Even the most strategically disinterested passive investor – that’s a compliment, incidentally – will know that the biggest US technology firms were what drove global equity returns higher last year.

I featured dozens of links in 2023 to articles charting the rise of the so-called ‘Magnificent Seven’.

Behemoths such as Microsoft, Amazon, Apple, and Alphabet that couldn’t possibly get any more highly-valued. Until they did!

Broaden the lens to the asset allocation level and things were almost as skewed. Not only did a handful of mega-cap equities drive returns – but equities, especially US ones, were really the only game in town.

And let’s not remind ourselves of the nightmare of 2022.

But okay, if we must then you’ll recall it was the year that diversification utterly failed and pretty much every asset went down. Starring, of course, the worst bond bear market in several generations.

Very high inflation and rising rates sent bond yields soaring and bond prices crashing.

This was not unpredictable given the pace of rate rises (which were unpredictable).

But it did make one despair of owning a diversified portfolio, and saw the 60/40 portfolio written off as dead (again).

Last year already proved that particular obituary to be premature (again, again). Especially in the US.

But while an end to the free fall in bond prices didn’t hurt, the truth is the 60/40’s decent showing was in no small part due to those biggest tech companies returning 50-100% or more in a single year.

So diversification worked, but only because it didn’t get in the way of what really worked.

Risky business

This all-conquering short-term dominance of equities is not an inevitable state of affairs, as this graphic from Legal and General’s 2024 outlook explains:

The graph shows that from around late 2001 to 2014, investors were rewarded – on a risk-adjusted basis – for having diversified portfolios, compared to if they’d only held global equities instead.

Since then though, more often than not owning anything but equities has been a drag.

This probably won’t last. Not least because high-quality government bonds now boast nominal yields of 4-5% or more thanks to the big sell-off, as opposed to the 1% or so they touted before it.

But also because sooner or later the global slowdown we’ve been promised for 18 months should finally arrive, even if it’s a mild one – and because central banks are due to start cutting rates regardless with inflation falling.

Given all the argy-bargy unfolding on the geopolitical scene, I’d certainly take a recession as the casus incisusthat sends bond yields down and hence lifts bond prices – in preference to the potential casus belli rattling across the news.

Indeed Legal and General’s head of asset allocation says:

…this is, in our view, not an environment in which to bet on the concentration of risk. One might be lucky and avoid a crisis but if not, performance could be terrible.

Instead, we believe it’s a matter of spreading risk over multiple regions and multiple return drivers.

Over a longer horizon, we believe diversification should outperform more concentrated portfolios on a risk-adjusted basis.

The historical average of the difference in Sharpe ratios is in favour of diversification, according to our calculations.

First among equals

As I’ve written before, it’s conceivable we’ve entered a late-capitalism endgame where the half-dozen or so mega-companies that got to scale just as AI arrives have the data pools and moolah to win forever.

In which case prepare for either a terrifying dystopia or Ian M. Bank’s culture, to suit your taste.

It seems safer to bet though that the stock market is having one of its moments. That, magnificent though these market darlings indisputably are – perhaps the best businesses we’ve ever seen – they won’t prevail perpetually any more than Vodafone, Standard Oil, or the Dutch East India Company did before them.

In which case it’s probably best to keep a sense of balance. Not least in your portfolio.

Remember Jake, who used geo-arbitrage to escape the rat race? We’re back in the Monevator snug to hear from the man himself whether his FIRE reality has lived up to the dream, one year on.

I have often found myself reflecting on life during the last 12 months. Especially so at a funeral I recently attended.

It was nice to hear all the stories and kind words that people had to say about this individual. Inspiring to hear how positive they were during their lifetime. A glass half-full kind of person.

I have had inflection points like this before. Unfortunately over time the light dims on them.

This time I aspire to be more intentional. There are only a limited number of good healthy years left.

FIRE by the numbers

Financially our first 12 months of FIRE went well. Our net worth on 1 Jan 2024 stood at £964,000.

For the sake of clarity, the net worth in my original FIRE-side chat was the value I took on a random day in early 2023. Specifically our net worth (excluding our house) on 1 Jan 2023 was £845,000.

This net worth figure climbed above £900,000 (again excluding our house) for the first time in June and stayed above that level for most of the rest of the year, with the brief exception of October.

We spent just under £32,000 during the year. That amounts to a 3.77% withdrawal rate.

We had been heading for a 3.30% withdrawal rate with a total spend of just under £28,000. But at the end of December we booked a 2024 family holiday at a cost of £4,000.

One caveat to our 2023 spending is we did not go on holiday. Instead we had plenty of family days out during the school holidays. Although we did book and pay for that 2024 holiday, we’ve yet to enjoy it!

There was approximately £3,000 of spending on a few (hopefully) non-regular bits, including some plumbing and insulation work.

Investing in the face of inflation

All the asset values in our net worth are nominal, and of course our net worth in real terms has been impacted by the recent high inflation.

We are heavily invested in equities, which hopefully will offset some of the negative effects of inflation.

Still no bonds and we’re still overweight America. I know this goes against the conventional wisdom out there. But currently I seem to have a mental block as I can’t bring myself to diversify into bonds and a world tracker. I may have to learn this lesson the hard way.

Having neither worked nor received any salary for a year, it’s a slightly surreal feeling that our nominal net worth has increased during this time – despite 12 month’s worth of spending being deducted.

It’s notable too that thanks to the price of most things we buy going up with high inflation, our bills are bigger than I might have expected had inflation remained subdued.

We are in the fortunate position that we don’t have a mortgage, and thus have not suffered at the hands of higher interest rates like so many homeowners.

Undercover escapees

During the past year I’ve attempted to adjust my mindset towards being more flexible with our spending, as opposed to my previous accumulation, saving, and investing mindset. The decisions and actions we took before are not necessarily what’s appropriate in our de-accumulation life.

I don’t mean spending large amounts of money on unnecessarily expensive items. Rather, spending little and often so we can enjoy days out together as a family, especially while our children are young.

I still look for value for money. But I want to put more emphasis on the joy that our family will gain from these experiences.

We’ve still not told people in our local area of our situation as financially independent early retirees. Only our family and old friends are aware we’re no longer working.

Most of the people we know in our local area are parents whom we’ve met via our children. I’ve observed the way some of them talk about money, finances, and wealthy acquaintances. The impression I have is that a lot of our new network are middle-earners who appear to put more emphasis on spending money, rather than saving and investing.

I think some may have mindsets too entrenched to appreciate the long-term hard work, planning, difficult decisions, grit, and delayed gratification that helped us arrive at where we currently are.

In contrast, having lived through it I’m obviously well aware of all the work I did that provided the money that I then invested, which in turn enabled me to leave that world in the rear-view mirror.

During the last couple of years at work I had an on-going internal debate of when enough was enough. I could have carried on for another year or two for the extra money, or because I was scared and fearful of the risks involved. But mentally I felt I was in the fast lane to burnout. I needed to end the journey.

Going with the flow

It’s surprisingly difficult to explain how we’ve spent our time since I left work.

Our days are still structured around our children and the school run. Which, for example, stops us from spending the whole day away from home. But I really treasure the time on the school run. Children grow up so quickly and I missed this in the early years.

Some of my time has been spent recovering from the stress, anxiety, and tension that I felt daily while in the corporate world. I’m learning to try and look after and understand myself more. To be kinder to myself, to not to be so self-critical, or to put myself under unnecessary pressure. I keep reminding myself that I can slow down.

There are some days when I don’t want to do anything, so I don’t. My mood may be low. Doubts and negative thoughts can creep in. Then there are other days when I feel the need to accomplish something. It’s nice to be able to listen to my body and mind when deciding what to do for the day. Rather than having the decision taken out of my hands by the corporate machine, as in my previous life.

I often spend time outside in the garden tidying up or going for walks around the local area. This enables us to enjoy the simple pleasure of observing the changing seasons. I’m fishing again, which is a wonderful way to spend time outdoors close to nature. If the weather restricts me to indoors, I will potter about, listening to music, reading, catching up on Monevator articles, doing household admin (I still write to-do lists), planning little projects. Sometimes I like to just sit down in peace alone with my thoughts.

This may not sound as exciting as some envisage their future post-work life to be. The excitement comes in different forms. Being able to observe our children develop and grow – witnessing those moments that bring them joy and intrigue without the interruption of the next urgent work emergency – is priceless.

Five things that went as planned

Financially we were fortunate that the winds of the American markets were behind us in our first year. This helped ease the initial fears of dealing with the de-accumulation phase and sequence of return risk.

My wife and I are in this together as a team. We have a joint objective to enjoy and make the most of our new family lifestyle.

In moments of contemplation, I’ve realised that giving up employment is not as scary as I had built it up to be. It’s easy to focus on the worst-case scenarios and ignore the potential benefits.

There is a feeling of freedom to finally have control and independence over our time, finances, and our direction of travel as a family.

The work-related stress has disappeared and hopefully over time this will benefit my long-term health. I sometimes smile to myself at a distant memory of a former boss misunderstanding me once again.

Five things I’ve learned or recalibrated

I had a fear that my work had become the main part of my identity over such a long period of time. It was a very stressful and demanding role that I found little enjoyment and even less meaning in. The jury is still out as to whether I’ve managed to re-discover who I was before my sentence in the corporate world.

There is not as much time available as you dream there will be, especially with children. I have multiple ever-increasing to-do lists on the go at the same time. I’m not sure how we ever managed pre-FIRE!

I’m still trying to understand if I need more structure in my day, in addition to the school run. Fortunately, there are no imposed deadlines on discovering what works in my new reality.

I suspect I haven’t fully decompressed since leaving employment. Being able to relax is a skill I am slowing re-acquainting myself with.

I wrestle with the dilemma of whether I should tell people that I’m no longer working. I have almost been caught out on a couple of occasions when people have asked how work is going, or whether we have any time off over the holiday period.

Closing thoughts

After a long and sometimes frustrating journey, we arrived at destination FIRE. And just like that, we are already advancing into our second year of early retirement.

We have the freedom to live the life we want on our own terms. There are potential risks on the horizon and plenty of challenges to overcome. But we feel we’re in a better place to prosper as a family.

Thanks so much to Jake for letting us know how he’s faring with FIRE. It’s good to hear from the other side of the rainbow! But what do you think readers? Should we make such occasional post-FIRE follow-ups a feature of the FIRE-side chats, or would you rather we focused on new stories?Please let us know in the comments below, along with any reflections or questions about Jake’s experience.

I began drafting today’s post on Wednesday, observing that while 2024 had begun with a splutter for most markets after the almighty Santa Rally, Bitcoin was still going strong.

How come?

Just like the others, Bitcoin has benefited from the emerging consensus that central banks will begin to cut interest rates this year. Perhaps markedly so.

Any asset that pays no income will surely benefit when the competition from cash recedes.

But there’s been at least three other narratives driving the Bitcoin rally:

A widely-held conviction that the SEC in the US is about to approve at least one Bitcoin ETF

The upcoming ‘halving event’ in April, which will halve the rate of release of new Bitcoins to miners

The fact that the latest cypto winter didn’t kill Bitcoin, despite all those bankruptcies and felonies. This must have made it stronger

It all helped Bitcoin’s price advance around 150% in 2023 – albeit after an epic crash the year before.

Things that go bump in the price

Yet no sooner had I hit ‘Save’ on my draft than this happened:

Yes, the Bitcoin price fell more than 10% in about ten minutes.

So much for the asset class growing up!

As I write, the cause of Bitcoin’s latest moment of madness appeared to be the opinion of a sole analyst.

Marcus Thielen of crypto platform Matrixport was quoted by The Block as saying:

“SEC Chair Gensler is not embracing crypto in the U.S., and it might even be a very long shot to expect that he would vote to approve bitcoin spot ETFs.

“This might be fulfilled by Q2 2024, but we expect the SEC to reject all proposals in January.”

Now, I can’t imagine why the SEC might be leery of green-lighting a retail-friendly ETF for an asset that dives 10% on the opinion of a single analyst in about the time it takes to Google it.

It’s not the message so much as the market that’s the problem here.

Everyone’s not a winner

Bitcoin remains a thinly-traded and illiquid asset.

A relatively small number of so-called ‘whales’ own a huge proportion – around 40% – of the outstanding stock. (Or at least all the stock that’s available that hasn’t been lost to Welsh landfill and the like.)

Indeed it’s not clear to me what diehard HODL-ers like Michael Saylor of MicroStrategy see as the endgame for their remorseless Bitcoin accumulation.

I obviously understand that scarcity can push up the price of a desired commodity.

But when that commodity’s only proven use case so far is as a (hugely volatile) store of value, surely that’s undermined if only a hundred or so entities control so much of the supply?

How will all the other stuff Saylor talks about with Bitcoin happen if it gets so closely-held that it becomes very hard to actually buy – and potentially use – it?

I suppose that the new financial order they predict (note: I don’t) could run with only tiny or even notional bits of Bitcoin changing hands. Maybe these massive holders will then act as de facto central banks?

Maybe, but I don’t remember reading about that in Satoshi’s white paper.

A stake in one future

Still, I continue to believe that brave – or crypto-enamoured – private investors can justify holding up to a few percent in Bitcoin or Bitcoin proxies such as MicroStrategy or the Bitcoin miner Riot Platforms.

For what it’s worth I do – despite some ongoing befuddlement.

Bitcoin and blockchain are among the most intriguing innovations of our time. But one has to acknowledge the vast range of potential outcomes, from Bitcoin going to zero, right up to it backing fiat currencies or being the preferred currency of powerful AI agents in a William Gibson-esque dystopia.

Hence why I’ve argued a small allocation that’s left to boom or bust is a practical response.

The trend is your friend

Of course this strategic inactivity might be severely tested if Bitcoin actually ten-bagged in a year.

And we can well imagine that a Bitcoin ETF could be very bullish for the Bitcoin price. It would make it easier for individuals and institutions to buy a small stake of the diminishing pool of free-floating Bitcoins.

As I believe a higher Bitcoin price is a self-fulfilling prophecy when it comes to the future price of Bitcoin, so higher prices should gradually de-risk the asset class by itself. At least for a time.

But others think differently, of course.

Some even say ETF approval would be the death knell for Bitcoin, because it would curb those exotic use cases.

Others just ridicule what they see as an unusually hard-to-kill tulip-mania.

We’ll have to wait and see.

Incidentally my comments here relate only to Bitcoin. I have no conviction about the other cryptocurrencies.

It is not that I’m certain they will all fail. If Bitcoin endures and delivers anything like a decent return, then I’d bet in that particular world that a few of the other thousands of cryptos will do very well, too.

It’s more that in any outcome where any other particular crypto currency succeeds, I think Bitcoin will be at least okay – as digital gold, if nothing else – even if it’s not the standout performer.

In contrast, in all eventualities it seems obvious that the majority of Bitcoin’s thousands of rivals will amount to nothing, even if a dozen or so do thrive. There’s just so many out there.

Hence Bitcoin seems the median risk bet.

Putting 1-5% into a cryptocurrency is plenty enough risk already. So I’ll do whatever I can to reduce the uncertainty!

One of the most frequent questions I get on Twitter/X is: “Which investment platform do you use?”

I don’t really know why people ask this in a world where the excellent Monevatorcomparison table exists.

Disclosure: Links to platforms may be affiliate links, where we may earn a small commission. It doesn’t affect the price you pay nor how we judge the brokers.

However there are a few real-world issues that are out-of-scope for the table’s aggregated roundup.

So today I’m going to treat you to a tour of every investment platform (or ‘broker’) that I use and why.

Disclaimer: I will be stating my opinion based on experience. I do acknowledge though that I may have made mistakes, been misled, or that I could be confused about things. I’m happy to be corrected in the comments. None of this article is a recommendation to use (or a recommendation not to use) any particular investment platform. Brokers are also welcome to DM me for clarification. Especially if it means they’ll sort out some of the things I’m complaining about.

Behind the scenes at the Finumus family office

First off, why do we use more than one platform?

There are a couple of reasons:

No one platform does everything we want

We don’t want all our eggs in one basket:

Yes, I know, there’s the FSCS. But it’s capped at an only moderately useful £85,000

Yeah, I know, assets are held in segregated client accounts 1 Well, sorry – I used to work in this industry and I don’t trust it

I’ll only be discussing platforms that I have direct experience of using on a fairly frequent basis. These are:

IWeb (essentially the same as Halifax Share Dealing)

IG

X-O (part of Jarvis)

Interactive Brokers

Yes, that’s quite a lot of platforms. There used to be even more! Platforms we’ve previously used but that we no longer do include:

iDealing

Barclays

Charles Stanley

I’ll let the reader draw their own conclusions from my change of heart.

Finally, when I say “we” I mean the Finumus ‘micro family office’. This is a portfolio of ISAs, SIPPs, and so on that I nominally manage holistically across three generations of our family, along with our Family Investment Company (‘FIC’).

Family linkage

Our micro family office set-up raises the first feature we like to see – some sort of ‘family linkage’ capability.

Both Hargreaves Lansdown and AJ Bell make a reasonable go at this. Account holders can nominate another account holder to manage the investments in their account. The managing account can then log in as themselves and flip to the other person’s account – without needing to share credentials – and without access to payment capabilities.

This is very useful to me for looking after the accounts of parents and children in a secure way.

Good as it is though, the family linkage is slightly hobbled. A prime example is that you can’t take any of the so-called Appropriateness Tests for things like complex products by proxy. Which is particularly annoying when you’re trying to rebalance into something that the investment platform has arbitrarily decided is ‘complex’.

You’re left having to phone Grandma to talk her through the test. If she’s on a six-week cruise at the time you can forget about it.

However, even when hobbled, these options are much preferable to those investment platforms that don’t offer this facility at all – which is every other one on my list.

Whatever the platforms’ reasoning for the lack of any family linkage, in the real world it leaves you having to insecurely share credentials – which is far from ideal – and in some cases having to call family members for a 2FA code every time you want to login.

Investment platform costs

We are less bothered about annual platform costs than we are that they should not scale with our AUM 2.

So we like fixed or capped costs.

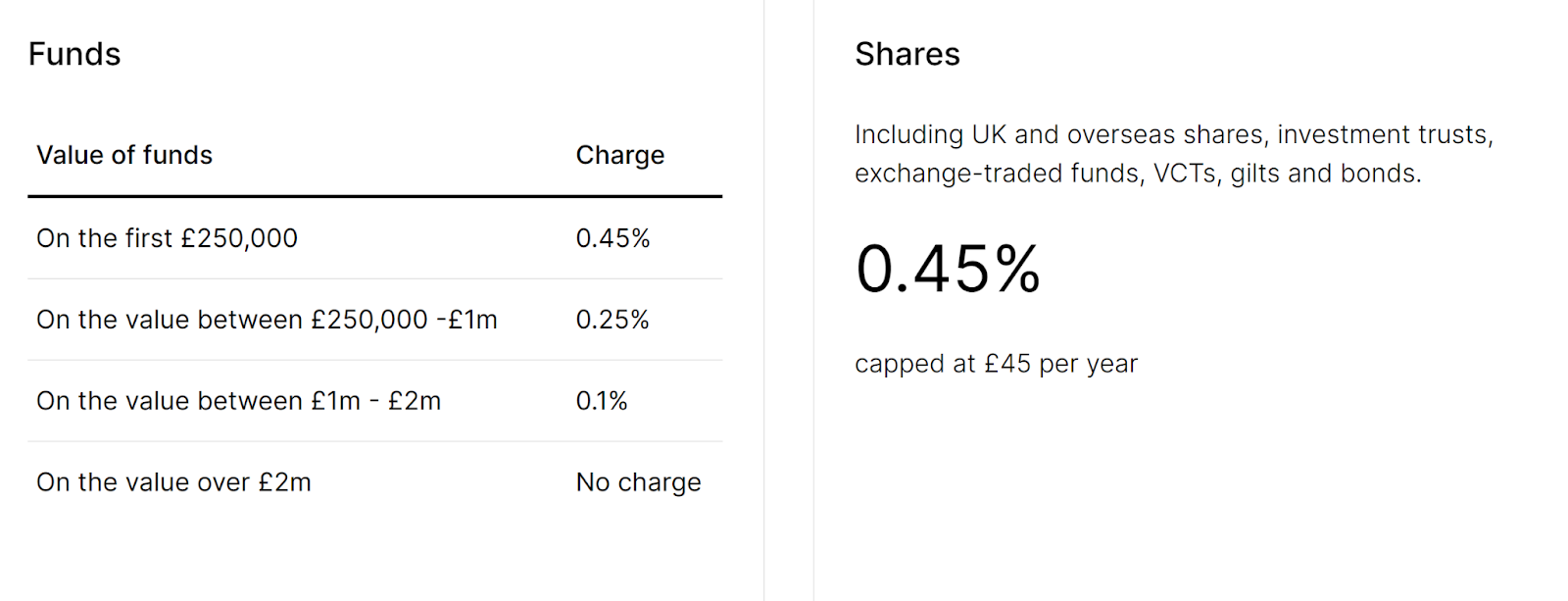

All our accounts are already over the value where the cap is kicking in. For example, Hargreaves Lansdown charges 0.45%, capped at £45 p.a. 3 while AJ Bell charges 0.25% capped at £42 p.a. 4 (as long as you don’t hold funds). That’s just £45 and £42 respectively fixed, as far as we’re concerned.

All told, our annual platform costs range from £0 (XO, IWeb) to a couple of hundred pounds (at Interactive Investor – but that’s for an ISA and SIPP) per platform, per person.

I don’t have anything else to add on this subject beyond what you’ll find over at the Monevatorcomparison table.

Does your investment platform charge extra for funds?

Perhaps because the regulator banned kick-backs from the fund managers to the platforms, some of the latter seem to have decided it’s okay to replace the revenue by charging customers higher fees for funds.

Right… Owning £2m of an ETF costs me £45 a year, but owning £2m of the same fund in an OEIC (Open-Ended Investment Company) costs me £4,000 a year.

What extra work is Hargreaves Lansdown doing to earn that £4,000? Absolutely nothing as far as I can tell – as evidenced by the fact that platforms like IWeb and Interactive Investor charge zero to hold that same fund.

Because we don’t really believe in active management and there are equivalent-cost ETFs for nearly everything we want, we only own one OEIC type fund.

And – duh – obviously we hold it across the investment platforms that don’t charge extra for it.

Note that none of the above applies to ETFs. Even though they have ‘fund’ in the name, ETFs are treated as stocks on platforms that charge high fees for funds.

Dealing costs

We don’t trade particularly frequently, so we’re not very sensitive to dealing costs.

That said, Hargreaves Lansdown charging £12 a deal doesn’t feel very 2024 to be honest.

The £5 that IWeb charges seems more reasonable. It’s notable too that AJ Bell is reducing its dealing fees from £10 to £5 in April 2024.

Again, see the Monevatorcomparison table to stay across all this.

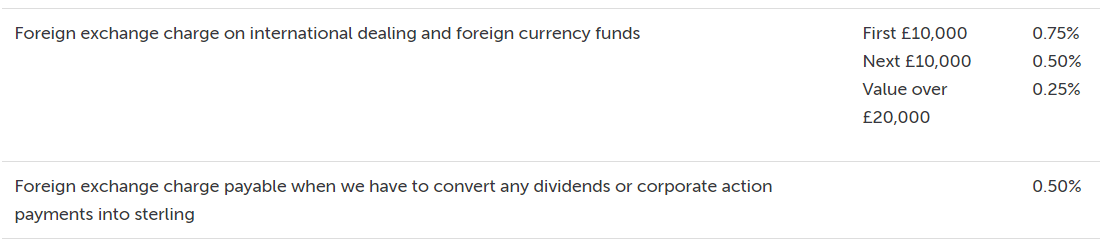

Foreign exchange (FX) fees

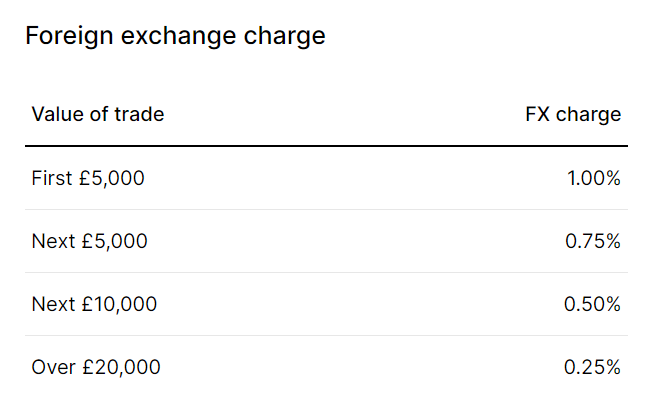

If you’re not careful, FX fees can really cost you.

The example on IWeb’s website features a notably sub-sized £1,000 trade. Perhaps because 1.5% on a more sensible £5,000 – £75 versus £15 – would seem like quite a lot?

A shame, because IWeb is such good value on every other vector.

To illustrate how much of a problem high FX fees can be, let’s switch £100,000 worth of Microsoft stock into Apple. A trade which – given the liquidity of US markets – you’d expect to cost a few basis points.

Here’s the deal:

Generously, the platform doesn’t charge commission. So the switch will cost me a mere £2,977 – or 298 bps of the notional.

Maybe let’s not bother doing the trade after all, eh?

Costly foreign adventures

There are two problems with high costs for foreign exchange.

One is when the FX fees are high, obviously.

The other is when you have to settle everything into GBP 5. Our example switch above saw two rounds of FX pain, because we can only hold GBP cash in the account.

Now, in the case of ISAs, this is not the platforms’s fault. It’s what the ISA rules mandate.

But still, a platform doesn’t have to charge an FX spread you could drive a bus through.

In contrast, here’s the FX fee over at Interactive Brokers:

Interactive Brokers is a full 50 timescheaper than IWeb when it comes to FX fees.

Let’s math out that same switch in an Interactive Brokers ISA:

The trade costs us £63 (6.3 bps). Quite a lot less than £2,977.

Naturally, it’s still not good enough for me though. What I really want to do is keep the proceeds in the base currency of the instrument traded, usually USD 6. That way I don’t need to pay any FX fees when I switch between assets in the same currency. Why should I?

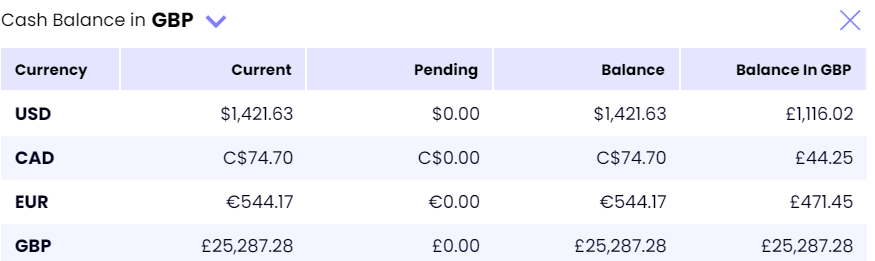

Outside of an ISA you can do exactly this with several platforms. But a grand total of two brokers in my list enable you to do this in a SIPP: Interactive Investor and Interactive Brokers.

Here are the current cash balances in my Interactive Investor SIPP:

See all those lovely hard currencies?

It’s something of a happy coincidence, because US stocks are best held in a SIPP. So this way you do not have to pay any dividend withholding tax on your US dividends, at least not with sensible platforms.

(In theory the withholding tax exemption should also apply to Canadian stocks. In practice it doesn’t.)

Both Hargreaves Lansdown and AJ Bell are big behemoths. They have the wherewithal to support multiple currency balances and settle trades in the instrument’s underlying currency within their SIPPs.

One way to avoid sneaky FX fees is to only buy ETFs for overseas exposure, and to always buy the GBP share class.

This way, your FX exchange happens inside the ETF wrapper at a much better rate / lower spread.

Since the underlying currency of most ETFs is naturally not Sterling, you should buy the Accumulation units to further reduce FX friction. Otherwise your dividends will be paid out in USD, which will then be FX-d into GBP at the platform’s spread and so bleed out another few bps of cost.

For instance, let’s say we wanted to track the MSCI World. We could buy the iShares Core MSCI World UCITS ETF USD (Acc) – whose base currency is USD – and specifically the GBP share class to avoid egregious FX fees:

Beware: a cunning trick sometimes deployed by platforms is to act like the GBP share class doesn’t exist.

You look up the ETF in its interface, you’ll only find the USD share class.

And when you complain, it’ll give you some blather about liquidity, or tell you that it “can only carry one share class of each ETF” – presumably because some numpty decided to use ISIN as the Primary Key in the investment platform’s product database.

Cock-up or conspiracy, limiting choice like this leaves you paying the platform’s FX fees.

Investment platform says “no”

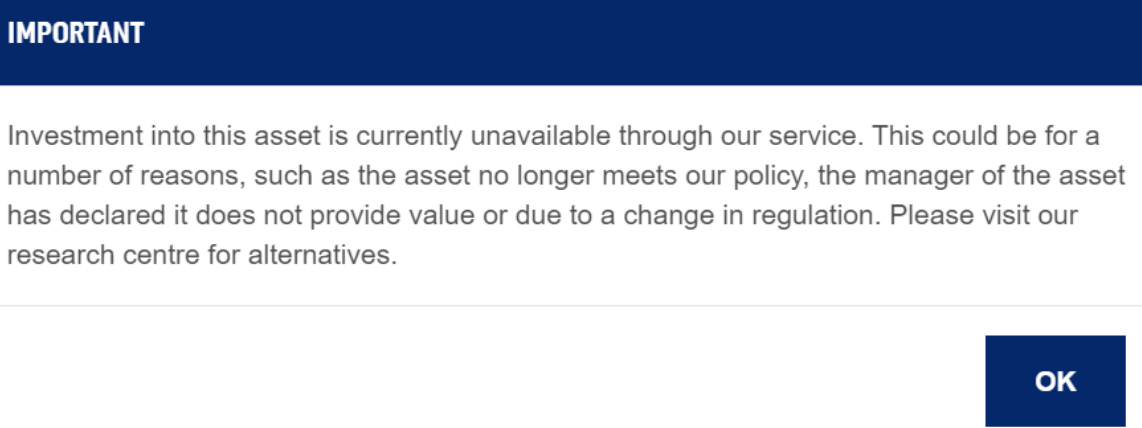

Which instruments each platform allows you to trade and under what circumstances is both highly variable between platforms, inconsistent across time, and hard to predict in advance.

Something you bought yesterday, for example, might not be available to buy today. Likewise, something that was previously not deemed ‘complex’ now is. This changeability can make rebalancing very messy.

Let’s say you own some Blackstone Loan Financing (Ticker: BGLP.L) in your IWeb ISA, and you want to buy some more with the spare cash in there.

Bad luck:

Source: IWeb

Now what do you do? Well, you could sell a different stock in another ISA on another platform and buy back that same stock on IWeb. This way you free up cash in the other ISA to buy more BGLP with – but at the cost of you paying two lots of transaction costs and slippage en-route.

In theory you could transfer the cash from IWeb to the other platform, while sending the other stock across to IWeb (perhaps if you were worried about overall platform exposure). But in practice this takes weeks and can cost money so it is not really an option.

Rule changes can also leave you in a weird situation where you own this stock, but if you sell it, you won’t be allowed to buy it again – creating a random hysteresis function in your rebalancing decisions.

Low no-go

Arbitrary restrictions abound in the weeds on the investment platforms.

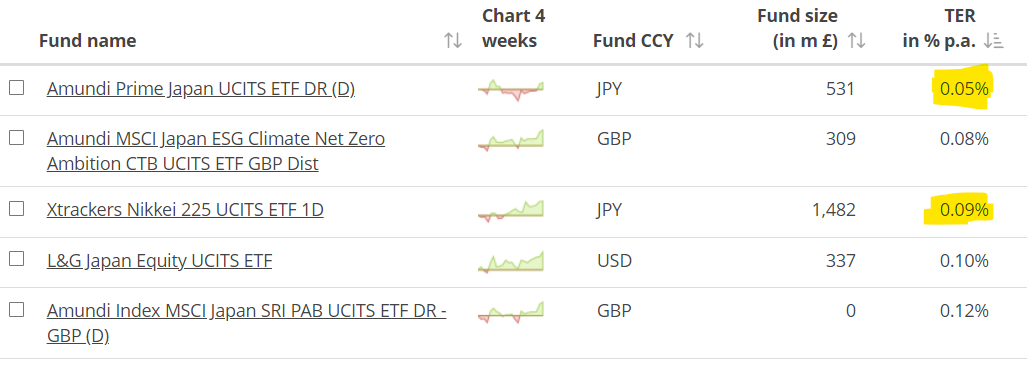

Another common one is to simply not support the lowest cost ETFs in a category.

Want to increase your Japan weighting a little? A fairly normal process would be to go to JustETF, filter by ‘Japan’, sort by TER, and then buy the cheapest one:

Trackers gonna track, so the ETF we want is clearly the cheapest 5bps one from Amundi. Yet most brokers don’t carry it, and if I ask them to add it they won’t.

Hence I end up paying nearly twice as much (9bps) for the Xtrackers’ one.

Call me old-fashioned, but at the very least anyone who holds themselves out as any sort of stockbroker ought to offer dealing in any London listed security, at a bare minimum.

Another difficult area is leveraged ETFs, which many platforms just won’t go near.

And all this is before we even get to the shit show that are the regulations around Packaged Retail and Insurance-based Investment Products (PRIIPs):

Source: AJ Bell

The KIIDs are not alright

In short, PRIIPs is an EU rule that says you can’t buy US-listed ETFs.

We might have left the EU but – completely unsurprisingly – the one single EU rule that was a personal inconvenience to me has not been repealed, and hence most UK investors still can’t buy US listed ETFs.

This is a shame, because for US markets, US-listed ETFs are cheaper, better, more innovative, and (if held in a SIPP) highly tax-efficient.

In theory, if you are a high-net worth or professional investor you can opt out of PRIIPs and then be allowed to buy US-listed ETFs. This is your ‘MiFID status’ in the parlance.

In practice, the only broker that actually enables this is Interactive Brokers. (IG says it does but, in my experience anyway, it doesn’t work, in that it still won’t let you buy US-listed ETFs, at least not in an ISA).

Because the PRIIPs rules require the platform to have a KIIDs on file for every fund you want to buy this can even hobble buying London-listed stuff, if the broker doesn’t have its systems properly sorted.

There’s also some uncertainty as to what counts as a ‘fund’.

AJ Bell and Interactive Investors enable you to buy completely different sets of US-listed Business Development Corporations (BDCS) because they’ve each made completely different decisions about which ones are funds under PRIIPs.

Which seems a bit… random.

Margin lending

Our Family Investment Company’s account is held at Interactive Brokers. The major advantage of which is very competitive margin lending rates:

Since interest is tax-deductible for a FIC, we concentrate most of our leverage there.

The other brokers don’t support leveraged trading, aside from some white-labeled CFD offering perhaps.

IG obviously has CFD / spread betting. But given its high financing spreads, that’s not really an offering that appeals to me.

Flexible ISA

Why don’t more platforms offer flexible ISAs? IG is the only one (on my list) that does.

As a result I end up carrying higher balances with IG than I would otherwise like to, from a platform risk perspective.

Pet peeve #1: Interactive Investor

It’s a small thing, but a special groan for Interactive Investor for not being able to take SIPP platform charges directly from your SIPP, but rather making you pay them separately from your bank account.

Doing so likely increases your effective post-tax platform cost by between 25-67%, because you’re paying fees from outside the SIPP with post-tax money, rather than from inside withpre-tax money.

I’ve complained to the platform several times. Maybe some of you could complain too? It would cost Interactive Investor nothing and it would save us all a few quid from the tax man.

Pet peeve #2: Interactive Brokers

I have a bit of a soft spot for Interactive Brokers. It is great value and I have a SIPP, ISA, General Investment account and the FIC account over there.

The platform stands out for offering MIFID professional status, low FX fees, multi-currency accounts, and being able to trade Options (long-only in the SIPP) and futures (in a general trading account).

However, it is not all sweetness and light.

To start with, Interactive Brokers’ interface is something only a grizzled institutional equities trader from the 1990s could love. Your Nan won’t be using it to buy a few hundred shares of M&S. The learning curve is steep.

The other thing to note – for people who trade UK stocks – is that Interactive Brokers doesn’t have any Retail Service Providers (RSPs).

RSPs are the institutional traders who get you those ‘inside the spread’ and ‘price improvement’ prices that you see with other platforms.

Interactive Brokers basically only offers Direct Market Access (DMA). If you trade UK stocks, particularly mid caps, this may be a problem for you.

My overall view of the investment platforms

Source: Finumus ‘Vibes’, based on personal experience.

Right, let us know what you think in the comments below. And do check out the fine print in the Monevator broker comparison table for more on each platform.

If you enjoyed this, you can follow Finumus on Twitter or read his other articles for Monevator.