When I finally secured a huge mortgage to buy my London flat in 2018, I confided to a friend that I was excited but also nervous, because for the first time in my life I could go bankrupt.

My friend thought that was crazy talk. He knew I had enough in liquid investments – albeit mostly in ISAs, which I didn’t want to touch – to pay off the mortgage outright if I had to.

Maybe I was just trying to get out of buying the next round?

But I was dead serious and it wasn’t even difficult to imagine a scenario in which I lost everything.

A once-in-a-hundred years recession. Stagflation. Interest rates soar and the housing market collapses. The stock market crumbles – and my active investing does worse. Perhaps I try to trade my way through the unprecedented chaos and blow up completely.

After a few years of this I get ill and find it hard to work.

I’m in negative equity. A 1930s-style crash has toasted my shares. I’m spending the last of my savings to keep the lights on.

One day I update my spreadsheet on a now-ancient laptop and it shows I have a negative net worth.

The sort of thing that has happened to people throughout history.

All too plausible.

For whom the bell tolls

Of course I didn’t judge that my utter ruin was very likely. I’d hardly have bought with a mortgage if I thought bankruptcy was a 50/50 coin toss. Not even at 95/5 odds.

However I did see it was possible. Indeed I felt this new risk entering the fringes of my sense of self, like icy fingers reaching out from various potential futures. If I strained my imagination, I could almost see the hypothetical disaster lands in the distance – like Frodo and Sam seeing the smoke of Mordor from a sunny green hill, long before they get there.

This visceral reaction was not surprising to me. I’d always hated debt.

I’ve noted before that I’m pretty sure taking out the mortgage tilted my active investing. Particularly in 2018, when I was first getting used to having debt in the picture.

2022 felt much worse than previous bear markets, too. Previously I almost whistled through those.

When Liz Truss drove the ship straight into an iceberg – just as I was coming up to remortgage – I wasn’t whistling anymore.

There’d still be a long way to go, but I knew that any march towards one of my worst-case scenarios would start something like that.

“I wouldn’t risk it”

In my experience most people don’t think this way.

Rather, they see things as pretty binary.

People will take out a mortgage because they have a job and they can meet the payments. This makes the mortgage ‘safe’.

Or they won’t take out a mortgage because they are worried about what would happen if they lost their job, and house prices fell. Mortgages are ‘too risky’.

Of course, savvy Monevator types like us know both things are true, right?

Well yes – but then consider all the debate we have whenever we discuss paying off the mortgage versus investing.

I’ve been called an idiot who shouldn’t dare to blog about money for having a big mortgage while I’m also investing. At the same time I’ve been chided for being wary of leveraged ETFs by none other than Monevator contributor Finumus.

Or you’ll discover that those same people criticising me for preserving my ISAs while running a mortgage also have pensions and a big mortgage themselves. They are just bucketing differently to me.

The thing is, everyone is right!

Risk does increase expected returns.

At the same time risk increases, well, risk.

And not only along a smooth spectrum either, where riskier things are more volatile but if you ignore the noise you’ll be okay.

Also in a very Old Testament sense, where risky things can kill you.

Risk in the moment

Morgan Housel illustrated this brilliantly this week with a series of graphs. I won’t pinch them all (please read his excellent post) but here’s the gist:

The black line represents anything volatile. It could be the stock market, house prices, your income, your health. Perhaps a blend that represents how things are going for you right now.

The red lines are tolerance bands introduced by debt.

How much can you take?

It’s a notional concept – obviously if the stock market soared, say, that wouldn’t directly hurt someone just because they had a mortgage – so don’t take it literally.

Rather it shows how debt is narrowing your window of resilience.

Particularly if you have a lot of debt:

This is a great illustration for how I think about the interaction of debt and risk.

Even a lot of debt and tough times won’t kill you if things go your way.

And milder brushes with danger are soon forgotten.

It’s 2024 and Liz Truss is now just a writer of comic novels. (Or biographies or political treaties, I’m not sure which). As things turned out I was able to remortgage for 4.49%, not 8-9%. And my portfolio has healed.

But there are worlds where those things didn’t happen. They got worse than merely wobbly for me.

Meanwhile, my friend from the 2018 chat is now more nervous about money than he was back then.

What has always seemed to me a gung-ho attitude serves him well in business. He’s a far better entrepreneur than I could ever be.

But yoyo-ing towards the fringes of an eight-figure net worth and back as private markets boomed and bust over the past few years has taken its toll.

Interestingly, he paid off his mortgage a few years ago, when times were especially rosy for him.

Perhaps he was thinking about more than just my next round when we had that conversation, after all?

Apparently articles about the fag-end of my buy-to-let (BTL) portfolio are very popular. I don’t really understand why. Voyeurism, maybe?

Well, if writing them puts even one potential landlord off from getting into BTL then I’m doing them a service.

If you’re new, you might enjoy my first article in this series, about my formative days as a landlord in the 1990s. Or try the second about my one remaining property in London.

The only other buy-to-let I have left – hopefully, the third is currently sold subject to contract – is a Victorian terrace in a pointless London commuter dormitory town.

It’s a two-up / two-down with a small garden, and, enticingly for this particular street, it has an upstairs’ bathroom.

Finumus’ folly

I bought this house in 2001, for about £60,000. The first tenant paid me about £450 per month rent. So did the second, who moved in during 2004.

That gave me a gross starting yield of about:

£450*12 = £5,400 = 9%

I took out an 85% mortgage at around 6%, set to track 75bps over the bank base rate for 25 years.

My managing agent also charged me about 10%, leaving me with £4,860 net income annually.

That was set against my annual cost mortgage costs of…

£60,000*0.85*6% = £3,060

… so after the mortgage I was left with…

£4,860 – £3,060 = £1,800

…of cash leftover every year to go towards maintenance and repairs and so on, before I’d hit my cashflow breakeven point.

That was was all I needed really, since inflation would increase the rent and capital value over time.

And that’s where the profit comes from – in theory.

Rent reduction

The tenant from 2004 is still there. Which is why – spoiler alert – I’ve not sold the place.

Her initially fixed-term tenancy turned into a ‘periodic rolling tenancy’ after six months. And the rent, apart from one change in 2008, stayed the same until 2019.

That one change in 2008 was a reduction. The tenant lost her job and couldn’t afford the rent on benefits, so I lowered the rent.

Not by much mind, to £420 pm. It stayed there until 2019.

So no rent increase for 15 years.

Now on one level you might think that failing to raise the rent for 15 years is a bit of a landlording ‘skills issue’.

I’m aware that some landlords increase the rent by the maximum they think they can get away with every year. I am not one of those landlords, or at least I’m conditionally not one of those landlords.

The conditions are:

I’m not making a cashflow loss

You pay your rent on time

My tenant has paid the rent, on time, in full, every month for 20 years. I’m not going to do anything to upset such a tenant, while I can afford to.

I’ve experienced enough of the opposite variety – the tenant that pays no rent at all – thank you very much.

Near-zero gravity

Even though I was completely negligent in raising the rent for a decade and a half, it didn’t really matter from a cashflow perspective. Because in 2008, the Bank of England cut its base rate to near-zero. And it pretty much left it there until the post-Covid inflation wave.

With a base+75 bps tracker, I was paying only £600-700 per annum on the mortgage for more than a decade.

Yes, like £50 a month.

There was really no need to raise the rent from £420 per month when the mortgage was only costing me £50 a month, was there?

Well…

Costs and consequences

You might think generating some £300 p.m. of cashflow would make this property a compelling investment.

Not so much.

Old housing stock requires a lot of maintenance. There was always something, such as:

Garden fence blown down in storm (about once a year)

Garden shed collapses due to rot from the neighbours dumping plant material behind it

Replace all windows with UPVC double glazing (because she can’t afford to heat the place in winter)

Get a new front door because the old one is not secure

Get a new boiler because the old one died

Replace the electricity consumer unit because it’s not compliant

Replace the downstairs flooring because a flood caused by a plumping leak

Eventually replace washing machines, fridges, and so on

Also – you hear that dripping noise?

It’s surely only the sound of money steadily leaving my bank account, isn’t it?

Ahem.

The mould problem

This property has a small, downstairs ‘lean-to’ utility room and toilet out the back of the kitchen – along with the proper bathroom upstairs.

And the downstairs loo often suffered from mould on the walls.

I would find this out from my agent’s periodic inspection report, not because the tenant complained about it. I’d then immediately instruct the agent to send someone around to sort it out. I’m not the sort of landlord who wants to be letting sub-standard mouldy accommodation. This is far from my vibe.

Whomever the agent instructed would do something – I’m not sure what, but it cost me a couple of hundred quid anyway – to ‘sort it out’.

But inevitably on the next inspection report the mould would be back. And we’d go through the same cycle again.

This is all pretty normal. To be expected. Not a problem.

However the costs increased steadily over time – as you might expect, I guess – from £1-2,000 per annum at the start to a £3,000 run rate now.

Some years it’s a bit more. Some a bit less.

Economies of scale

Compounding this problem, the original letting agent – where I had known the principal – got sold to a larger group. Then that group got sold to an even larger group.

In theory this should have brought economies of scale. But in practice, you can probably guess what happened.

Service quality declined and my costs went up.

Although the core management fee remained the same, lots of other costs started appearing. Periodic inspections that used to be included in the management fee got an explicit charge. And the costs of their ‘independent’ contractors went up by a lot.

Section 24

Since we’re going chronologically, the government also introduced the Section 24 taxation treatment of interest expenses in 2017, staged over four years.

This made mortgage interest not fully tax-deductible. Essentially it meant that one now got taxed on turnover, not profit.

Since we didn’t really make a profit on this property anyway, we had to start paying a bit of tax on profits that we’d not made.

But with interest rates still very low, this didn’t – yet – make too much difference.

Banning tenant fees

The straw that finally broke the ‘not increasing the rent’ back was the banning of tenant fees in 2019.

These fees include things like reservation fees, credit reference fees, right-to-rent checks, and inventory fees. The sort of thing that, historically, landlords and agents had tried to stick on tenants at the beginning of a tenancy.

Now you might think these fees would be neither my nor my tenant’s problem, on account of the tenant having been there for 15 years?

I would agree with you. My agent though, not so much.

It decided to replace this revenue by applying a fixed surcharge on every tenancy of £15 per month (+ VAT).

This might not be a big deal if you’re letting somewhere for £2,000 a month. But with our £420 per month, that’s 4.2% of the rent.

I wasn’t happy about this. I even ended up having a chat with the CEO of the new-new merged agent about it. His point was, not completely unreasonably, that I was charging a massively below market rent anyway. There was no reason why I couldn’t just put it up by 5%.

With Section 24 also biting, I was set to lose about £500 to £1,000 a year on this property.

This is not much for a temporary bump in the cost of doing business, maybe. But the other problem was that house prices had stopped going up. In the absence of capital growth, I need the property to at least wash its face.

The other option, of course, is just evicting the tenant and selling it.

But was I really going to evict a single mother, with two kids in school – a reliable tenant, who has paid their rent on time every month for decades?

Honestly, I’d rather not.

Such are the unintended consequences of government policies to ‘crack down’ on greedy landlords.

Raising the rent

And so for the first time in 15 years, and with an immense amount of reluctance, I put the rent up.

Only by 5% mind. The agent feels you can’t really just double the rent to the market rent. You need to do it slowly.

The wisdom of just putting the rent up a little bit every year was starting to make a lot more sense now. In anticipation of interest rates rising at some point – and having crossed the Rubicon – I resolved to increase the rent by 5% a year until we got up to the market level. (The tenant was now in employment).

Since I’d just put her rent up, I decided to make a concerted effort to sort out the mould problem. And as I was between jobs, I took the time to go over there myself to take a look at it.

I unblocked the drain just outside the toilet in question. I removed a five-foot tree that was growing in the silted-up gutter pipe. Next I did a bit of repointing around the affected area. Then I replaced the tiles on the lean-to roof above. Lastly, on the internal wall, I stripped back all of the paint, all of the blown plaster, and re-plastered and repainted with the most toxic and reassuringly expensive anti-mould paint I could find.

It all took about a week of solid work. But I was quite pleased with the result, optimistic I’d sorted the issue out – at least for a while.

Of course on the next inspection the mould was back.

Show me the money

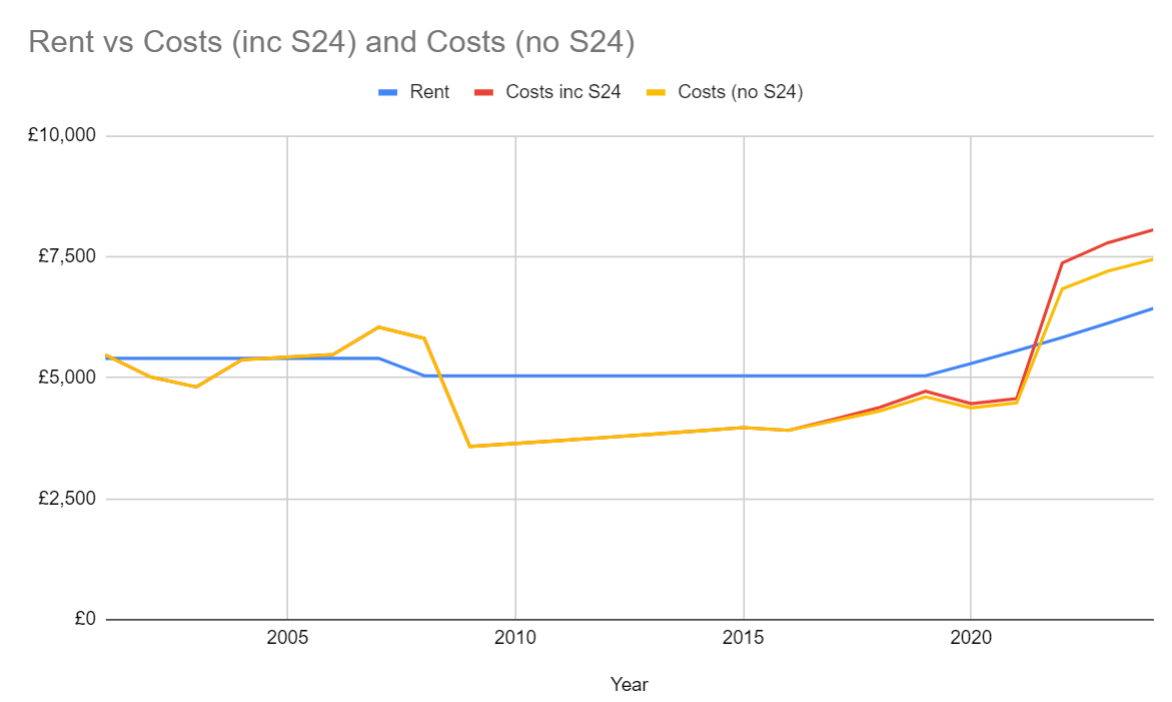

Finally, the post-Covid inflation arrives and I’m putting the rent up by 5% every year. Which for a while is actually a real-terms rent cut. 1

But this is fine, just so long as interest rates don’t go up…

…which of course they duly do:

From 2022 then, this investment has been making me a loss – even after I increased the rent.

And while Section 24 hasn’t helped, I would have been in the red anyway, on account of my costs and interest rates climbing:

Thankfully property is not my pension.

Shrug emoji

The zero net cashflow, the tax implications, the capital value of the house itself even, are not particularly large numbers in the overall balance sheet of the Finumus household.

It’s not causing me any great financial distress anyway. Which is fortunate for my tenant, I guess.

It does leave me feeling that providing free housing is not an optimal use of my capital. But here we are.

If things stay this way – they can’t, for reasons I’ll get to below – it would take about another five years of compounding 5% rent increases to get back to this house not losing money. (For what it’s worth, without S24 it would only be two years).

But there are a couple of other worries on the horizon.

The first is that my mortgage comes to the end of its term the year after next. Something will need to be done, likely something fairly binary. Either just paying it off or leveraging it up to the max loan-to-value.

I’m not sure which I should do. At some point I might need capital to fill ISAs. Leveraging up is a way of ensuring I have the capital to hand without evicting the tenant.

Secondly, there are quite a few policy risks floating about that could make things even worse.

Incoming!

The (hopefully) incoming Labour government will doubtless continue the trend set by the Tories of implementing economically-illiterate anti-landlord – and therefore anti-tenant – policies such as:

Rent controls: in which case I’ll need to raise the rent to market levels immediately.

Reduced repossession rights: in which case I’d likely have to evict the tenant and sell it.

Possibly something on Energy Performance Certificates (EPCs) or similar.

Slightly orthogonally: Labour could re-introduce the Pension Lifetime Allowance (LTA). This would cause me to reduce my pension contributions and raise my marginal tax rate, worsening my Section 24 problem. Though it would also see me retire earlier – which might fix my S24 problem.

None of which will help my tenant, mind you. But people respond to incentives, regardless of how much politicians like to pretend otherwise.

Cashing up

I’ve only made a few grand from annual cashflow on this investment so far – and even that will soon be wiped out.

But how much capital gain have I made?

Zoopla reckons the house is now worth £210,000. But it has not seen the mould. Let’s conservatively assume the house is worth £180,000 after selling costs.

This would imply I’ve made 200% in 24 years. A pretty underwhelming CAGR of 4.9%.

However £60,000 in 2001 is £109,000 in today’s money. Hence in real terms – that is, after-inflation – the CAGR is only 2.2%.

(Sadly we have to pay CGT on nominal gains, not real terms ones.)

This all works out at a post-tax, real-terms CAGR of…drum roll… 1.43%.

Now you see why everyone thinks BTL is such a money spinner.

As an aside, these sums also suggests that – based on the Zoopla valuation estimate – the current gross yield is only:

£6,432 / £210,000 = 3.06%

This at a time when 30-year gilts boast a 4.9% yield-to-maturity.

“MSCI are on the line about the mould again!”

Okay, you could argue that because I used leverage – and the tenant paid my mortgage interest for me – the actual capital invested is the deposit, not the purchase price.

The deposit was:

15% * £60,000 = £9,000

In reality there are a few more costs at procurement time – legal fees, new kitchen and so on. Let’s call those £6,000.

So £15,000 capital all-in.

This certainly makes the CAGR look much better. £15,000 in 2001 is £27,000 in today’s money. My £91,200 gain from £27,000 is a 6.7% real terms post-tax gain.

Not bad at all. But not great either, I’d argue.

Even with leverage we’re hardly knocking the covers off compared to the MSCI World index in GBP terms. And the MSCI World never calls to complain about the mould.

Certainly if I had the choice again in 2001 to do this or fill the ISAs (or was it still PEPs then?) it’s not obvious that BTL would have been the trade. Especially given the hassle. And this during a time when house prices were booming, apparently.

What’s more I’m not even sure whether working on the basis of the deposit is an entirely fair comparison.

Leverage increases risks, and I could have ended up underwater. Not something that would have happened in my ISA. [Well… – Editor, with a wry smile. But no, not underwater…]

Going forward, it’s hard to imagine house prices are going to rise in the next quarter of a century like they did in the last.

So when people ask me what I think about BTL – which weirdly, they do quite a lot – I just tell them not to bother.

Every morning at 9.30am in New York, a bell is rung at the famous Stock Exchange to signal the start of trading.

It happens again with a closing bell at 4.30pm – repeating a routine that’s watched by almost nobody in the actual business of investing.

Okay, a few hundred floor traders are prompted to think about which route they’ll take home. A giddy CEO from a biotech wonders if they chose a diverse enough team to join them on the platform for the bell-ringing ‘ceremony’ they coughed up for. A retired dentist in Florida watching CNBC growls as yet another day’s viewing has not revealed what sank her 3M stock.

Elsewhere, data whips around the globe. A high frequency hedge fund manager visiting a server farm coughs politely and suggests her cabling could be at bit closer to the wall. A thousand crypto bros ply their trades, day and night. And a fund manager in Tokyo curses himself for snoozing through his alarm and missing the US close.

Major currencies and bonds can now be traded all day and night from Monday to Friday.

But US equities can only be traded out-of-hours in a half-arsed fashion – via wonderfully-named ‘dark pools’ if you’re an institution, or even the internal markets of certain US retail platforms like Robinhood.

And that isn’t good enough for some people.

Be a part of it

24 Exchange – a startup US trading venue backed by hedge fund manager Steven Cohen – has been looking to take trading 24-hours for years.

Its latest submission is with the regulators. Meanwhile the New York Stock Exchange is polling interested parties about how non-stop weekday trading could work.

The Financial Timesnotes the survey is being conducted by the New York Exchange’s data analytics team, rather than its management. It seems like a fact-finding foray at this point.

And one can certainly imagine all sorts of technical obstacles – from staffing to liquidity to compliance – that would challenge a stock market rolling along for 120 hours on the trot.

On the other hand, doesn’t it feel sort of odd that we still have set market hours?

The whole show is run by restless machines these days anyway, while cryptocurrencies have given the younger human participants a taste for always-on trading.

Google news stories about the New York poll and you’ll find most of the coverage is from the crypto sites. Not a coincidence.

There’s even an intellectual argument for 24/7 trading.

A stock’s price is supposed to reflect all known information about that company and its future cashflows.

But if an earthquake happens in San Francisco on Monday evening, say, a US company’s price is basically a stab in the dark until Tuesday morning.

Investors who want to react to the news cannot do so – except via overseas proxies, the futures market, or those alternative trading venues I mentioned. All of which have their own issues.

It’s up to you New York, New York

Whether reducing these ‘blind spots’ in pricing overnight – and even, conceivably, at weekends – would produce more accurate prices overall is an open question.

Already out-of-hours markets are bedevilled with illiquidity and glitchy pricing.

Long-time commentator Felix Salmon warns “off-hours markets can be treacherous places for investors” and reckons any 24-hour equity market would be a ‘casino’.

Writing on Axios, Salmon also notes that institutions already do most of their share trading around the market’s open and close, when liquidity is greatest.

So most of them wouldn’t want anything to do with buying Tesla shares at 1am on a Wednesday.

That would make official nighttime trading the domain of retail punters – and of those who’d prey on them.

Which probably wouldn’t end well for the punters.

“As any casino will tell you, risky gambles are more popular at night,” Salmon concludes.

Contrarily, some European insiders are discussing actually reducing trading hours on the continent. European trading hours are currently two hours longer than the six-and-a-half hours seen in the US.

The aim would be to shore up liquidity, rather than spreading it even thinner over a longer trading window.

These little-town blues

Where any of this would leave the poor old London Stock Exchange is anyone’s guess.

For many decades London profited from being in a convenient timezone between Asia and the US continent – as well from its ultra-close proximity to Europe.

Would London have more or less relevance in an always-on trading world?

Or are we anyway on a path to one exchange – in New York, which is already home to around two-thirds of global listed equities by value?

Who knows, but in the meantime the London market’s struggles continue.

This week we saw DarkTrace, Tyman, and Hipgnosis agree to bids from overseas acquirers. The £2bn drug maker Invidior also confirmed previously mooted plans to shift its primary listing to the US.

All in a day’s work for the shrinking LSE.

AJ Bells’ investment director Russ Mould warns the volume of firms being snapped up means “the UK market is experiencing death by a thousand cuts.”

Still, it’s an opportunity to profit if you’re an active investor. At least it is if you can figure out what’s truly cheap and/or potentially attractive, versus what’s a conked-out value trap. (Harder than it looks.)

Needless to say, passive investors owning global trackers can ignore all this noise with a wry shake of their heads – and then continue to go about their business of compounding their long-term gains, regardless of how and when the underlying shares are traded!