The reason to encourage pension contributions from the government’s point of view is to get more people to save for their old age and so to not be dependent on the state.

But the reason to make pension contributions from our point of view is to minimise the amount of tax we pay over our lifetimes.

After all, we can save for old age in all manner of ways. Locking up money within a pension therefore requires an extra incentive – and the opportunity to save tax is that push.

In principle, defined contribution (DC) pensions are pretty simple:

- You contribute to your pension ‘gross’ of tax (i.e. before income tax is taken off).

- Your pension pot grows tax-free.

- Finally, you pay tax on the withdrawals at the time you take them.

All else being equal (especially your tax rate while working and your tax rate in retirement) this is a tax deferral strategy.

Pensions only turn into a tax mitigation strategy when we get a higher rate of tax relief on pension contributions than we pay on drawing the income in retirement.

As finance nerds, we want to maximise the ‘spread’ between these two rates, with as much money as possible, with the least possible risk.

Show me the OAP money!

With the abolition of the pension Lifetime Allowance (LTA) – which we’ll come to – I sat down to work out the optimal pension contribution strategy.

It should have been easy, right?

All you need to do is:

- Work out your marginal tax rate to drawdown money from your pension in retirement as a function of pension pot size.

- The bigger your pot, the more income you’ll need to draw, and the higher your tax rate on drawings.

- Discount those pot sizes back to today using your expected investment return in the pension.

- If your current marginal tax rate is above the extraction tax rate for the pension pot size that you currently have (discounted back to today), then make contributions. Otherwise don’t.

Hence all I needed to know was: when I’ll retire, the tax regime that will be in place then, how long I’ll live, and what my investment returns will be before and during retirement.

Ahem. Perhaps not surprisingly: I failed.

However my analysis turned up some titbits that I’ll share today in the hope they’ll help some of you, too.

A recent Monevator poll showed a majority of our readers are higher- or additional-rate taxpayers.

And with income tax thresholds frozen and inflation dragging more people into higher tax brackets that number is only going to grow.

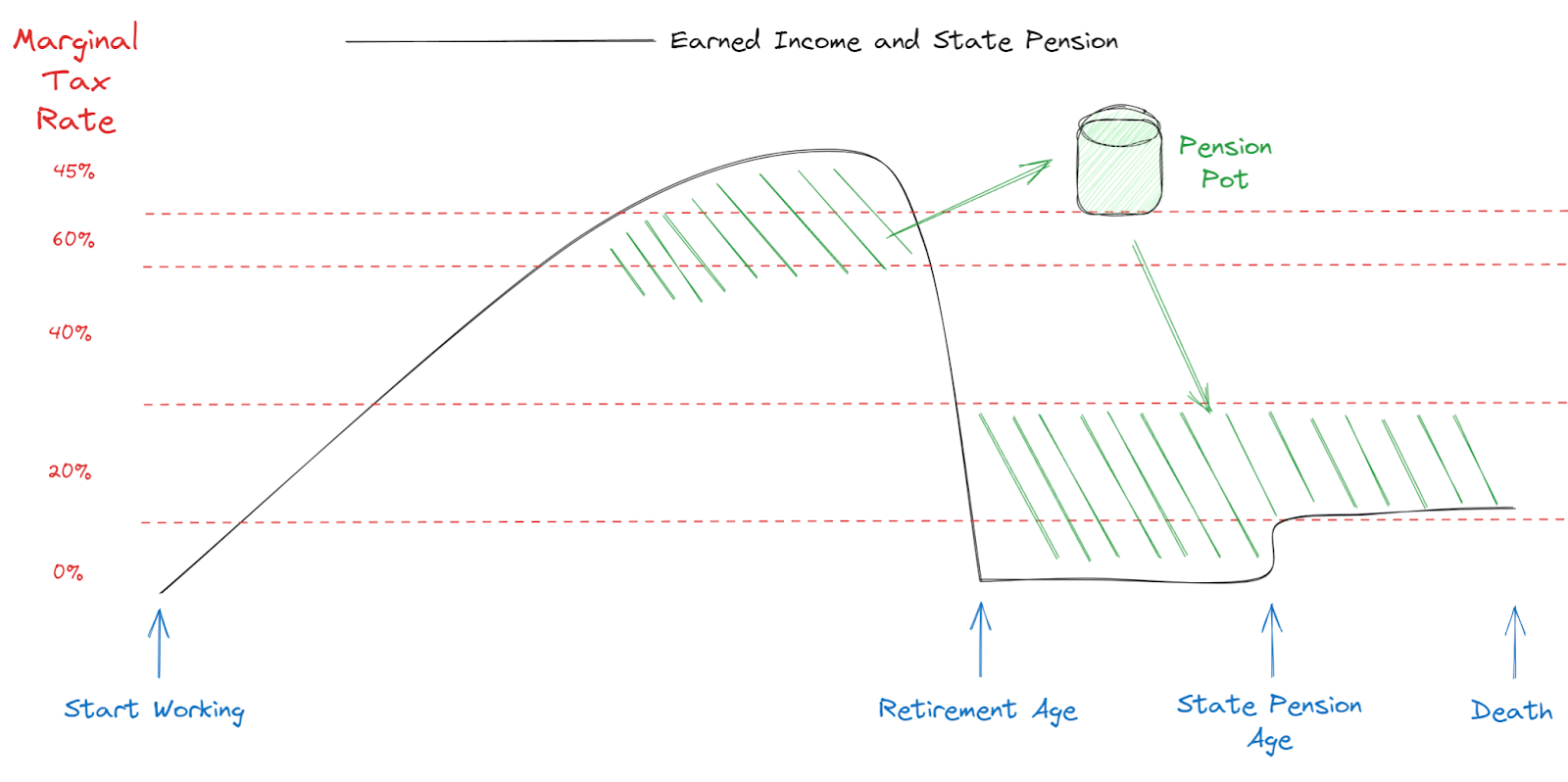

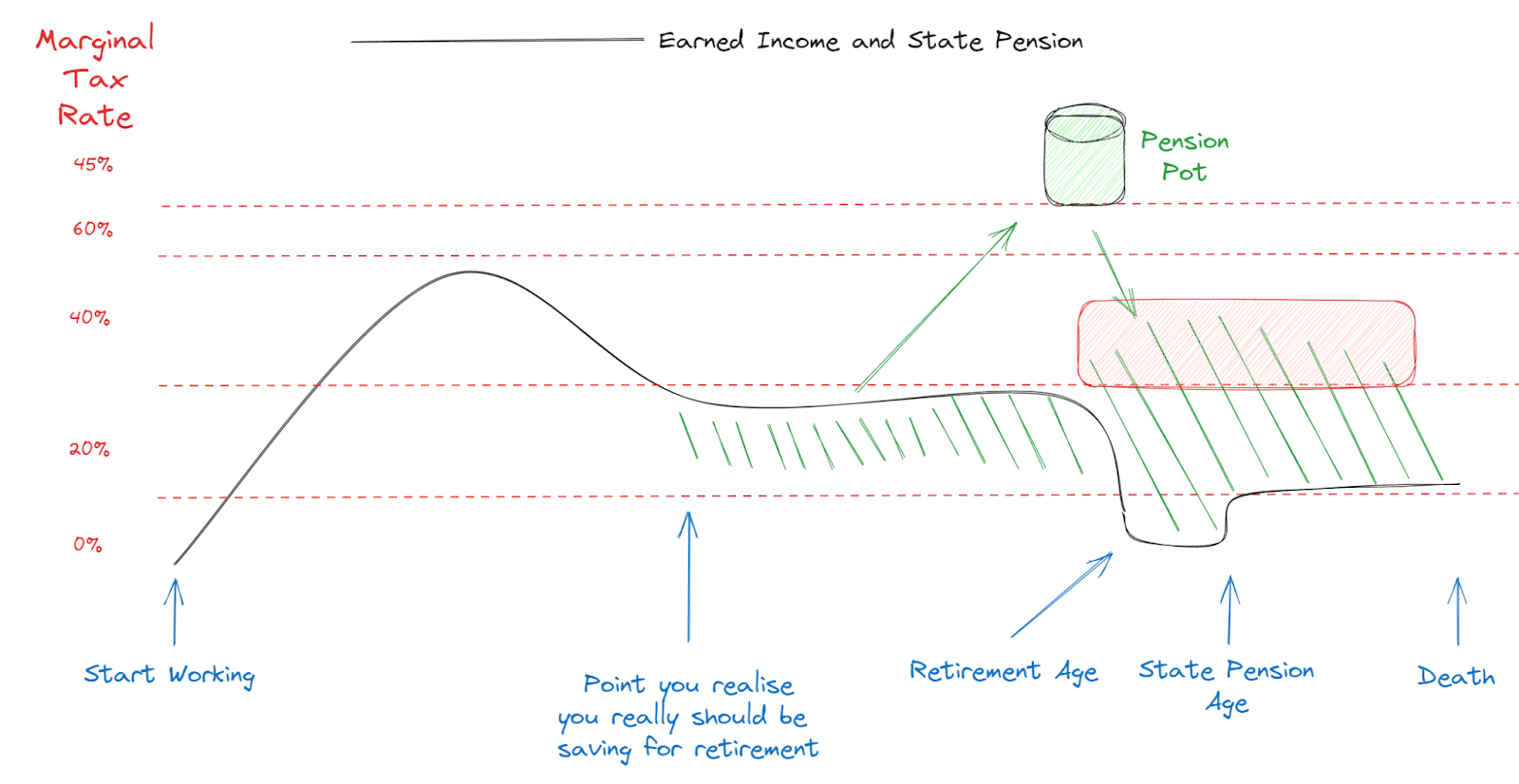

Rich people’s problems

What we’re trying to optimise with our pension contributions is this:

Now, for the purposes of this post we’re going to pretend that we live in the idealised world of finance professors.

In this textbook world we can:

- Move money across time at the same discount rate.

- Borrow, lend, and invest arbitrarily large amounts of money at this rate.

- Afford to make tax optimal pension contributions without considering anything else.

Therefore the only consideration we are making in this article is maximising the spread between contribution tax relief and the tax rate on extraction.

This is a highly simplifying assumption. But it is a reasonable approximation for fairly rich people. For everyone else, not so much. (You can’t buy food with money you’re not going to get for 20 years.)

I’ve also sort of implicitly assumed that you’re making decisions about pension contribution rates after you’ve already filled your ISA (and your spouse’s).

This is also highly unrealistic. It’s quite an ask to come up with £40,000 of post-tax income to put in an ISA, whilst also making maximally tax-efficient pension contributions.

Happily though, that is my situation and therefore the one of most interest to me.

For most people there’s a trade-off between ISA and pension contributions. The discussion that follows might help you weigh up the balance for your own situation.

Please note and to avoid me having to repeat myself: everything I’ve written below is under the current rules. (Until we talk about future policy uncertainty, clearly.)

Also remember that the tax code is thorny and everyone’s circumstances differ hugely.

Get professional tax advice if you need it. This article is all just food for thought.

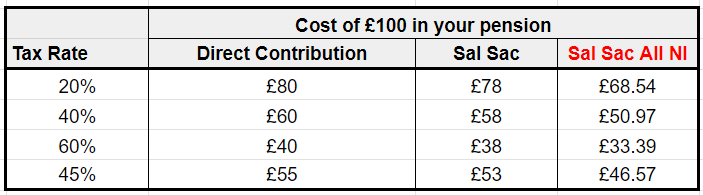

The basics: direct contributions vs salary sacrifice

Let’s start at the beginning. How do you best pay into your pension?

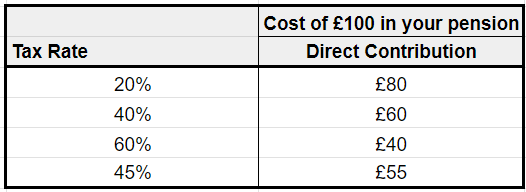

Direct contributions

You write a cheque to your SIPP provider for £80 and they gross it up by the basic tax amount. Which means you end up with £100 in your SIPP.

- This is a ‘net contribution’ of £80 and a ‘gross contribution’ of £100.

The distinction is important when we get to the limits on contributions and so on, because what counts is the £100 number, not the £80.

Now, if you are a basic-rate taxpayer that’s it. You’re all grossed-up, so to speak.

If you’re a higher-rate taxpayer or above, however, then you report this (gross) contribution on your tax return. HMRC adjusts your (gross) income down by the amount of the (gross) contribution, and you’ll be owed a refund.

For example, if your marginal tax rate is 40%, then you’ll get a refund of £20 on your £100 gross. Which makes the effective ‘cost’ of putting £100 into your pension just £60.

- You write a cheque for £80, you have £100 in your pension, and you get a cheque back from HMRC for £20. Net cost: £60.

That the contribution is used to ‘reduce’ your income from a tax point of view is important.

Crucially, if you’re in the 60% tax bracket – between £100,000 and £125,140 – then you effectively get 60% tax relief on your contributions. (Because reducing your income gets some of the annual allowance ‘taper’ back, which is the cause of the 60% rate in the first place.)

For completeness, if you’re a 45% taxpayer:

- You’ll get £25 back from HMRC when you file your tax return.

Taxed from every angle

In practice, you may find you pay multiple rates of tax relief from a single contribution.

For example, if you earn £150,000 and make a £60,000 contribution, that contribution will experience tax relief in part at 45%, 60% and 40% rates:

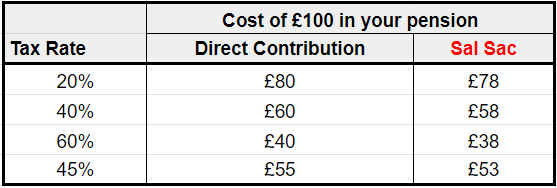

Salary sacrifice

The other way to make pension contributions is to sacrifice some of your salary. Here you instruct your employer to pay some proportion of your pay into your pension scheme instead of to you.

The important difference with this arrangement is that there is no National Insurance (NI) due on this payment, because it is not ‘pay’.

Now nominally this might not sound like a big deal. Employees NI is only 2% (mostly).

Still every little helps, as you can see in the table below.

But you saving a few quid is not why your big-hearted employer is always sending you emails extolling salary sacrifice as a way to pay for electric cars, bikes, pensions, and goodness knows what else.

No. Your employer is motivated by the 13.8% employers’ NI that it doesn’t have to pay on whatever you salary sacrificed into your pension.

Your employer saves £13.80 per £100 of salary sacrifice. So probably the most important question in this whole post is: can you get your employer to share some of that money saved with you?

Well, can you?

It depends. Some employers do it by default. Others don’t. And some – big and small – will negotiate.

For my part I’ve successfully negotiated a sharing of these savings either firm-wide or as a special deal for me (“I won’t tell anyone else”).

You do have some leverage. After all, you can just make a direct contribution. It’s 2% more expensive for you, but 13.8% more expensive for them. When we approach the limits of maximising the amount of tax we save it turns out it’s highly sensitive to the ability to clawback some employers’ NI, so I’d encourage you to go for it.

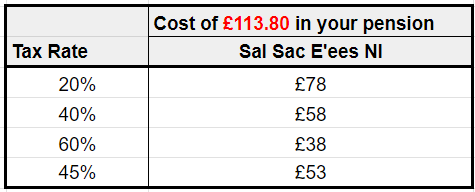

Usually, any sharing of these savings goes into the pension contribution, rather than as (taxable+NI) cash to you – otherwise the process is a bit circular.

This makes the maths a bit weird, because we’re now ending up with £113.80 in the pension for each £100 of salary sacrifice:

If we renormalise that back to the cost of £100 in the pension we get this:

The ‘gross contribution’ if you sacrifice £100 of salary and your employer pays £113.80 into your pension is £113.80, not £100.

If we’re hitting our peak tax mitigation potential – that is, inside the 60% bracket – then we are foregoing just £33.39 in net pay to get £100 in our pension.

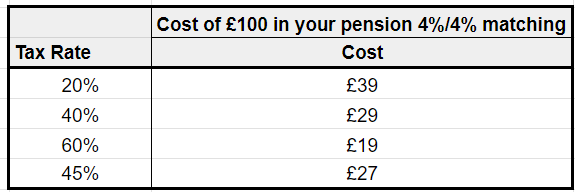

Employer matching

There’s a legal obligation for your employer to make pension contributions on your behalf, and to deduct a minimum contribution from you. It is usually something like they pay 4% and you pay 4%.

You can opt-out of this (I believe…) but why would you? It’s pretty much free money.

Given that your employer-matched contribution is processed as salary sacrifice, you end up with this:

There’s pretty much no extraction tax rate on drawdown that would render these contributions not worthwhile.

Indeed, during my pension wilderness years enforced by the LTA, the employer match was all I did.

Employer pension schemes vs SIPPs

A common complaint I hear about salary sacrifice (SS) is that you can only SS into your employers’ chosen pension scheme.

The scheme with poor investment choices, obscure fees, and a website unchanged since the late 1990s.

Well yes but this is trivially surmountable. Just set the investment choice in the company scheme to ‘cash’ and every six months or so transfer that cash from your company scheme to your favoured SIPP.

Your company won’t care. (Probably.)

Contribution limits

There are limits to how much you can contribute to your pension.

The limit is the lower of:

- £60,000

- Your total employment income

Note this limit is on the size of your gross contribution.

The £60,000 limit is ‘tapered’ (it becomes less) if you earn over £200,000 – or £260,000 because the rules are, inevitably, pointlessly complicated.

There is also a mechanism called carry back that allows you to carry forward (I know…) your unused allowance from previous years, for up to three years.

Handy if your earnings are very volatile.

Summary: getting the money in

We’ve established the cost of getting money into our pension scheme:

It’s worth noting that if you’re subject to the ‘High Income Child Benefit Charge‘, have things like childcare tax-credits, or you earn income from residential property (with a mortgage) then your marginal tax rate could be higher.

It might even exceed 100%.

An example of what not to do: what I did

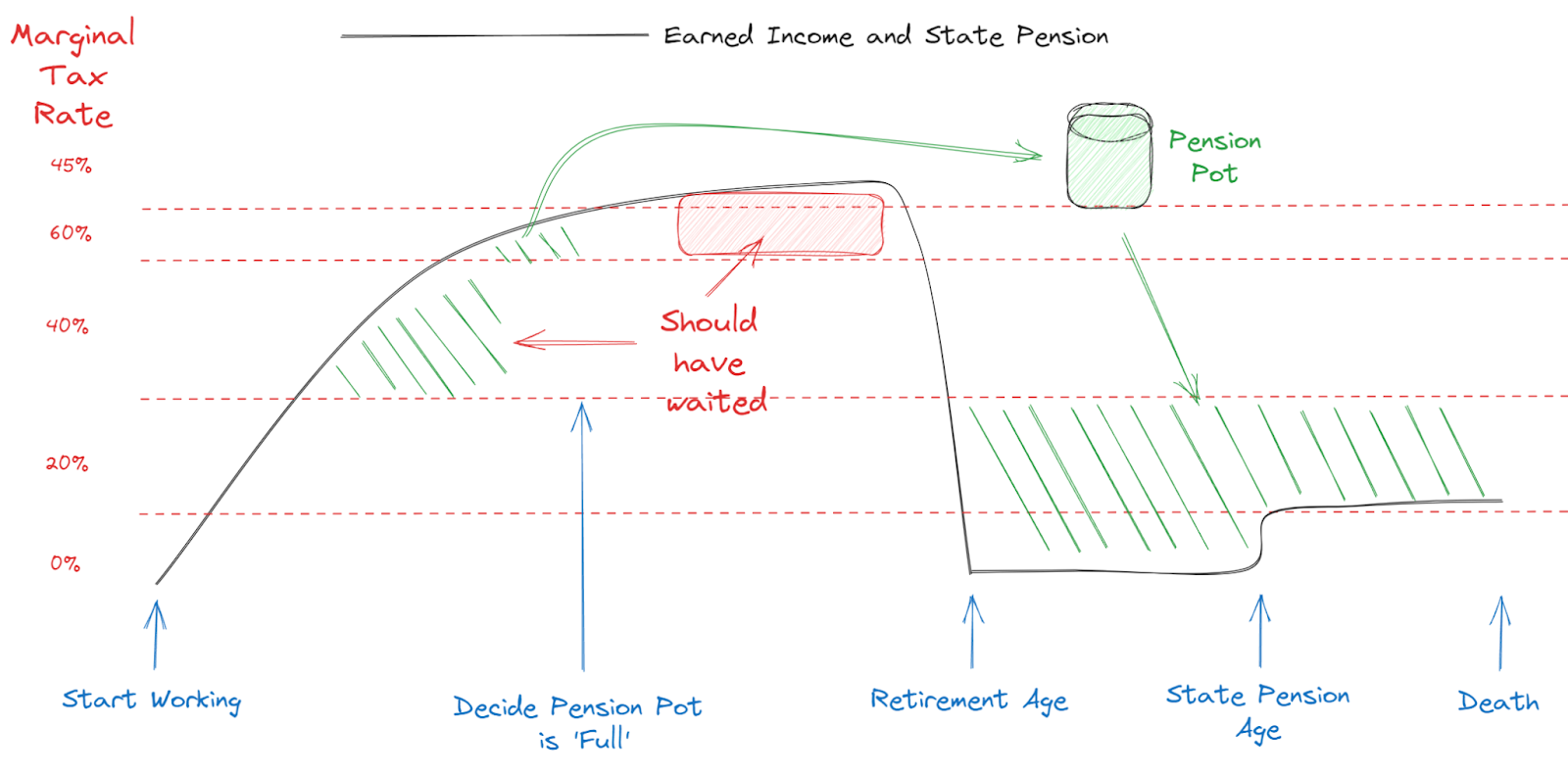

The challenge is that you don’t know the future. Specifically, you don’t know your future earnings.

You want to concentrate your contributions in years when you have the highest marginal tax rate.

But when will that be?

What you really want to avoid is a situation where you’re getting tax relief at, say 40%, but you could (later) fill your pension with tax relief at, say, 60%:

This is not far from my situation actually.

High earnings and acute imposter syndrome early in my career meant I contributed large sums to get 40% tax relief.

Later on I didn’t contribute – even though I could have got 60% tax relief – because I was over the LTA.

In my defence, when I made those original contributions the maximum income tax rate was 40%. We didn’t have the 60% band. Indeed, we didn’t have the LTA!

Still, I should have been more patient.

This rather emphasises the point that over long time periods there’s enormous policy uncertainty.

The pension pot then grows tax-free…

…or does it, really?

I would argue not.

Sure, from an administrative point of view you don’t have to pay capital gains on any gains or income tax on dividends (except on some foreign dividends).

However in the end you will have to pay income tax on your gains – even if those gains only kept up with inflation.

And income tax rates are higher than both capital gains tax and dividend tax rates.

Then there’s the possibility that the government will just decide to confiscate some or all of the gains, in this supposed ‘tax-free’ wrapper. Which they have done before with the LTA.

So, I’m unconvinced.

Given there exists a perfectly good actual tax-free wrapper – the ISA – I would argue that the allegedly ‘tax-free’ growth in the pension is not, by comparison, tax-free.

The ‘tax-free’ ness of investment returns in the pension pot should be ignored when considering the spread between inbound tax relief and outbound tax paid.

This is not to ignore the impact that investment growth has on our capacity to withdraw under certain tax thresholds, or to be subject to any future LTA charge. These considerations do very much matter. They should feed into our estimates of the extraction tax rate.

Perhaps a reasonable base case is that our investments keep up with inflation, but that tax allowances do not. (Reasonable because this has been the situation for many years).

Cashing out

At last the fun bit!

Kerching! Et cetera et cetera.

Actually, while spending your pension pot is certainly more agreeable than doing without in order to fill it, in the meantime we’ve yet more maths to do.

Moreover it turns out that working out the tax relief we’ll get in on the way in was the easy bit.

Now we need to guess estimate work out our marginal tax rate in retirement, when we come to extract that cash from our pension.

The tax-free lump sum

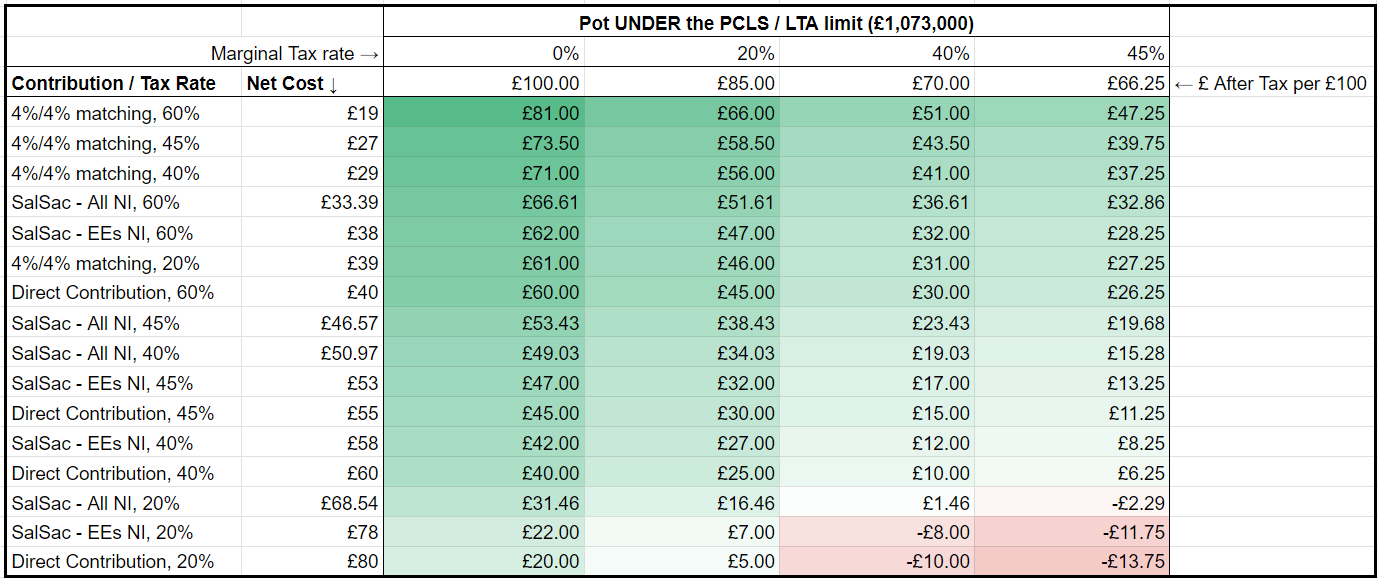

Thanks to the pension commencement lump sum (PCLS) – sometimes just called the tax-free lump sum – you can withdraw 25% of your pension tax-free, up to a limit of £268,275.

Effectively if your pension pot is going to be worth less than £1,073,100, then you can just assume your tax rate for withdrawals is 75% of your actual tax rate.

For example, you retire with a £1,000,000 pension pot. You pull £250,000 out tax free, and pay 20% on the rest (by spreading the withdrawals over many years).

- Your marginal tax rate will be 75% of 20% = 15%

Great, that’s lower than the rate of tax relief we got putting the money in, regardless of the circumstances. (See the chart above. The lowest amount of tax relief possible is 20%).

Getting a camel through the eye of a needle

The larger your pension pot though, the harder it is to drawdown at low tax rates.

In fact, given the low threshold for higher-rate tax (£50,270), your investment returns can be mediocre and yet you can still reach (non)escape velocity – where you’re only drawing down investment returns, and never ‘shrinking’ the pot.

If you do need to choose between pension and ISA savings then you also need to think about this dynamic. Don’t just pour all your savings into pension contributions. Because of the cap on the PCLS, the key inflection point is when your projected pot is on target to exceed the old LTA limit of £1,073,100.

Summing up

Putting it all together, we can calculate the ‘P&L’ in tax savings. By which I mean the number of post-tax- pounds we’re better off as a function of tax-relief on the way in and tax-rate on the way out…

…depending on if our pot is below the old LTA limit:

…or above it (LTA extraction rate at 55% included for completeness):

Avoiding over-saving

A shortcut is to think about worst case scenarios. In particular, what we’re trying to avoid is the situation where we’re paying a higher rate of tax on withdrawing than we got in tax relief:

Don’t touch it

There’s another option to consider, too.

People who are lucky enough to have lots of other assets to draw on can simply never draw their pension down at high tax rates. They can just leave it in there, growing.

Your beneficiaries can then draw it down at either 0% or their marginal tax rate, when you are gone. It’s outside your estate for IHT purposes.

We’ll discuss this a bit more below, because I believe it is very likely these rules will be changed.

For me personally – with kids, and with about a 25% chance of dying before the age of 75 (and a 100% certainty eventually) – this is quite a valuable benefit.

But won’t they change the rules again?

Yes of course they will.

So what tinkering might we anticipate in advance?

Reintroduction of the Lifetime Allowance

Bringing back the LTA is an odds-on favourite because the Labour Party immediately committed to its reintroduction when the Tories abolished it. (At least, for everyone who doesn’t work for the NHS.)

With that said, they’ve not been particularly vocal about it since. Perhaps now that the detail about the limit on the tax-free lump sum has sunk in it seems less of a priority?

After all, if you’re constraining the amount of tax-relief that high earners can get on the way in, and the amount they can get out tax-free, it’s not obvious that the LTA justifies its considerable complexity.

On balance I think it’s likely that a long period of ‘consultation’ about pensions will ensue. If they don’t re-introduce the LTA then that consultation is likely to include at least one of the other possibles I’ll get to.

Countermeasures

- Don’t save too much in your pension. Focus on those very high tax rate years.

- Only contribute if your tax relief on contributions is so high that you’ll still come out ahead even if you’re subject to the LTA charge .

- Historically there have been ‘protection’ regimes available if the value of your pension is above the LTA when they introduce it. This is so they can pretend that the LTA is not, effectively, retrospective taxation. (Although of course it is, even if you’re below the LTA limit when it gets introduced).

- Have the lower return assets in your pension and higher return assets in your ISA. (You should do this anyway.)

Changes to inheritance tax treatment / beneficiaries pensions

As we’ve seen, one of the major benefits of getting money into your pension is that, under the current rules, it’s outside of your estate for IHT purposes.

I have discussed previously how wealthy families are already using this as an inheritance tax avoidance strategy. (That earlier post also goes into the mechanics of how). For those who are still working and whose estates would likely be subject to IHT, this is a very attractive planning vehicle. It enables them to get very high rates of tax relief. The result is a highly tax-efficient ‘trust fund’-like pot, which either they or their heirs can access.

It’s unlikely, for legislative reasons, that pensions will be brought inside the IHT net. The most likely change is that full tax-free withdrawal by beneficiaries if the benefactor dies under the age of 75 will be removed, and the same rules apply regardless of their age at death.

Indeed this might actually happen anyway as part of the LTA abolition.

Pensions would still remain very useful from an IHT planning point of view. The beneficiaries can drawdown when their marginal tax rate is low, for example. Or they can just treat the whole thing as an emergency fund that they can get at if they really have to (and pay the tax to access it).

Over the long run I doubt having ‘beneficiary’ pension pots that can compound tax-free for decades or even centuries would survive the “So-and-so has £1bn in their pension” headlines. We are not America.

Talking of America, another proposal occasionally raised is to force beneficiaries to take a certain fraction of their pot as taxable income every year. These are called required minimum distributions.

But let’s not give our politicians any ideas by discussing that further here, eh?

Flat-rate tax relief

The tax-saving benefits of pension contributions rise with your earnings, thanks to higher rates of tax relief. Because of this, many people consider the tax planning we’re discussing today as inherently ‘unfair’.

Critics argue the purpose of tax relief is to try to ensure you aren’t a burden on the state in your old age.

But high earners will save for their retirement anyway. They don’t need a tax incentive.

In contrast, because they get less tax relief, lower income people have less of a motivation to save. Yet these are also precisely the people who need more encouragement to do so.

The solution often posed by left-leaning think tanks is to offer tax relief on contributions at a ‘flat’ rate. Somewhere above the 20% basic rate, but below the 40% rate. Typically 30% is proposed.

Such a flat rate would give less tax relief to the rich and more to the poor.

Full disclosure: I’m quite sympathetic to this argument.

There would be quite a lot of complexity involved in implementing it – especially for those in Defined Benefit (DB) schemes. However, since the remaining DB schemes are pretty much all in the public sector, there’s no reason (other than fairness) as to why there shouldn’t be a different (more generous) tax regime for them.

If we can have a different tax system for people in the NHS, why not for all government employees?

Countermeasures

If you think flat relief is coming, your action depends on the tax relief you currently get on contributions:

- Are you a higher / additional / 60% rate taxpayer? Then you should max out contributions that get tax relief at those rates because in the future tax relief would be lower.

- Are you a basic-rate taxpayer? You should make minimal contributions now. Aim to increase your contributions when the flat rate is introduced.

Elimination of the income tax allowance taper (60% rate)

We can all agree that having a 60% rate in between the 40% and 45% rates is ridiculous, yes? So it’s not completely impossible that some future government will agree.

Labour has committed to not raising income taxes when they form the next government. I imagine they shan’t be lowering them either!

But in a second parliament they might eliminate the taper as a quid-pro-quo for increasing additional rate tax to 50%, for example.

Countermeasures

- If you’re a 60% taxpayer then pay the 60% slice into your pension, because that relief might not be available in the future. The same slice might only attract relief at 40%, 45% or 50% someday.

Generally higher income tax rates

A penny on income tax to “save the NHS”. Another one for “care”. Another one for our “brave boys and girls fighting in some foreign war”. Oh, and another one to send some poor sods to Rwanda.

You know the drill. Taxes pretty much only go up, as state expenditure increases faster than the size of the economy. I believe this is is best tackled by increasing the size of the economy. But growth seems to be even less popular with voters than high taxes, that are, anyway, mostly paid by someone else.

If income taxes are going up over the long term, then the last thing you want to do is defer your income tax until later. You’d be better off paying tax now.

Countermeasures

- Don’t save into your pension except at very high tax relief rates.

Crazy things that a government might consider

All those potential revisions to the pension system seem somewhat feasible to me.

But the longer you’ve got until retirement the crazier it could get.

Here’s just a random assortment of crazy ideas you see kicked about:

- Means testing of the state pension – based on private pension ‘income’. This would favour ISA savings (which likely wouldn’t be counted) over pension income (which would).

- Means testing of the state pension – based on ‘wealth’. Possible that pensions wouldn’t be counted, but ISAs would (as they are for some wealth-based benefits, such as unemployment benefit). Favours pensions contributions over filling the ISA.

- The integration of NI and income tax. This obviously makes sense, because they are both just a form of income tax. A properly brave government would wrap employers’ NI in too. (Although if people really knew how high tax rates are…) The pay-off for this bravery would be much higher income tax rates which could also be applied to ‘unearned’ income such as income from pensions. Favours ISAs over pension saving.

- ISA lifetime allowance. I wish John Lee in the FT would stop banging on about how much he has in his ISA. Because seriously, why draw attention to it? Some sort of cap on the value in an ISA that’s eligible to be tax-free would be retrospective and highly complex to administer – but when has that ever stopped them? Obviously favours pension saving over ISA saving.

- ISA allowance cut (or a real terms cut through fiscal drift). Favours getting cash in your ISA while you can and leaving pension savings until later. Perhaps when you’re on a higher marginal tax rate?

- Special tax rates for pension income / an ‘Unearned Income Surcharge’. Factor in employers’ and employees’ NI, and people in employment pay much higher tax rates than the retired. This is unfair. Rather than rolling NI into income tax, you could address this by taxing pension income at a higher rate than employment income. This has less behavioural impact, because while employed people will work less if you tax them more, retirees have no choice but to live off their pensions. Favours ISA saving over pension saving.

How to model all these risks? We can’t really. You will have to make your own assessment.

The best insurance policy is to focus your contributions where you get very high rates of tax relief. That way you will probably come out ahead in most circumstances.

Tips and tricks with pension contributions

There’s always something more to do with a tax code as complicated as ours!

Keep it in the family

Make sure you plan your pension savings holistically with your spouse. Let’s say you stop working for a decade while the kids are small, but your partner keeps working. Once you go back to work you are both higher-rate taxpayers. You have a pension pot of £200,000 and your partner has one of £800,000.

Clearly, because of the PCLS cap, as a couple your pension contributions should take priority over that of your partner’s.

Similarly, if both your pension pots are small and one of you can get your employers’ NI through salary sacrifice and the other can’t… you know which one to prioritise.

Maybe you should even think about pensions from the perspective of your whole family, as we showed previously.

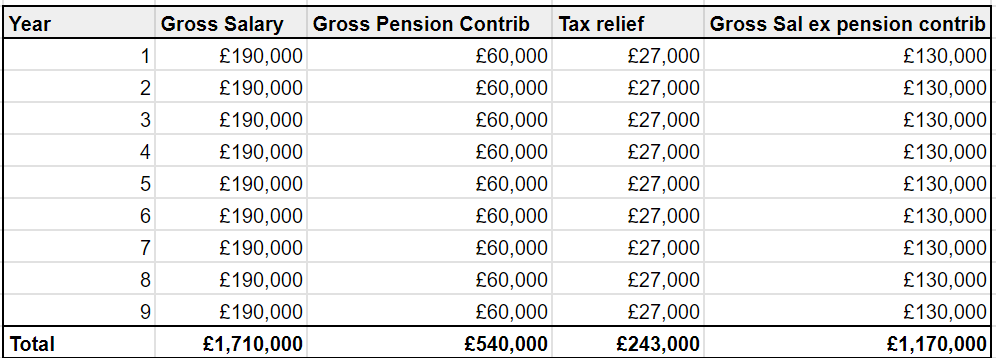

How to get 60% tax relief if you’re a 45% rate taxpayer

You earn £190,000 a year. You make the maximum gross contribution of £60,000 a year. This brings your taxable pay down to £130,000.

So you’re only getting 45% tax relief on the contribution. And you are paying 60% on most of that £30,000 above £100,000:

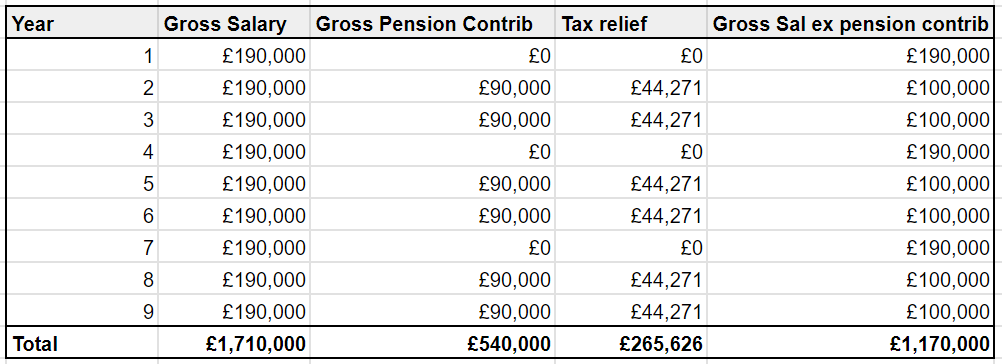

Is there something we can do to improve this situation? Well, yes, of course, otherwise I wouldn’t have brought it up.

By using ‘fallow’ years – where we don’t make a pension contribution – we can use ‘carry back’ to carry forward the unused allowance from the fallow year to make a contribution that eats into our 60% tax rate.

Voila:

This saves us £22,626 of tax over a nine-year period – £2,514 per annum – just for being organised.

Fill your ISA with your PCLS / tax-free amount

You want to max out your pension contributions in the last few years before age 55? This doesn’t leave you enough cash to fill your ISA?

Then you can do something like the trick I showed previously. But beware of the ‘pension recycling rule’.

The pension recycling rule

Not targeted at my trick linked to above particularly, but if you increase your pension contributions ‘significantly’ prior to taking your tax free-amount, then HMRC has a special rule aimed at clawing back your tax relief.

Called the recycling rule, it’s designed to… stop you using pension contributions in exactly the way that Parliament intended you use them.

Scaling salary sacrifice

Is your employer paying its NI savings into your pension? Make sure that the amount you’re reducing your salary by (to get into a lower tax bracket, for example) is less than what’s going into your pension (as used to calculate the annual contribution allowance).

For example, let’s say you earn £160,000 and you salary sacrifice £60,000.

Your employer will be paying £68,280 into your pension, including the NI savings. This is £8,280 over the annual allowance – unless you’re using carry back.

The maximum salary you can sacrifice within the annual allowance is: £60,000/1.138 = £52,724.07.

This will leave some of your earnings exposed to the 60% tax rate. Be careful.

Summary

- There are almost no circumstances where contributions to your pension that attract 60% or higher tax relief or employer matching contributions will leave you worse off in the long run. That’s true even if the LTA is re-introduced in its old form.

- Capturing some of the employer NI as part of your tax relief can make a big difference.

- The larger your pension pot, the more you need to think about policy risks.

- Once your pension pot is over four-times the PCLS limit, there’s little point in making direct contributions at 20% tax relief.

Made it this far?

Want more Finumus magic? Follow him on Twitter or read his other articles on Monevator.

Hi Finumus, thanks for this. I too have grappled with this and it is surprisingly complicated to get “right” in real time. I (heavily influenced by being a tax adviser and therefore being seduced by tax efficiency) sacrificed a lot of 40% earnings into my pension pot earlier on, and now find myself with more of a practical problem – I get employer matching and am in the 60% rate now (and would need to contribute quite a bit to get my tax relief into the 60% band), so pension contributions are in theory more attractive than ever, but my wealth is massively skewed towards my pension pot and I want to retire before I am allowed to draw from it. So I am left contributing less and sacrificing tax efficiency for the more practical goal of having some money to live off to get me through to pension drawdown age. A good problem to have (I never anticipated being able to afford to retire well before 57) but an offence to my tax efficient mind and obviously wish I had not gone ham on the pension contributions quite so early!!

Great article. There is even more subtlety in the marginal tax rate decisions than I was aware of. I’m eternally grateful to whatever it was that drew my attention to the 60% marginal tax rate, probably around 2007/8/9 – at the time we had a side hustle that was generating income that took both me and spouse into that territory and we quickly took the decision to divert everything we could to pension to avoid that hit. Although it caused the odd cashflow problem at the time, in retrospect it has put us in a position 15 odd years later where RE is a viable option. I learned recently of a colleague who only just became aware of it and he is kicking himself.

I think LTA overly distorts decisions (I know it’s only an issue for a tiny few)- after all it’s on withdrawals not pot size. (Like a student loan is an incremental tax rate not a loan). Bigger pot is better from almost every angle – allows much more freedom to take risks of many sorts.

My guess is that state pension will be added to LTA calcs. at some point in the near future. Simple to do as HMRC has all the data. Means the (relatively) wealthy get a higher proportion of their pension withdrawals taxed at a higher rate.

Excellent post, thanks for that. A few comments:

Contribution limits: isn’t it the lower of £60,000 and total income (not just total employment income)? Say someone has employment income of £15k, dividend income of £15k, rental income of £15k, interest income of £15k, I believe they can contribute up to £60k, right?

Regarding your contributions attracting only 40% relief: don’t be hard on yourself, it was *not* a mistake given the information at the time. It’s like saying contributions attracting 45% relief now are a bad idea if lower tax rate goes to 50% in the future. If it does, then yes, you would have been better off not contributing to the pension, but you don’t know that in advance and there’s no reason to expect it. What if the marginal tax rate hadn’t increased but instead reduced from 40% to say 35%? Had you been more patient as you say, you would have regretted not having the tax relief at 40%!

ISA lifetime allowance: if this were ever to be introduced, you simply cash out the ISA once you hit that level. Unlike the pension that is locked for decades you can do that.

Great article, thank you.

Since you can of course contribute above your annual allowance (but then pay the Annual Allowance tax charge on the surplus), is there any scenario where it would be beneficial to do so?

For example, if I have already contributed up to my annual allowance, I could either take £100 as income or my employer could put £113.80 into my pension (if they give me the full 13.8% employer’s NI saving).

Taking £100 as income would leave me with £53 after income tax and NI.

Taking £113.80 in my pension would leave me with £113.80 in my pension but £-51.21 cash after paying the charge, so £62.59 net, but I would of course still have to pay income tax (if any) when withdrawing from my pension.

Great article, and a subject I’ve been thinking about a lot lately. I run my own limited company so putting pre-tax earnings into a pension is by far the most efficient method of drawing from the business (though obviously doesn’t cover my day to day expenses). Now that the LTA is gone, is there a theoretical maximum optimal pot amount to be aiming for? I’ve been operating with a target of ~1.6m, i.e. enough for 52k from 4% SWR after maximum tax free lump sum. Or am I missing something?

> Special tax rates for pension income / an ‘Unearned Income Surcharge’… This has less behavioural impact, because while employed people will work less if you tax them more, retirees have no choice but to live off their pensions.

I think it will have a behavioural impact – it would cause retirees adjust their voting behaviour…

“… and every six months or so transfer that cash from your company scheme to your favoured SIPP. ”

Unless it’s a scheme like Nest, who don’t allow partial withdrawals.

(Of course, the workaround there is to opt out temporarily, close the Nest account, then opt back in, all the while hoping you don’t miss a month’s worth of contributions which would likely wipe out any advantages of doing this.)

Seems that Finumus is arguing that people such as myself should still be contributing to a pension.

I took fixed protection in 2012 to protect my £1.8mm LTA and so have not been able to contribute for over a decade without losing that. The argument in favour of breaking fixed protection is that the LTA is gone and the pension trust is tax free from IHT perspective so max it out. The arguments against are that the LTA might come back, my PCLS is £450k with protection but £268k without, and basically what is the point when the annual allowance is still just £10k.

Right now, I’m still of the view that fixed protection is better. The risk is that might change over time and, meanwhile, I’m missing out on those accumulated (small) contributions. Interested why Finumus never took fixed protection.

Nice post.

From the weight of respective text/diagrams I think you are more focussed on the accumulation side of things. De-accumulation can also offer opportunities to optimise/minimise tax payments, but these are rarely written about although they generally use similar arbitrage methods.

A key thing to look out for in de-accumulation (that I personally overlooked until almost too late) is that it is about the whole taxable income stream and not just the DC pension income. May also be worth noting in passing that the pensioner effectively pays the deferred tax on all contributions (plus hopefully growth), not just those made by him/herself.

The overall balance is not just about tax rate differences but there is also a critical time (actuarial) component too. Take the following completely non-realistic example as a thought experiment. All contributions made in one year attracting say an average of 60% relief. Pot grows well and many years later the family/survivors use it as a perpetual trust that they withdraw 2%PA from for ever that they pay 15% or maybe after a while 20% or even more tax on. Is this optimal or ……….

IMO, the tax man does rather well out of pensions and has somehow managed to convince people that the costs/benefits he incurs are only the upfront cost of tax reliefs and he apparently gains absolutely nothing from the deferred income tax streams – a great piece of spin if ever I saw one.

Lastly, with you 100% on RMD’s and IMO something similar may well be rolled out to tackle the IHT issue.

A request: a post on pension transfers to the great land of Abroad. What to do if you hope to scoot off to warmer climes?

For example, might it be wise to take your tax-free lump sum under British tax law and then, a couple of years later perhaps, do a bunk and transfer the remainder of the scheme abroad? Is that even possible?

Or would one simply settle for drawing the pension scheme income (as distinct from TFLS) in the normal way but subject to foreign income tax rather than UK tax because one is no longer tax resident in the UK? Is that even possible?

For some of the poorer people reading can you clarify your maths for the salary sacrifice contributions within the 20% income tax band?

It looks like you are not factoring in Employee NICs at 12% (soon to be dropped to 10% in the New Year) and instead using 2% which is only applied from the 40% threshold?

It is one of the reasons why salary sacrifice is in a sense proportionally even better for 20% taxpayers, or indeed 40% taxpayers who salary sacrifice deep into 20% territory when they otherwise may have only gone down to £50k if they were not getting relief on Employee NICs .

Thanks for the post. This is something I think about a lot and is quite hard to get my head around. Two things I’m not so sure about:

“Sure, from an administrative point of view you don’t have to pay capital gains on any gains or income tax on dividends (except on some foreign dividends).

“However in the end you will have to pay income tax on your gains – even if those gains only kept up with inflation.”

I don’t get this, especially with reference to the ISA. An ISA is an investment pot that you contribute to with post-tax earnings, whose gains are not taxed, and from which withdrawals are not taxed. (“T-E-E”, or “Taxed-Exempt-Exempt”). A pension is an investment pot that you contribute to with pre-tax earnings, whose gains are not taxed, from which withdrawals ARE taxed. (“E-E-T”, or “Exempt-Exempt-Taxed”.)

The amount you get in either scenario is the same – it’s mathematically identical to tax contributions at x% as it is to tax withdrawals at x%. The only exception is when you move across tax bands, so (eg) a basic income tax payer may be better off contributing to an ISA than to a pension, because their gains or later contributions to the pension might make their pension draw-down earnings large enough that those contributions are taxed at a higher rate when the pot is drawn down. Obviously, most of the time people aim to use pensions to do the opposite. The Lifetime Allowance does add another complication, but the basic point that TEE and EET accounts are identical in terms of net return to the saver is important.

I disagree with your discussion of tax relief completely. The purpose isn’t to “encourage” anyone to do anything, it’s just to avoid people being taxed more for saving in a pension than they would if they didn’t do so. If you had 30% tax relief, then anyone paying 40% income tax or more who contributed to a pot that allowed withdrawals that would be taxed at 40% or more would be paying 10% tax on the way in and 40% tax on the way out, so they would immediately be worse off than if they’d just paid the money up front and held it as income. Pensions really wouldn’t make sense for a lot of higher earners at all in that case.

There may be other practical limits when using salary sacrifice. My company, for example, will no longer allow me to earn less than minimum wage when using salary sacrifice (at the time, I had a side hustle earning more than enough to keep body and soul together).

@ZXSpectrum48k

I never took fixed protection because my pension was worth like, £400k when they introduced the (then £1.8m) LTA. I’m not sure you could even take protection unless the value of your pension exceeded the LTA at the time? Anyway I didn’t know my investment returns would be so good (i.e. lucky), and that a bias for USD denominated assets in the SIPP would have Brexit pushing me over the LTA limit. (I wrote about it here: https://monevator.com/oops-ive-gone-over-the-pension-lifetime-allowance/)

@SemiPassive

Yes, you’re right about this, I did not count employee NI properly on below £50k, this was a error, sorry. TBH I’m just not familiar with how employee NI really works – for me it’s always just ‘marginal 2%’. That it doesn’t seem to line up with income tax bands, and that all the quoted stuff is based on weekly earnings does my head in.

Smart piece and very nicely written and explained. Many thanks @Finumus.

Worth highlighting possibilities for policy arbitrage between different governments if you have a DB alongside a DC.

Take the DB at scheme retirement age.

Until then, or thereafter if part retired and still working, pay what you can afford to into SIPP/DC, after filling ISA (subject to AA – i.e. earning limit or £60k or a lower tapered amount).

Hold fire on touching SIPP/DC until the Tories get back in again (sooner or later they will) and then see if they remove the LTA for what will then be a second time (assuming that it’s Labour in from 2024/25 to at least 2029/30, and that they do what they’ve said that they will and reinstate it).

The moment the LTA is removed again (should that happen) then take the DC pension (and the maximum tax free lump sum).

In a phrase ‘strategic patience’.

You’ll have up to 75 before you having to cave in and use the DC/SIPP, and will also be fortified by receipt of the state pension for the last years up to then.

And, in the meantime, as you wisely note, have lower return assets in SIPP & higher ones in ISA.

Of course, one advantage of retirement is you’re not tied to living in the UK for work anymore, which means opportunities to live in lower cost, lower tax jurisdictions.

@TLI – I think once you draw a pension the maximum contribution is 10k ? Not the lower of your salary/ 60k? Might be worth you checking before pressing the button.

@Finimus – thanks for the article. I guess the real life problems with it are you don’t know what your earning peaks will be, or what will happen with the tax rates or bands, so to me the key variable is the employer match.

@BBlimp: For reasons which I’ve never really fully understood, the £10k p.a. Money Purchase AA only applies to contributions to DC pensions & doesn’t affect DB schemes. My DB pension is basically the reason that I stay with my existing job. It’s a golden ball and chain.

This article is what I like this website for, just amazing source of useful information.

“If you’re a higher-rate taxpayer or above, however, then you report this (gross) contribution on your tax return.” – I’m a higher rate tax relief virgin, could someone point me to the source how I could actually do this? I used to call HMRC and they were doing it for me but the caluculations they were coming up with were never matching my own, so this time I would rather do it the other way.

@Peter: If you’re not in self-assessment already (in which case you have to use self-assessment) then you have two options, either:

a). through registering for self-assessment and completing a return; or,

b). by writing to HMRC directly.

To claim through self-assessment, you will need an online self-assessment account. There are time limits and processes for registration for this and for completing an online return (e.g. 31 January 2024 for the tax year ended on 5 April 2023).

If you do go via this route, then you should go to the relevant section of the online self-assessment return and then state there the amount of your gross pension contributions, i.e. including the total of both your cash contributions and also the basic rate tax relief of 20% given on them at source.

Your higher rate tax relief will then be given as one of: a rebate at the end of the tax year, as a reduction in your tax liability, or as a change to your tax coding.

You can instead write to your tax office. You should be able to find the relevant address on your P60 or payslip.

Your letter should set out for HMRC how much gross you have contributed to your pension in the tax year in question, again including your own contributions and the basic rate tax relief on them given at source.

You will also need to provide details so that you can receive the higher rate tax relief.

You will need to submit a new letter every time you alter your pension contributions or your salary changes.

You can also claim for any previously unclaimed higher rate relief for periods in which you made pension contributions as a higher rate taxpayer going back up to four years after the end of the tax year that your claim relates to.

@TLI – wow!

The article is excellent @finumus but one additional metric might be worth considering for 20% tax payers. You are able to contribute the maximum of £60K or your annual income. You have a zero tax band on just over £12K with the personal allowance but with pension contributions the whole amount is given the 20% relief. So in theory if you could contribute your whole income you would benefit from an additional 20% of relief on that £12K.

Practically this is only possible if you have a large amount of savings / windfall, inheritance or a very well off partner who has reached their maximum contributions for the past 4 years. It worked for us when my wife was on maternity. Her earning had dropped significantly but I wanted to contribute once my own pension / ISA was maximised so she did not lose out looking after our child on having a pension and fell upon this little benefit.

@SemiPassive #11 and others

As well as the cumulative position (tax + NI) only being 10% (soon to be 12%) different between the standard 20% + 12% (10%) band to the higher 40% +2% bands. There are also lots of secondary tax benefits from sacrificing heavily from a higher rate into a standard rate. For example, any benefit in kind tax will be paid at 20% rather than 40% so cost of company cars, private healthcare etc etc will be halved.

@Finumus – Excellent article as ever!

@Al Cam #9 – always enjoy your insightful comments. Totally right, govt pension tax spin supported by the media, ignores the true facts, worryingly not sure Labour wish to recognise this, not all of us get a “Sir Keir special pension relief”… It would be great to hear your thoughts on choosing DC before DB, tax management etc as you say not many discuss this other than that other fine fella Ermine, appreciate you may not want to say too much. Cheers!

@Peter @TLI

If it’s for the current year, the easiest way to get the extra tax-relief is to do it online through your Personal Tax Account. You just have to provide an estimate of the gross pension contribution and HMRC will adjust your tax code.

@LdnGent (#23):

DB and DC can be a tricky dance – they both have advantages and disadvantages. A key disadvantage of a DB scheme is they are just not flexible, e.g. once commenced they cannot be paused. I would say any approach you adopt should be suited to your own situation – ie there is absolutely no one size that fits all. To some extent the approach you take will probably also depend on the respective amounts and a plethora of other parameters and/or personal foibles.

Personally, once I left paid work I set about trying to empty my DC before starting my DB. We have no kids so we are not interested in the IHT angle. Even if we did have kids I am not persuaded that this will stick around for much longer – but that is just my view. This meant most of my DC would ideally be drawn at the lowest possible tax rates. However, the situation changed as the plan unfolded and I am now involved in much more complex situation than I ever envisaged – primarily due to the freeze on allowances/tax bands. But so be it.

Trust this is of some use?

Nice article.

Re the last graphic – as I read the punchline first thought I’d been a moron by automatically trying to chuck in up to the annual allowance but appreciate the nuance of you can do a lot of speculation and forecasting or just shortcut it by concluding it can’t be terribly wrong to chuck in where you can provided you have “bridge” capital elsewhere to cover you pre 55 if you choose to retire earlier. And of course that you earn “enough” for above 20% tax relief to be relevant.

Been debating LTA elsewhere as the spectre of its reintroduction haunts me very directly at the moment. For those passing 55 feels like best strategy is to crystallize ASAP if past last LTA (assuming no protections) because say a pot of £1.3m is immediately reduced to £1.032m after max TFLS of 268k. Then you’re below if an LTA of circa £1.1m is reintroduced. Then assuming you still have income pay in or not based on the level of LTA actually introduced. Limited downside unless one thinks a future govt will suddenly hike TFLS cap which feels implausible at the moment – more like a reduction would still be politically acceptable to the majority of the population given general ignorance about pension provision and personal taxation.

Early (relative to need) crystallization of TFLS feels most no regrets. Though IHT inefficient that is almost certainly someone else’s problem. Gut feel that IHT privileged status may not last for long. Bit of a pain managing any gains in a GIA as you bleed it into ISA over time but hey-ho if you are getting meaningful CGT life probably isn’t too bad.

What am I getting wrong?

Perhaps worthwhile future article though acknowledged likely most relevant to 50-60 age bracket?

@BBB

I crystallised to the LTA several years ago and took the full TFLS leaving the excess uncrystallised. The TFLS didn’t fall out of the equation at that time but who knows what legislation may be introduced later. This week I requested crystallisation of the remaining portion paying the now standard rate @ 0%. It’s seems like a no brainer to me.

@Al Cam – very helpful, thank you. My situation has many similarities hence the interest, of course having to make long term decisions based on short term policy changes and stealth taxes makes the process even more challenging.

@LdnGent (#28):

Yup, it is tricky, but IMO inaction is not a great option either.

When I pulled the plug about seven years ago (gosh time flies!), I had the following primary objectives (which others may well see as daft – but so be it): a) to avoid an LTA charge; and b) never again pay HR tax. At that time, I was totally convinced that a) would be the trickier. Well, it did not turn out that way – and that was before Hunt scrapped the LTA! The jury is still out on whether I will achieve b) – but it is currently not looking too clever, and every revised inflation forecast just makes it worse!

Having said that, there are far worse problems to have and I have no real regrets !

@Al Cam #29. Surely you only need pay HR tax if your DB scheme (and/or annuity if you have annuitized) takes you above the threshold (which of course it might with DB inflation adjustments against a frozen threshold). If you still have DC pot on top then you either leave for a rainy day (glitch in the DB payor etc) or suck up the 40% tax. It’s something I’ve thought about too – what if my early plan to live off TFLS/GIA plus DC drawdown only to personal allowance means I’m not drawing at sufficient rate on my DC to avoid HR tax later when my non income taxable buffers are exhausted? Better to draw at 20% IT to have a bigger buffer in GIA? Feels it makes sense to draw at 20% if you have capacity and ISA shelter when your ISA funding sources are otherwise exhausted.

@BBBobbins (#30):

Re “(which of course it might ….

That is essentially the problem in a nutshell.

My solution was to overdraw for a few years from DC at BR (and park in a GIA) before commencing DB earlier than originally foreseen and try to get remaining DC flattened and into ISAs (along with GIA buffer) before SP starts …. bit of a faff, but looks about doable.

Paying HR to empty DC is a fail in my book no matter how irrational that may seem to others!

Very helpful article and great comments. I was thinking once you can take the full tax free pot then simply take it and put into a GIA. Then use this to buy gilts as mostly tax free. Drip into ISA if required. Then you can still put money into pension and get tax relief as not taken drawdown money. When you are ready to retire you have ISA income, GIA Gilts income as tax free (well almost) then take 4% from the pension to use your tax allowance . With reasonable care and 500k ISA pot i can see 15k from GIA 20k ISA 4÷ of 500k plus 40k from 4% 1m pension so about 47k tax free and 28k (40-12) post 20÷ of 23k which gives about 70k post tax and reasonably safe from inflation etc and when the state pension kicks in you can adjust as the GIA pot is probably getting rather small.

More generally, what should the investment strategy for a SIPP be now?

In my 70/30 portfolio I tend to have my equity in ISAs (in which Mrs Valiant and I are invested to the maximum possible), and keep the gilts, cash, gold in general dealing accounts, on the grounds that I hope over time it’s the equities that will generated the big bucks, so I want them sheltered.

I’m quite close to the LTA (actually, one of the higher ones; I have protection from 2012. In hindsight this was a mistake since the abolition of the LTA meant that I could have carried on contributing to the SIPP with impunity, but part of the deal for an enhanced LTA was that you had to stop contributing, and now I am no longer earning). Being close to the LTA meant that any substantial upside was likely to take me over it and thereby be heavily taxed, so I tended to keep it quite conservative with lots of gilts etc).

Now with the abolition of the LTA I suppose that should go out of the window, and I may as well replace the gilts in my SIPP with equities in the un-sheltered platforms.

Unless Labour restores the LTA …. 🙁

(It’s really quite disgraceful how governments of all kinds keep dicking about with the rules. We private sector workers need certainty that pertains over decades for effective pension planning).

Top marks for effort on this article! Very comprehensive, but you missed one trick I can think of. Some may be able to make savings on the 10% NI rate through salary sacrifice. That is being particularly picky though.

An additional advantage of DC pensions/SIPPs compared with GIAs/ISAs is the availability of uncapped inflation linked annuities at very competitive rates. This is the route we are going down at present with about 40% of our SIPPs. RPI linked annuities are about half the price they were a few years ago. Helped by higher annuity rates and Mr Hunt’s generosity in no longer taking 25% of the growth over the LTA.

One of the reasons for annuitising now is diversification. I cannot see how Labour could bring back the LTA in its present form, but they might bring in something more draconian that hits large DC pension pots hard.

@Sam (#12):

There is one key thing missing from your personal tax treatment of DC/SIPP vs ISA. That is the tax free lump sum (aka PCLS) from the DC/SIPP. Whilst the PCLS is now limited, in the vast majority of cases it will still tip the scales towards the DC/SIPP albeit it cannot be accessed until at least age 55. Other major things that often further tip the balance in favour of the DC/SIPP route include NI savings (via salary sacrifice) and employer contributions.

OOI, have you ever looked at the government tax take in a DC/SIPP vs ISA scenario (with or without a PCLS)? The results of such an analysis over reasonable timescales may be of some interest.

@Naeclue (34):

IIRC you do not have a DB and – like the rest of us – are not as young as you used to be, so IMO annuitising now could well be a smart move.

Great article and comments. Think different decumulation approaches and optimisation strategies are worthy of future content – although appreciate that individual nuances can be tricky to navigate.

18 months out from pulling plug – focus on building cash bucket and optimising partner’s SIPP allocation to maximise tax free income allowance in years 55 onwards. Should have started this earlier after she went back to work – but doing as much as we can against her part-time earning cap.

Very fortunate to be at the old LTA cap – with a DB & chunky DC pot – but cash flow modelling suggest we won’t clear the DC pot into our late 80s – so kids will benefit if IHT pension rules remain – yeah right.

TFLS destined to drop into offset mortgage in part, and also will add to cash bucket for short term living. ISAs and kicking off my DB early will also support the 55 to 67 journey.

More positive market sentiment/direction making me think that I might avoid the OMY challenge – let’s hope it continues…..

@Rosario and G, yes there are other benefits and checking my own work pension scheme it does seem there is some national minimum wage rule that prevents people sacrificing below a minimum gross salary of around £21/22k pa.

The good news is above a fairly low % of additional personal contribution past a certain minimum they seem to pass on not quite half of the employer NI savings. So for the bulk of my contributions I can effectively get either 36% relief (on 20% band salary sacrificed from January next year) or 48% relief on (40% band salary sacrificed) when you add everything up.

It’s a reminder for people to check the small print of their work pension. It may be better than you think. As long as you manage your income on the way out to be effectively taxed at 15% overall (e.g. not exceeding £50k pa taxable income) then salary sacrifice pensions trump ISAs for building retirement wealth for perhaps 90-95% of people. Especially if you are not planning to retire before 55 or 57 anyway so don’t need an ISA bridge.

Anyway I’m going off topic, back to the top 5% with their LTA woes 😉

I’ve worked on pension systems with Fixed Protections and know Labour will have a headache if they want to reintroduce the LTA because they can’t do a retrospective tax grab. So yes, expect to see a new ‘Fixed Protection 2025’ introduced.

@KeepOnKeepinOn (#36):

Any chance that a redundancy package could feature in your escape plan? Assuming you have a reasonably high savings rate and got a decent payoff this may go quite a long way in the “55 to 67 journey”. The maths is basically the same as that MMM popularised in his “The Shockingly Simple Math Behind Early Retirement” post; although it was well known before then.

@Al Cam (#38)

now that would be the proverbial “cherry on top”! Not lost on me, but can tricky to engineer. All being said – lucky that I enjoy what I do and work with nice people in a good company with good culture. However, work is work. In the meantime, keep to the plan…

@SemiPassive #37

I’ve stopped earning now but have made 2 x £3,600 contributions since the LTA was removed.

Now I’m rather wishing I hadn’t because, although my accountant advises that it’s likely, those contributions could jeopardise enhanced PCLS.

So I have potentially endangered a (450-267.5)= £182,500 tax free lump sump for less than £2,000 of tax relief.

I don’t expect anyone to feel sorry for me and my combination of good fortune and greed, but I am very resentful about the uncertainty of it all, especially when compared to how favourably public sector workers are treated.

ZXSpectrum48k I came to the same conclusion with my fixed protection of £1.25m If I make contributions now it will mean my tax free amount is reduced.

I’m a year or two away from stopping working. If I had more time my conclusion might be different.

@ZXSpectrum48k I came to the same conclusion with my fixed protection of £1.25m If I make contributions now it will mean my tax free amount is reduced.

I’m a year or two away from stopping working. If I had more time my conclusion might be different.

Excellent details, with some fascinating details.

For me, my simple rule number 1 has been for many years – don’t pay higher tax.

My second rule, achieve the above by putting anything earned over the basic tax allowance, into a SIPP.

Then let it grow.

@Valiant

Ouch – I have fixed protection 2014 (£1.5m & £375k TfLs), my understanding is that any new contributions invalidate the protection, meaning £268k tax free but no (current) lifetime allowance going forward. For me I’d need to put an additional £100k in with 40% tax relief to break even (theoretically).

My mistake was assume the 25% tax free lump sum was based on the notional (Dc+Db) combined pot and not each pot separately. Originally I was not planning on taking the DB TFLS, but now will probably have to. At least it creates some basic rate tax head room!

If I was you I’d be investigating reversing the transactions on the basis of vague/unknown rules/basically any excuse I could think of….

It’s too complicated and I’m too mean to pay for advice

@Boltt:

Clearly I do not fully understand your scenario, but can you not achieve the same effect by taking your DB pension a few years earlier?

@Al Cam

I have 6 tax years to drain as much of my DC pot at 20%/BRT as possible – starting the DB earlier probably makes my “never pay 40% tax again” even harder. There is an option to delay the DB by a couple of years to gain 10% uplift – I’d gain 2 years of DC drawdown year but gamble on how many years I’d live. Things would be easier if you could just transfer to spouse tax free

If you’ve applied for your protections before 15 March 2023, then contributions after 5 April 2023 will not affect your protections (i.e. your tax free cash entitlement):

https://www.gov.uk/guidance/taking-higher-tax-free-lump-sums-with-lifetime-allowance-protection

@Boltt: “My mistake was assume the 25% tax free lump sum was based on the notional (Dc+Db) combined pot and not each pot separately. Originally I was not planning on taking the DB TFLS, but now will probably have to.”

Yes, tax free cash isn’t an allowance you can use up per se. So if you don’t take your cash free cash from one pension, you can’t” make it up” from another pension.

@47 TDM

That’s awesome thanks – Valiant must be cracking open the bollinger as we type!

Now on to researching recycling rules and whether I can get pension tax relief on CGT

@Boltt (#46):

Got you, I think.

Is your DB schemes NRA 61?

If it is, then a two years DB deferral is not a biggie IMO especially if it helps to secure your HR tax objective. However, the 10% uplift seems mean to my eyes. Is it, perhaps, inflation plus 10%?

Excellent article, Finumus, lots of information to digest and pretty easy to follow pics

@Boltt

>> That’s awesome thanks – Valiant must be cracking open the bollinger as we type!

Please, Darling … Cristal!

Thank you for that, Details Man!

@A1cam

NRA 60, but a March birthday means a bonus tax year for the early retired.

You are right it’s 15.6% not 10% (I only estimated using the deferment increases)

@Boltt (44): “My mistake was assume the 25% tax free lump sum was based on the notional (Dc+Db) combined pot and not each pot separately.”

I assume this does not apply to you but, for the benefit of other readers, if the DC pot is actually an AVC associated with the DB, then they can be combined to work out the PCLS. I did this when I took my DB pension. I had a substantial AVC and was able to take it all as tax-free cash without reduction of my DB monthly payments.

@Boltt (#53):

15.6% sounds much better! And 60 to 62 is also probably not a biggie?

You [perhaps inadvertently] have raised an interesting point about DoB and how it is used in DB schemes. As usual, the devil is in the details of your scheme – and schemes often differ- but the date that you commence your DB and its relative proximity to your Birthday [and also the tax year boundary and whether the pension is paid in arrears or advance] can make a difference to the actual pension paid and the first time indexing is applied. If your scheme has a modelling tool it is definitely worth doing some what-ifs to have a look see. Failing that, a few carefully selected possible retirement dates sent to the administrators may help illuminate things.

@DavidV – thanks, yes Ermine pointed that out to me a while back – good to know for the lucky few, unfortunately not for me

@ A1Cam – birthdays and first inflation factor rules are rarely shared/discussed. We could do with a Pension actuary sharing some wisdom here. IIRC my rules are : if born on 1st,2nd, 3rd of the Month then pension starts being paid on 1st on month born, else 1st of next month (seems unnecessary strange). First inflation uplift is Prorata on 1st Jan – so if pension starts on 1st April you get 9/12th of RPI in Jan (ignoring caps etc)

@Boltt (#56):

I agree, some chatter on this aspect of DB’s would be good – FWIW my scheme rules are different to yours.

However, it may be more pressing for you if people shared their experiences of the nuts and bolts of drawdown, with a particular emphasis on their first time. FWIW, my experience has not been good and my solution is to allow plenty of time (typically starting about 3 months before I need the money) . Given your 55th Birthdays relative proximity to the end of the tax year this may not work for you.

@Boltt and @Al Cam

Defo up for hearing more on drawdown detail – watch outs, people’s experiences, tax optimisation, leveraging spouse’s tax allowances, etc.

With a Feb birthday – thinking of working into new tax year till May/June – unlock all TFLS – and head off on Lions 2025 tour in Australia. One of the many things on the list of to dos…!

@Al Cam, it is definitely a better time to buy annuities than 18 months ago, but I still hope it is a bad time to buy! I hope we will see another 10-15 year bull market.

Interesting thing about annuitising is that it will lower our SWR because the annuity rate is much higher than our current SWR. That means we can increase our gifting.

@TimeLike Infinity

You were wondering why the reduced AA only applies to DC, not DB. It’s because it’s an anti avoidance measure brought in as part of pension freedoms. Treasury was worried that, for employees over 55, employers would be able to make a substantial contribution to a DC pension, potentially of everything over minimum wage (salary sacrifice on stilts), which the employee could then draw out immediately to live on, with the benefit of the NI savings, the BR top up into the pension, and the tax free PCLS element. It’s probably a sledgehammer to crack a nut

@KeepOnKeepinOn (#58):

I have been doing an annual drawdown (d/d) since spring 2018.

I do one ad-hoc d/d per year and always schedule it to complete towards the end of the tax year. IMO there are several advantages to this timing, not least of which are: a) by then you should have a pretty good idea of your overall tax situation for that tax year and b) it minimises the amount you will be initially over-taxed – you will still be over-taxed (even once they have a pucka tax code for you) and will have to claw it back in due course.

A few other pointers follow:

1) Give yourself plenty of time. Do not be rushed into anything and whatever you do do not leave things to the last minute as the process is far from slick. The process often relies on phone calls and completion of paper forms that have to be posted to you and then completed, signed, and sent back in the post. Before I did my first drawdown I did locate a ‘warts and all posting’, but unfortunately it has since been put behind a firewall. There has been little improvement in the intervening years by my provider and their long promised online system, which to date I have used just once, was actually worse!

2) Be clear on what you want to achieve before you action anything. Flexible Drawdown vs UFPLS vs Phased retirement, etc, etc. Some folks may want cash to live on, others may want to re-invest into an ISA/GIA, etc, etc. How much money, when e.g. fixed monthly d/d’s may suit you better.

3) Establish that what you want to do is feasible with your provider (it may not be – as not all providers support all possible options). This may require you to change provider – which will take some time too.

4) Understand the timescales that the product provider can meet – i.e. get them to tell you as it is seldom written down anywhere in the supporting paperwork.

5) Note that if you do want to re-invest you will face time out of the market risk. Mitigations can be taken but these come at a potentially non-trivial cost.

6) Be clear if there are any other essential pre-requisites. IIRC I read somewhere that some providers are now insisting you have a Pensionwise session before they will touch your first drawdown. To my eyes this is a clear example of where the providers interests truly lie – the people you are most likely to interact with are primarily focussed on compliance/box ticking and have little, if any, understanding of the actual products/process.

I had always assumed that the process/experience would improve over time; but, if anything, it has actually got worse!

There is a lot to think about and many ways things can go awry. To give you one silly story: one year I was sent some forms with a SAE for them to be returned in. Unfortunately, the SAE was for the wrong address!

Lastly, my experience is mine alone. Having said that I have exchanged views since 2018 with others – at least one of whom has tried several different providers – and our experiences are all similarly disappointing.

Lastly, please DYOR and YMMV.

A great article and set of comments.

(Un)fortunately I’m subject to the annual allowance taper which gives a reduced annual limit of £10k. With a non-working spouse meaning a SIPP limit of £2,880, are there any other possibilities for pension saving, or is it just fill our ISAs, the kids’ ISAs and kids’ SIPPs?

Thanks

thanks Al Cam – appreciate the insights.

The question is what do you do if you are a high rate taxpayer, already max your ISA and you believe that you’ll reach your peak earnings in 5 or 10 years time? Do you invest in a GIA rather than a pension even though you have unused pension allowance? You can defer CGT in a GIA account, but you can’t really escape dividends tax if you want to invest in index funds.

#64 Rather depends on what your beliefs are about pension taxation in the future. Assuming some form of LTA is reintroduced in the future (perhaps a Lifetime Contribution Allowance – though I have no idea how that were to be equated with DB schemes ) you might be arbitraging between tax relied now at 40% vs future contributions at maybe 60/45% (or 50% if you are pessimistic).

If no LTA is introduced then it feels to me that pension is preferable to GIA UNLESS you simply are not going to be able to bridge the gap between retirement date and age 55/57 for DC/SIPP access on ISA alone. The main flaw in this is that spending down an ISA early means you lose the tax free growth in the future.

So in short you need to do your own calcs based on earnings expectations and possible retirement dates. It’s only the high earners over I’d say at least £200k that have the luxury of being able to fill everything optimally for all future circumstances and even then they are constrained by reducing pension annual allowances.

Thanks for the article of much interest. My DC pot isn’t approaching LTA levels but I am no longer contributing as have stopped working. One thing I hear sometimes is eagerness to take the 25% tax free lump sum as soon as eligible on the basis that it it might change in the future.

What I am not clear on is whether doing that renders the remainder unsheltered for tax purposes. If so it probably would not always make sense since the benefits of tax-sheltered growth could outweigh the benefits mitigating a future reduction of the tax-free lump sum by taking it now. Does anyone know if the remaining 75% becomes unsheltered from tax if you take your tax-free lump sum?

No DC is ” sheltered from tax” – beyond the TFLS element it’s all taxable as income. The advantage from leaving money in is that the growth might increase the amount you can take out tax free up to the new £268k cap.

A DC pot is sheltered from some tax. There is no CGT on investment growth. There is no tax on bond and cash interest. The only tax on dividends is foreign withholding tax and in some circumstances that withholding tax is lower than it would be in a GIA or ISA.

Withdrawals are of course subject to income tax and I expect a future Labour government will replace the LTA charge with something, for the larger pots at least.

@Naeclue

Thanks for the more nuanced answer which is of course correct. Perils of rushing a response.

retiring at 62 this year, money into my SIPP is a no brainer. Every £ (up to £60k) is tax free going in and for 5 years taking out 12570 x 5 is also tax free. Beyond the £12570 is 25% tax free saving in total £83,800 over 5 years. Living a healthy and good frugal life (I live on less than £20k a year) means I will pay little or no tax again.

Hello,

I have maxed out my ISA. I am in the 45% marginal rate of tax (£165k per year including bonus). I expect my pension will grow over the old LTA limit without any further contributions. My employer will contribute their 13.8% NI savings if I salary sacrifice my bonus.

I understand the maths that the 55% tax rate will effectively make me worst off if I contribute to my SIPP. However, does this not ignore tax on dividends/capital gains when doing the alternative and investing in a normal taxed trading account? I.e. If I can expect a 10% return in a SIPP, I cannot expect a 10% return in a trading account due to tax on dividends/capital gains. I’d say it’s more like 7.5% after tax. Therefore the taxed account will grow at a slower rate.

Appreciate your help if I’ve misunderstood!

Really enjoyed this in-depth article. I learned a lot.

One thing I don’t quite understand is why you picked £113.80 when talking abou salary sacrifice. You are assuming the employer will give 100% of the NI “savings” to the employee. Why should an employer do that? They won’t be saving any money here. It’d be simply a transfer. I am missing something here.

> Just set the investment choice in the company scheme to ‘cash’ and every six months or so transfer that cash from your company scheme to your favoured SIPP.

Could anybody point me to some resources that explain how to do this? I tried a search for say “transfer work pension to SIPP” and most of the results are about old workplace pensions that are not actively funded. I have a pretty standard workplace pension with Aviva. They have a couple of money funds and I’d be eager to investigate the possibility as I don’t particularly like Aviva.

Thank you in advance.

Thanks for this article.

We’ve been taking monthly UFPLS sums from our SIPPS for several years. Myself a small amount on which I pay some tax. My state pension is just under 15k and I now pay tax on it from this year. My wife we’ve been raiding her SIPP for the last few years taking just under the tax threshold of taxable income until she reaches pensionable age. We both pay in £2880 into our SIPPS and get the basic rate of Tax back (£720) We’re currently trying to equalise the amounts we have in ISA’s as I suspect the new Government will limit the saving in ISAs at some point.

My current concern is what Sir Kier said, an then retracted, is that the tax free PLS may be abolished. Should I cash in and take the full PLS now?

To confirm, the £60,000 pension contribution limit includes your own contribution AND any employer contribution AND the HMRC relief on these contributions?

@parguello

Yes, it does. This is what I meant in this section:

https://monevator.com/rich-optimal-pension-contributions/#:~:text=Scaling%20salary%20sacrifice

Thanks for the helpful read, Finumus!

“As we’ve seen, one of the major benefits of getting money into your pension is that, under the current rules, it’s outside of your estate for IHT purposes.”

This section may (sadly) need an update if I’ve understood right – Reeves announced that “from 6 April 2027, unused pension savings may be included in your estate for IHT purposes.”

https://thepeoplespension.co.uk/support-for-pension-scheme-members/know-your-pension/pension-basics/inheritance-tax-iht-changes-on-pensions-from-6-april-2027/