think the Iran conflict will end the same way, and soon.

It’s possible. Despite Trump having said hours earlier that he wasn’t interested in a ceasefire with Iran, I woke to news that some tweet or segment from a Fox News pundit now had him pondering winding down his latest campaign.

Top Trump

We’ll have to see how Trump feels tomorrow. Nothing else will matter.

US politicians have been supine while enabling Trump’s second term antics – which is why he so swiftly went from abducting a head of state to at least taking the cellophane off the manual marked World War 3 – and he doesn’t appear bothered about the average US voter, either.

So despite the war cementing Trump’s status as the most unpopular president of all-time, so far he’s not for TACO-ing.

And yet the bombing potentially going into a fourth week is already surprising, given that the White House war aims appear to have been met:

- The casual decapitation of another sovereign regime

- Plenty of exciting new downloadable content for fans

- Nobody moaning – or reading – about ICE shooting US citizens anymore

But what about the ‘complete obliteration’ of Iran’s capacity to develop nuclear weapons, you say?

Don’t be silly. Trump assured us he’d already done that last year.

No doubt he’ll completely obliterate it again next year if he needs to.

The sick man of the G7

Falling stock markets are one thing, and arguably not even unwelcome. They come with the territory.

The unmooring of the world’s hegemonic superpower is another, more frightening thing. At the far end of that storyline is a long global conflict just one mistake away from the four-minute warning.

And slap-bang in the middle is good old Blighty, always ready these days to get the worst of it:

Other consequences that even those who complain that ‘politics’ – if that is what we’re witnessing – has no place on an investing website like Monevator will concede are relevant include a near-50% rise in the oil price to $100, and a direct hit on UK households:

-

- Energy bills could hit almost £2,000 a year… – Guardian

- …as gas prices reach their highest level for three years – This Is Money

There’s little that the UK government can do in response. Not least because Rachel Reeves has bills to pay of her own. Any breathing room from lower borrowing costs has again gone for now:

If yields stay up here for long they will kibosh any economic recovery. They’ve probably already done for a spring bounce in our beleaguered housing market.

Hence the UK economy will continue to languish – at least £100bn a year smaller than it would have been if we had remained in the EU, and thus £40bn short annually of the tax receipts that might have helped make things better.

But I won’t shoot more fish in the Brexit barrel today.

Indeed one can almost look fondly on our own poundshop populist-in-chief, given that Nigel Farage can apparently satisfy his own urges for crass showmanship and self-interest by charging £100 a pop to meet the whims of white supremacists on the Cameo app, when the alternative is blowing up the Middle East.

Falling down

Unlike our own witless foray into national self-harm though, something good could actually come out of this unnecessary conflagration with Iran.

Were the regime to fall and a version of democracy to take hold, I’d be the first to cheer Iran rejoining modernity. A bigger Dubai with better museums and restaurants, or more seriously a proper grown-up country with a global standing befitting its size, resources, and storied history.

However that end does not justify these means.

Veteran anti-American leftists must look back on President George W. Bush’s laborious efforts to establish a coalition and a cause for the Iraq war as fantastical. Something more akin to the Council of Elrond in The Lord of the Rings compared to this president, who sets the Middle-East ablaze one week then mutters about ‘taking’ Cuba the next.

But maybe you’re one of those supposedly tough-minded realists who thinks we’re just seeing how the world was always run, now President Trump has bravely pulled down the curtain?

Firstly, you’re wrong. This isn’t how the Western world was run for the past 80 years. (Granted it’s how it’s sometimes run in banana republics, or under African tyrants).

But secondly, there’s nothing tough about smashing stuff up for no good purpose other than to make a lot of noise to please your base and satisfy your ego.

Hard things require hard work, as well as holding your tongue and sometimes your power.

As Canadian PM Mark Carney eloquently put it at Davos in February:

For decades, countries like Canada prospered under what we called the rules-based international order.

We joined its institutions, we praised its principles, we benefited from its predictability. And because of that, we could pursue values-based foreign policies under its protection.

We knew the story of the international rules-based order was partially false, that the strongest would exempt themselves when convenient, that trade rules were enforced asymmetrically. And we knew that international law applied with varying rigour depending on the identity of the accused or the victim.

This fiction was useful, and American hegemony, in particular, helped provide public goods, open sea lanes, a stable financial system, collective security and support for frameworks for resolving disputes.

The rules-based order that some now scorn is exactly why the West enjoyed many decades of relative peace and prosperity.

But it’s also why, for instance, China was able to pull a billion people out of poverty, and why – and always most importantly and easiest forgotten – why the post-nuclear horror film Threads is still a work of fiction, as opposed to what happened last Tuesday.

Won’t anyone think of the despots?!

You might say the rules-based order was a lie that didn’t give Vladimir Putin or Kim Jong Un – let alone Saddam Hussein or any number of Central American dictators – a fair shake.

Fair enough, but at least be clear who you’re advocating for.

Similarly, you might find it refreshing to hear the leader of a nuclear superpower calling his NATO allies cowards for not diving into the latest mid-season plot twist for the Trump White House.

But don’t complain when every other country starts pointing nuclear missiles at their neighbours as a consequence.

As Janan Ganesh points out in the FT [Paywall] this week:

As of last month, there is for the first time in over half a century no binding agreement to limit nuclear arms between America and Russia, which have the world’s two largest arsenals.

What is this?

A wave of recklessness? Perhaps, but also a natural response to events.

If the worst that results from this circus is higher prices at US gas stations and another 20% down on the S&P 500 then we will have gotten off lightly.

But I’m inclined to worry that the unravelling of the post-WWII Western consensus will – eventually – come with a higher and bloodier bill.

Of course the United States is far from the first empire to grow fat, hubristic, and ignorant at the height of its power.

But it is the first to be run by a former TV game show host.

No wonder Wheel of Fortune, Jeopardy, and The Price Is Right seem to be the closest we have to a doctrine in Washington these days.

Housekeeping: email issues

It seems more Monevator emails have been going into spam and junk folders than even my critics’ complaints about my forays into politics would warrant.

The issue may be that I’ve been using URL shorteners to tidy up lengthy link addresses. So I’ll be cutting back on that.

Anyway if you’re reading this article on the website but you’re also an email subscriber who hasn’t seen an email for a while then please do double-check. Mark any Monevator emails you find in spam as ‘not spam’.

We’ve been doing three emails a week for many years now. That’s how many you should get!

Related, several dozen Monevator members are not receiving member posts over email, so they must be reading them on the site. (Via the growing Mavens and Moguls archives perhaps).

If that’s how you want it then fine. But if you’re a member and you’re missing the emails, then please make sure you’re subscribed to get all Monevator emails.

Re-subscribe if need be. (And again, look out for the confirmation email getting lost in spam…)

If that doesn’t work then please do drop me a line.

It’s our lovely Monevator members who keep the lights on around here these days, and I want you to read us exactly how best suits you.

Have a great weekend!

A conventional gilt is a reliable fellow. He is quite predictable right through to maturity, with yields drifting up or down broadly in line with his siblings.

But his wayward cousin the linker has no intention of going quietly. With less than a year to live, index-linked gilts seem to throw off the shackles of convention and lose all inhibition. Yields surge and plunge quite alarmingly.

What is the cause of such unseemly behaviour? And can investors benefit from it?

Linkers gone wild

Here’s the yield for the 22/03/2026 index-linked gilt for the year to maturity (blue), compared with that of the 2027 and 2028 linkers:

(All yield data is from Tradeweb .)

These three linkers start the year with similar real yields. But between June and July – about nine months from maturity – the 2026 yield suddenly jumps higher. The others barely move.

Linker yields reported on Tradeweb (and elsewhere) exclude the effect of inflation. They show the real yield – what your return would be if inflation was zero.

The actual return will be the real yield above plus RPI (to be replaced by CPIH in 2030). You only know this retrospectively, when all the relevant inflation reports are published by the ONS.

An opportunity?

You might be forgiven for thinking that this wild surge in yield represented an opportunity for a few months’ higher returns on some idle cash.

At least I hope you could be forgiven. Because that was the mistake I made.

But before we look at why there aren’t actually easy extra returns here, it’s worth illustrating this late-stage yield movement is not unusual.

The 2024 linker

The last index-linked gilt to mature before 2026 was the 22/03/2024 issue. It also had a 0.125% coupon.

Here’s the plot of its yield compared to its two nearest peers in the run up to maturity:

Again, the yields clearly diverge about nine months from maturity.

The 2022 linker

Just for fun, here’s the wild last ride of the linker maturing on 22/11/2022, mapped against its nearest peers:

This time there’s a slump in yield, rather than a spike. But more notable are the astonishing negative yields.

But let’s leave the madness of a post-pandemic inflation spike and a bonkers mini-budget and return to that late surge in yield on the 2026 linker.

Inflation

Inflation clearly has a central part to play in index-linked gilt pricing.

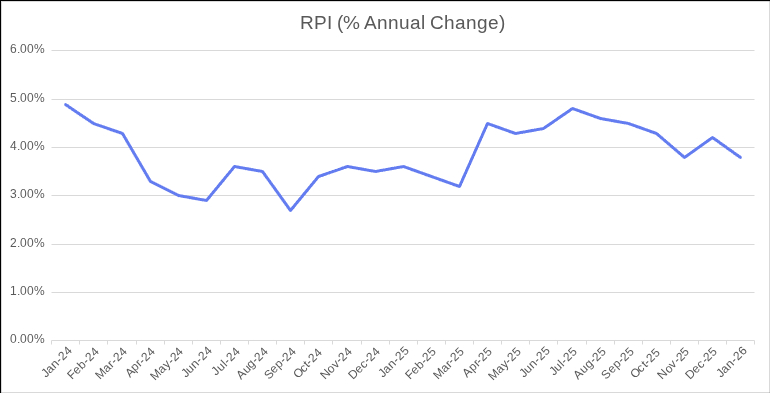

Look at annual RPI change below. Nothing seems to jump out that would account for the sudden change in yield on the 2026 linker:

But the value of index linked gilts does not increase with annual inflation. It increases (and sometimes decreases) with the much more volatile monthly changes in the index:

Advance warning

Because (most) linkers use a three-month RPI lag — and inflation data is published with a few weeks delay — investors know part of the future indexation in advance (as laid out in the DMO rules).

For example, the RPI figure for January 2026 was published on 18 February. That value feeds into the index ratio applied to linkers during March. So on 18 February, investors already know the inflation uplift that will be applied to the bond over the next six weeks.

When a linker has a few years to run, this advance warning doesn’t tell you much about the likely overall return. But as you run down the final months towards maturity, it most certainly does.

Impact on yield

As a linker approaches maturity, a growing proportion of the remaining inflation uplift is already determined by published RPI data that has yet to be fed into the index ratio applied to linkers.

Once that future uplift is known, the bond’s price adjusts to reflect it, which shows up as a move in the quoted real yield.

When only a few months remain before maturity, even small changes in the expected total return can translate into large swings when expressed as an annualised yield.

The 2026 linker yield

We can see a steep increase in RPI in April 2025, for which the corresponding increases in the principal and interest rates of the 2026 linker would play out over the course of June.

Thus, as June progresses, with more of that April gain locked in and the prospect of a lower future inflation uplift, the market works to increase the real yield to compensate for it.

Which explains the surge that we saw earlier in the yield graph for the 2026 linker.

Coincidentally, there is also a big rise in RPI in April 2023 which would similarly account for the June rise in yield for the 2024 linker.

Adding it all up

I’ve shown below a comparison of the annual inclusive yield of the 2026 linker and the corresponding yield on offer at the time from the conventional gilt maturing on 31/01/2026.

The ‘inclusive yield’ here means the total return including inflation indexing — the real yield plus the RPI uplift.

Obviously, at the time you didn’t know what the inclusive yield would be. But we do know this retrospectively, now we have all the inflation data:

Despite the headline yield for the 2026 linker swinging up three or four percentage points, the inclusive yield doesn’t change by much more than one point, and then much more gradually.

The swings in headline yield experienced since June are just smoothing out the monthly fluctuations in RPI to give an expected inclusive yield that isn’t a million miles from what you could get from a conventional gilt with a similar maturity date.

Which is pretty much what you’d expect from an efficient market.

These seemingly violent moves in real yield are really just the market doing its job – adjusting for inflation data already known to investors.

Not so wild linkers?

Rather disappointingly then, and despite my rather racy title, the last year of a linker is not wild at all. It looks a lot like the last year of a conventional gilt.

In other words, a bit like holding cash.

Indeed funds like Vanguard U.K. Inflation-Linked Gilt Index and iShares £ Index-Linked Gilts ETF (both based on the Bloomberg U.K. Government Inflation-Linked Float Adjusted Bond Index) sell gilts in their final year. There isn’t much inflation protection left in them by this stage.

The hangover

Experienced linker investors will know all this already. I suspect some are now rolling their eyes – assuming of course that they got this far.

But I only started dabbling in linkers last year. And I jumped into the middle of the yield spike to see what would happen. Having some money invested is the only way I seem to be able to focus my attention enough to learn about different instruments.

My future – wiser – self now knows:

- Not to confuse a temporary spike in headline linker yield with the genuine prospect of a better return.

- To consider the baked-in effect of the last couple of RPI values when judging the value of a linker nearing maturity.

- There’s nothing exciting about linkers in their last year and very little to be gained by buying, or for that matter selling, in this period.

So I didn’t get rich, but I did learn something – which is the best kind of return you could wish for. (Just as The Investor told me when he agreed to let me write for Monevator…)