A few years ago I wrote about market efficiency and investing edge – and about how you don’t have it.

But let’s dig deeper into why this is true.

You often hear from retail punters and professional investors alike that passive (or index) investing makes markets less efficient.

Their argument is that this inefficiency is what justifies active management.

Well, they’re wrong – but not in the way you might think. The reality is more nuanced.

Let’s do a little maths to explain how passive investing actually makes life harder for active managers, not easier.

Model market: Alice, Bob, and Clifton

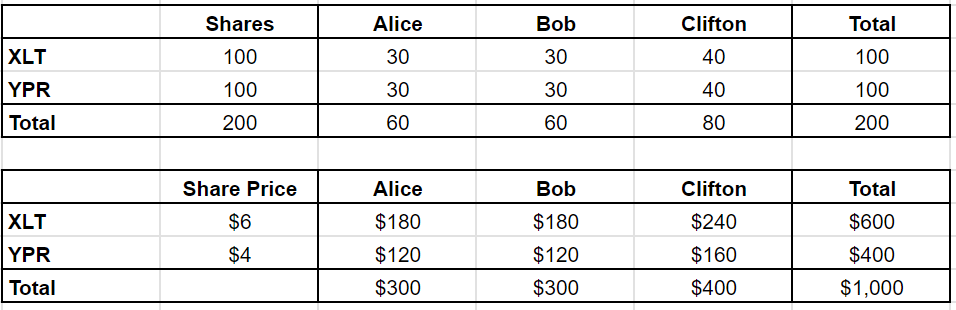

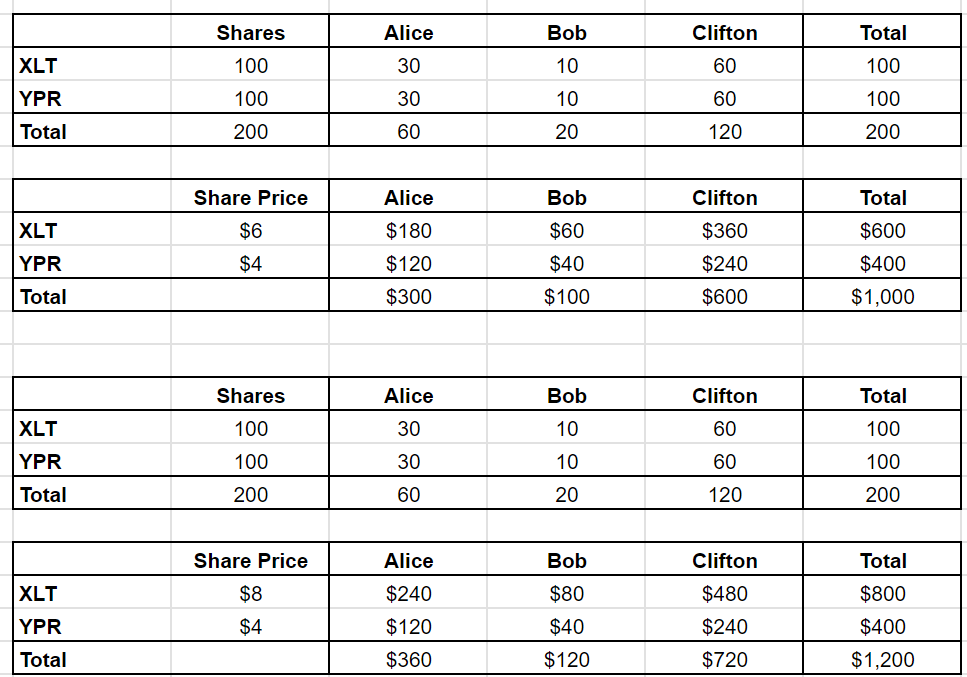

Imagine a market with two stocks, XLT and YPR, and three investors: Alice, Bob, and Clifton.

The total market capitalisation is $1,000.

Between them, Alice, Bob, and Clifton hold portfolios that add up to that $1,000.

There are no other companies and no other investors – we’re keeping things simple – but the ways in which this model is ‘wrong’ are not really material to the point today.

Alice and Bob each hold $300, while Clifton has $400.

XLT and YPR each have 100 shares outstanding, with XLT priced at $6 per share and YPR at $4.

(Yes, this is starting to sound like GCSE maths, but stay with me.)

In other words:

Now, Alice, Bob, and Clifton all hold market weight portfolios. This makes them passive investors by default.

Ideologically though, Clifton is your classic index fund investor – passive through and through.

Alice and Bob, on the other hand, are active traders. They are willing to take a punt if they sense an edge.

So this market is 40% passive (Clifton) and 60% active (Alice and Bob).

Dumb passive money?

One common misconception is that passive investors blindly ‘buy expensive stocks’ when prices rise.

Let’s expose this myth with an example.

XLT releases stellar results before the market open, and Alice decides she’s bullish. She calls Bob to buy some of his XLT stock, knowing that Clifton – the passive guy – basically does not trade. (Clifton doesn’t even bother going to the office till after lunch!)

Here’s how their conversation goes:

Ring, ring…

- Alice: “Hey Bob, I’m in the market for XLT. What are you offering?”

- Bob: “Hmm, I saw their results. Strong stuff. I’d have to start with an 8…”

- Alice: “I was thinking more like $7.95.”

- Bob: “LOL, nope. I’d buy from you at that price. $8.05 – final offer.”

- Alice: “I’ll leave my bid on Quotron. Call me if you change your mind.”

- Bob: “Catch you later.”

When Clifton finally gets into the office – sometime after his tennis match and a long lunch at the club – he logs onto his Quotron and sees that XLT has jumped 33% to $8.00.

A news headline reports: XLT Surges on Blowout Results – Light Volume.

Pleased with his morning’s ‘work’, Clifton updates his portfolio to reflect the new prices.

So note that nobody did any trading at all here. Alice and Bob just sort of agreed that $8 was a reasonable price for XLT, and so, by proxy, did Clifton.

This is how most price moves in the stock market happen. You don’t need trading to move prices.

The alpha chase

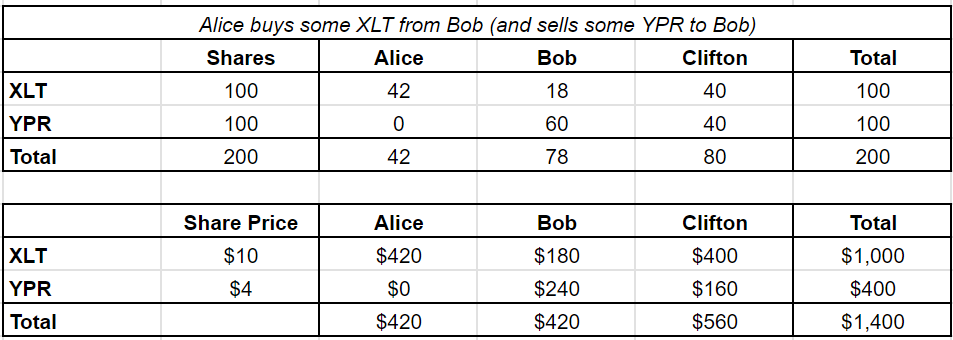

Fast-forward a few weeks, and Alice gets some inside info on XLT – let’s say from a friendly round of golf with its CEO. The company is about to secure a major government contract.

Alice tries again to buy from Bob, who smells something fishy. He agrees to sell her some XLT shares – but at an even higher price, $10 per share.

Since this is a closed system, Alice needs to sell YPR to raise the cash to buy XLT. And guess who she has to sell it to? Bob. They agree to swap their stakes.

Alice is now all-in on XLT, while Bob holds more YPR. (For convenience we’re ignoring that Bob would probably demand a discount on the YPR he’s buying, as well as a premium on the XLT he’s selling – Alice’s ‘market impact’).

Here’s a status check:

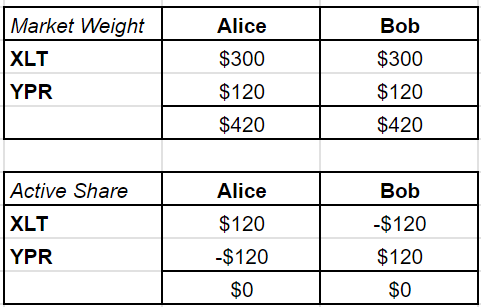

And here’s the kicker: for Alice to overweight XLT, Bob must underweight it. Clifton, as the passive investor, doesn’t change his positions at all.

This is a zero-sum game. Every dollar of ‘active share’ that Alice holds has to be offset by Bob’s:

None of this has changed their relative portfolio values – but it will.

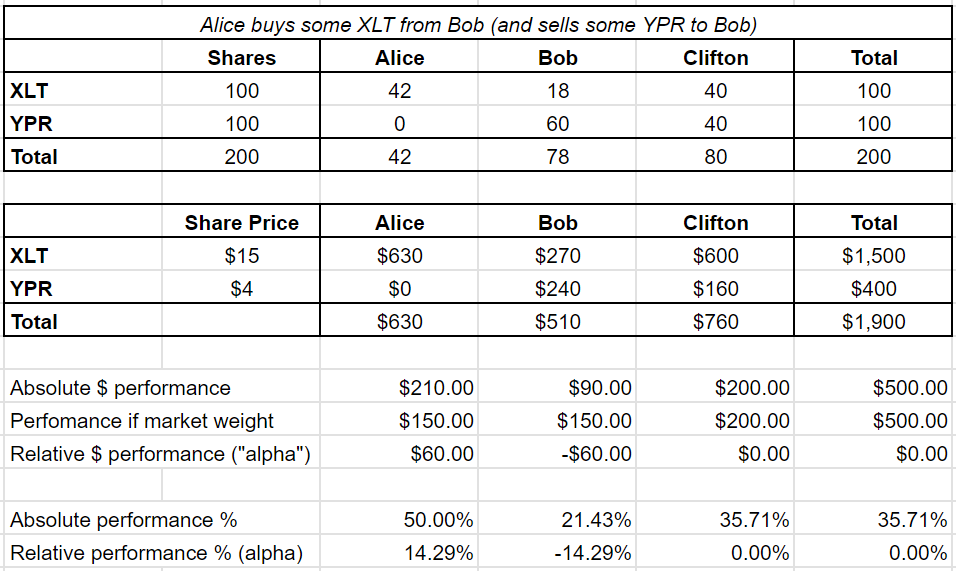

When XLT surges 50% on news of the contract, Alice makes a $60 profit.

But Bob? His loss is the exact mirror of Alice’s gain:

Since anyone can just buy the market, what matters for active investors is outperformance.

Alice’s outperformance (aka alpha or profit) of $60 is exactly offset by Bob’s underperformance of $60.

Bob still made money. Just less money than he would if he’d stayed market weight.

I know I keep making the same point, but it’s important: Alice can only make her $60 alpha at the expense of Bob.

The winner needs the loser. 1

Increasing passive share

Now let’s imagine that Clifton, our passive investor, controls more of the market than before.

Let’s say the market has shifted so Clifton now runs $600 of the total $1,000.

Meanwhile Bob only has $100 to manage while Alice’s capital stays the same at $300.

The passive share of the market has grown from 40% to 60%. Let’s re-run that first conversation between Alice and Bob that bumped up the price of XLT to $8, to see where it gets us.

Ring, ring…

So far, nothing changes. However when Alice returns from golf with XLT’s CEO and tries to buy more shares, things get trickier.

Bob doesn’t have enough shares to sell her all that she wants. Now Bob only has ten shares of XLT, priced at $10 each, for a total of $100.

Alice has $120 worth of YPR to sell, but she can’t buy as much XLT as she would have liked:

As passive investors like Clifton take up more market share, Alice’s strategy runs into a brick wall. She can’t go all-in on her insider tip because there aren’t enough active participants to trade with.

And that’s a major problem for her alpha.

In fact let’s check what it’s done to everyone’s alpha compared to our previous example of 40% passive market share:

It’s got worse for everyone except Clifton!

- Alice’s alpha has reduced.

- Bob’s negative alpha, in proportion to his capital, is now even worse.

- Clifton doesn’t care either way.

The passive doom loop

Let’s imagine that Alice keeps getting lucky – or inside information – and Bob consistently underperforms.

Eventually, some of Bob’s investors will redeem their money. Diehard believers in the quest for outperformance, they would like to hand it to Alice – but they can’t.

Why not? Because Alice’s strategy is capacity-constrained.

Alice can only make money if she can trade against someone else, like Bob. But if Bob’s investors leave him and put their money into Alice’s fund, she’ll have fewer people to trade with – meaning she can’t deploy the capital effectively.

Bob’s redemptions have to flow to Clifton.

And so passive money grows, and active managers like Alice and Bob have ever fewer opportunities to beat the market. As passive share increases, active management becomes harder and harder.

It does not matter how good Alice’s inside information is. Her ability to monetise her edge is limited by the supply of suckers she can trade against.

This is where the so-called doom loop comes in.

As passive investing grows, active investing gets tougher, which drives more money to passive funds, which makes life even harder for active managers… and so on, in a vicious cycle.

Who’s Alice?

So, how do you spot a bad hedge fund?

Easy. They’re the ones willing to take your money.

The true hedge fund giants – names like RenTech, Citadel, and Millennium – won’t even let you invest.

Why? Because their alpha is capacity constrained.

These guys often can’t even compound their own money.

If you’re an investor with RenTech – which means you’d have to work there – it cuts you a cheque for the profits every quarter. You don’t get to leave the money in there compounding for the long-term.

Such funds have already soaked up all the market inefficiencies their strategy has unearthed.

They can’t let just anyone in – in fact they need suckers on the other side of their trades, so why not you.

Don’t be Bob

Finally – who is Bob?

Bob is anyone willing to underperform for long periods without having the money taken away.

For years, this was the underperforming active mutual fund manager.

Now? Increasingly, it’s retail investors.

Why do you think hedge funds, prop shops, and market makers will pay brokers to trade against their retail order flow?

*Cough* *cough* – I mean, provide ‘price improvement’ services!

Don’t be Bob.

Follow Finumus on Twitter and read his other articles for Monevator.

- Incidentally I hope our model market makes it obvious, if it wasn’t already, that Alice’s insider trading is not a ‘victimless crime’. She is taking money directly from Bob.[↩]

I love this thought experiment. I had wondered why the majority of hedge funds were supposedly making losses (beyond that of active managers).

@Bob — You’re taking your losses very well, have a chat with Clifton 😉

In my electronics engineering career feedback systems with varying delays tended towards instability, particularly when combined with nonlinear feedback elements. I am sure that AI will be brought to bear on this, which will be successful, most of the time…

Expect some serious humdingers of market crashes, as the invisible hand gets increasingly weighed down and limited in action. And a good few ‘it’s all different now’ periods of, what was it called, ‘irrational exuberance’

Be careful what you wish for and all that…

Slight complication:

Most quoted companies can issue more equity for cash / hold sharws in treasury and sell them / buy them in, for cash.

So there is scope – a lot of scope – for large corporates to take the other end of the active trades.

Not sure how much difference this makes but i suspect it alters the “fixed pool of investments” assumption. A winning business can sell shares at an inflated value for cash and/or buy them in a dip (the latter possibly funded by borrowing from the bank…)

Very interesting thought experiment nonetheless!

Is this the financial Groucho Marxian: “I wouldn’t want to invest in any hedge fund that would have me as an investor”?

“… feedback systems with varying delays tended towards instability”: many of us probably learned that in the showers at school.

The effect was even more striking when you went from one shower operating to several. Once twenty-two or thirty showers were operating it became less of a problem (or so my memory says). Is there a theorem that speaks to that?

Superb. Thanks for this.

Thanks for this, makes a lot of sense.

I’m periodically tempted to dabble in active-investing and articles like these help replenish the supply of willpower that stops me from doing so!

But what if the XLT rise was a bubble?

i.e. Sensible passive C enjoys an effortless temporary wealth rise

[oh, and during the bubble summer, desperate careful Passive MOI

buys half of C’s shares; C has a nice summer cruise; MOI is staking his

retirement on this]

The bubble pops: A is wiped out, B won because YLT takes XLT’s business and the whole market is valued back at $1000, C had his fancy cruise and a nice ride and he carries on, and MOI? hasn’t MOI’s passive retirement just evaporated?

@Meany — Passive investors returns will indeed rise and fall with the market, bubbles and all.

The first question facing investors is what do you do about it?

Unless you have edge (and Finumus argues most people don’t and I agree) you’ll be unable to pick funds or stocks that beat the market, except through luck — and you’ll pay higher fees than a passive investor for trying.

Hence on average ‘you’ (strictly speaking we should take about money) will do worse than if you’d stuck with index trackers.

The other question is whether passive investing flows inflates overall valuations. There’s been some fresh research in this direction recently suggesting ‘yes, a bit, maybe’.

But again there’s not much you can do about it unless you have edge, and you probably don’t, except invest more of your marginal money elsewhere I guess (your home, your qualifications, you buy-to-let, cash, etc) — however saying you know valuations better than the market (market timing) is itself a claim for having edge… 😉

For ease of reference, the relevant MV comments on, and the links to, that recent research (on the Inelastic Markets Hypothesis, proposed by Xavier Gabaix and Ralph Koijenand) referenced by @TI #10 above are reproduced below, alongside the links to its discussion by its populariser (Michael Green).

I’d be interested to know @Finumus’ views.

It seems to me the shrinking pool of alpha issue that@Finumus so clearly explains with his excellent example above is one of the 4 pillars supporting passive alongside each of the other 3 of:

1. Cost advantage (least important but still useful),

2. Non-ergodicity, in that the equity return skew profile (as researched by Bessembinder) means that the weighted average of active portfolios represented by the index performs substantially better than both the median and modal active portfolio, whether of a professional active manager or of an amateur active investor.

3). Increasingly inelastic markets increasingly favour passive over active (in particular, less liquidity per unit of market cap for the mega caps means that they get bid up more proportionate to their cap weight by net positive fund flows, and price insensitive passive flows don’t self correct for this).

NB: IMO this (the IMH) is a virtuous self reinforcing feature, and not a bug, for passive. Of course, beyond a certain point, as the effects are convex at extreme passive share (not the current 50% for the most heavily indexed equities – the S&P 500 – but 80% plus), this could, eventually, have negatives, but we’re way off that level of passive concentration for now.

Here are the previous comments and links relevant to this:

https://monevator.com/weekend-reading-we-all-feel-the-pain-of-active-fund-managers-now/

#16 and 37

https://monevator.com/weekend-reading-oh-what-can-ail-thee-knight-at-arms/

#15 to 19 and 21 and 22, 24 and 32 and 33

https://monevator.com/weekend-reading-fama-and-fortune/

#3, 6, 9 and 48

https://monevator.com/weekend-reading-lets-have-a-meeting-to-talk-about-time-wasting-meetings/

#17, 18 and 31

https://monevator.com/weekend-reading-common-sense-for-crazy-times/

#37, 41, 43 and 47

https://monevator.com/weekend-reading-the-city-that-never-sleeps-mulls-midnight-share-trading/

#19 to 21

https://monevator.com/weekend-reading-looking-for-gain-from-the-cgt-pain/

#7 and 8

https://monevator.com/weekend-reading-the-trading-game/

#10

https://monevator.com/weekend-reading-not-going-out/

#17 and 31

Papers

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3686935

Substack – Green

https://open.substack.com/pub/michaelwgreen/p/trying-to-be-better-again

https://open.substack.com/pub/michaelwgreen/p/why-bother-being-better

https://www.yesigiveafig.com/p/be-better

Substack – Klement

https://open.substack.com/pub/klementoninvesting/p/the-butterfly-effect-index-funds

Interviews – Green

https://www.bloomberg.com/news/audio/2024-08-15/masters-in-business-mike-greene-podcast

https://rationalreminder.ca/podcast/302

https://youtu.be/N_-oRE4bDUc?feature=shared

Bogleheads

https://www.bogleheads.org/forum/viewtopic.php?f=10&t=430546&newpost=7844074

Substack – Other

https://davenadig.substack.com/p/why-the-activepassive-debate-matters

This is such a good explanation.

Only quibble – the guys who provide liquidity to retail actually are typically not your fundamental long term active guys, they’re generally high frequency trading firms – and they’re actually providing incredibly good fills (I used to be a very happy Schwab customer when I lived in the states…) which are much better than retail could achieve on screen.

The reason they pay for the order flow is that even after providing substantial price improvement the flow is (on average) uninformed enough that they can recycle it for a profit.

While this is technically true, it’s an overly simplified model. The real world has a couple of features that create ‘natural losers’.

The many non- economic market participants. Examples include companies managing their balance sheets, governments owning strategic stakes, passive investors tracking benchmarks (huge amount of flows in and out of shares that get added or removed to indices), companies pursuing buyback policies, and employees disposing of stock based compensation.

My issue with ‘passive’ investing is that for the two biggest US indexes it isn’t passive. Because the two indexes have now become so heavily skewed to 7 companies:

E.g.

For every £100 a ‘passive’ investor invests into an S&P500 tracker £7 goes towards buying the shares of 1 company..

Are you (mr passive investor) ‘really’ that enthusiastic for the fortunes of 1 company that you’d invest 7% of your ‘passive’ funds into it at its all-time highs?

A decision to invest ‘passively’ – in other words to make no decision on any particular company – has become an active decision to invest 7% of your investment pot into one company :))). That isn’t ‘passive investing’ by the commonsense understanding of the term.

It might be mathematically passive or whatever. Worth considering.. and what that sort of lopsided weighting usually leads to. Might be ‘passively’ tracking the index but if an index of 500 of the most valuable US companies is so massively lopsided that 7% of its total value is weighted to just 1 company (and 18% of its total value weighted to just 7 companies) then the index itself might not be a good representation of what ‘passive investing’ is commonly understand to mean.

Enjoyed this, and something I’ve also written about.

Just one comment.

“So, how do you spot a bad hedge fund?

Easy. They’re the ones willing to take your money.”

There are occasional edge cases where a hedge firm with an edge is still scaling and hasn’t reached capacity. The investors are generally unhappy when capacity is reached, and their money is handed back.

@Rambo – Yes, kind of, most indexes ignore shares held in treasury, of course they can issue shares – but not get all Modigliani and Miller on you – what difference does that make? You’ve just swapped all market participants spare cash for cash on the balance sheet of the companies they are invested in. If you “look-through” to the companies balance sheet as well – it’s a wash.

@Meany – Yeah – this is essentially an argument that markets are micro-efficient, not that they are macro-efficient. i.e. You can’t beat “the market” – and therefore you shouldn’t bother with giving your money to active managers (or, at the extreme, hedge funds). As to if you should invest in equities at all? This is kind of a different question.

@DeltaHedge – I agree with pretty much all of your 4 pillars.

@Paul – indeed – liquidity providers to retail aren’t your proper “active investors” – I kind of meant this as a joke.

@Datosaurous – Yes, I originally had a longer section about the stories people tell about who the active losers are – but – I’d argue that these are actually pretty small. Stocks getting added / deleted – Vanguard VTI has an annual turnover of about 2% of it’s AUM – that’s not much alpha.

@petejh – Of course, you’re correct – the S&P500 isn’t a passive index at all – it’s actually an active portfolio chosen by the index committee. But, it doesn’t have that much tracking error to a “whole market” – VTI is up 88% and SPY up 93% over 5 years (and other 5 year periods it will be the other way round).

@petejh,”It might be mathematically passive or whatever. Worth considering.. and what that sort of lopsided weighting usually leads to. Might be ‘passively’ tracking the index but if an index of 500 of the most valuable US companies is so massively lopsided that 7% of its total value is weighted to just 1 company (and 18% of its total value weighted to just 7 companies) then the index itself might not be a good representation of what ‘passive investing’ is commonly understand to mean.”

My definition of passive investing and the one used by Finimus in the article is to invest in a market by market weight to achieve market returns. Trouble is the term has become corrupted and now means different things to different people. Some people extend the definition in all sorts of strange directions, none of which has anything to do with the basic “invest to achieve market returns”. If that means overweighting a few giant companies, then so be it. If you don’t do that then you are at risk of not achieving the market return.

What do you mean by “the index itself might not be a good representation of what ‘passive investing’ is commonly understand to mean.”? If not market cap weighted, what does it mean?

Just for clarity, when I said “overweighting a few giant companies”, what I meant was overweighting in monetary terms, not overweighting in market terms. A passive stockmarket investor should invest precisely by market cap, so overweighting in monetary terms inevitably follows from that.