Good reads from around the Web.

Are you a prudent saver who regularly runs the numbers on your potential post-retirement income?

Or are you a Scrooge McDuck who has fallen in love with money for its own sake?

The title of a John Authors’ article in the FT this week – Is Greed Good? No, It’s Seriously Bad For Your Health [Search result] – implies that this isn’t an academic question.

Authors even cites research suggesting it’s not just your physical health that could suffer from an excessive love of money, but also your financial health.

He writes:

Psychologists now have a clear definition for love of money. It is not about any instrumental need for money to fulfill our other goals, which all of us have, but rather about a love or need of money for its own sake.

Using the Money Ethic Scale developed by Thomas Li-Ping Tang in 1992, State Street developed an Investor Love of Money Scale (ILOMS).

Researchers asked interviewees in 20 countries a series of questions designed to find out how important money was to their self-esteem.

They also tested how they would respond in a series of financial situations.

For example, they would ask if money was a symbol of success, if they talked about it a lot, or if they wanted to be rich.

The results were clear. The more someone had an emotional attachment to money, the more likely they were to make mistakes with money.

A series of behavioural biases that lead investors into predictable mistakes have been diagnosed over the years. Avarice exacerbates all those biases.

The article goes on to list investing vices, from over-trading to buying high and selling low.

Being in love with money could be counter-productive, in other words, even for intentional money-grabbers.

Money, money, money

It’s a nice morality tale and life is more complicated, but I do agree that concentrating on wealth can at least change you as a person.

I’ve seen a bit of that in myself.

When you first start saving and investing, the idea that you’re in love with money feels fanciful.

Unless you inherited the family pile – literally – you start with nothing (or these days likely less than nothing, after student loans).

You’re just trying to be sensible, at a time when money is scarce, too.

However as the years go by, your wealth grows and snowballs. At some point it becomes so much that when you’re adding the sums up you’re looking at quite a wodge.

And you wonder.

Of course, you probably rationalize this wodge away – as I believe you should. It’s for financial freedom or to keep the lights on in retirement. Your friends might not nurture their nest eggs to the same degree, but they face the same challenges and have likely stashed some of their cash, too.

Being conscious of these challenges and actively trying to confront them doesn’t seem like the same thing as being in love with money to me. The FT quote I highlighted above agrees.

Then again, I know that in my 20s I seriously didn’t care much about money.

I saved it because I am by nature a saver.

But I earned a relative pittance compared to my university peers and I rarely thought about it.

I considered gambling away ALL my life savings in a business venture in my-mid-20s – and I did put about half of them into one in my early 30s.

I can’t imagine taken such proportionate risks with my wealth barely a decade later. Have I fallen in love with money?

I don’t think so. Rather, I know I’ve gotten older and I believe there’s less time left to make good.

That said, unlike most Monevator readers I have probably fallen in love with active investing and with keeping score.

But what about you? Is money for you a means to an end, a fling, a passion – or the only thing left that can really still do it for you?

From the blogs

Making good use of the things that we find…

Passive investing

- How to survive a market melt-up – A Wealth of Common Sense

- Asset management fees are a stealth tax – The Evidence-based Investor

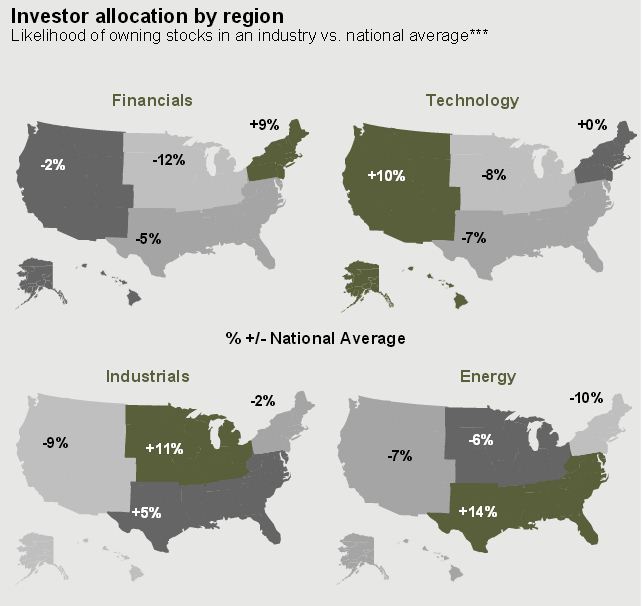

- Forget home bias, what about region bias? [Image] – JP Morgan

Active investing

- Why consumer staples are the new dotcoms – The Value Perspective

- Investors perilously wait for Goldilocks market – Investing Caffeine

- IG Group still looks cheap – UK Value Investor

- Late summer, late cycle – MFS

- The causes and consequences of cash burn – Musings on Markets

The great de-retirement debate: A follow-up

- Where can we live but days? – SexHealthMoneyDeath

- Burnout, baby, burnout – Simple Living in Suffolk

- FIRE is… – The FIREStarter

Other articles

- Selecting your DIY pension platform – DIY Investor (UK)

- What is a safe pension withdrawal rate? – Schroders

- Naive, a victim, or just plain irresponsible? – Retirement Investing Today

- Can today’s electric vehicles make a dent in climate change? – MIT

- Retire early with kids? You’re kidding, right? – Simple Living in Suffolk

- Introverts get “hangovers” from too much socializing – Kottke

- What’s wrong with America? [Tweetstorm] – Chris Arnade

Product of the week: Nothing good lasts forever, as I often told my exes. And that’s triply true of bank accounts, as demonstrated most recently by Santander slashing the 3% cash geyser on its 123 account down to a puny 1.5%, as reported by ThisIsMoney. Seriously, never put your happiness in the hands of anything or anyone. Except, possibly, puppies and kittens. And remember that higher-interest paying P2P alternatives like Zopa and RateSetter come with extra risks.

Mainstream media money

Some links are Google search results – in PC/desktop view these enable you to click through to read the piece without being a paid subscriber of that site. 1

Passive investing

- Interview with Charles Ellis about index funds [Video] – WealthTrack

- This anonymous index fund manager oversees $800bn – Bloomberg

- Fund charges fall in Europe as investors demand value [Search result] – FT

Active investing

- Investment: Rise of the DIY algo traders [Search result] – FT

- The price of oil is back from the dead – Telegraph

- Swedroe: Who trades on momentum? – Mutual Funds

- Is it too late to invest in gold? – ThisIsMoney

- Some US shares the ‘ultimate stock pickers’ picked – Morningstar

A word from a broker

- The economic verdict on Brexit so far – Guardian/Hargreaves Lansdown

- A quick look at high yield bonds – TD Direct Investing

Other stuff worth reading

- Like me, comedian David Mitchell is all for inheritance tax – Guardian

- Poor little rich kid! On inheriting wealth [Search result] – FT

- Is AirBnB income really worth the hassle? [Reader debate] – Guardian

- You can’t withdraw 4% from your pension and expect it to last – Telegraph

- Big banks already getting ready to bail on Brexit Britain… – Bloomberg

- …but High Street sales figures defy the Brexit doom – ThisIsMoney

- …while regional housing market health depends how it voted – ThisIsMoney

- How one couple saved $1m in four years to retire at 43 – CNBC

- Why can’t we see we’re living in a golden age? – The Spectator

- The State pension top-up nobody seems to want – Guardian

- London finds Brexit hard to stomach – Reuters

- In defence of the adult nap – NY Mag

Book of the week: Have you been enjoying Billions? (I’m thinking of the TV drama on Sky, not your net wealth). Do you have the ‘Edge’ that eludes so many? Do you want to start a hedge fund? Then why not read How To Start a Hedge Fund? It is well-endorsed and has decent reviews, but beware it is focused on the US – the UK path is unfortunately more complex.

Like these links? Subscribe to get them every week!

- Note some articles can only be accessed through the search results if you’re using PC/desktop view (from mobile/tablet view they bring up the firewall/subscription page). To circumvent, switch your mobile browser to use the desktop view. On Chrome for Android: press the menu button followed by “Request Desktop Site”.[↩]

{kind=link}

Comments on this entry are closed.

TI

On the subject of whether we should be more selfish, I’m always amazed at how much work you put into compiling this every week. Thank you!

TEA

Interesting article about an analysis of loan underwriting standards on a leading US peer to peer lending platform. Principal-agent problems all over again

http://www.bloomberg.com/news/features/2016-08-18/how-lending-club-s-biggest-fanboy-uncovered-shady-loans

An interesting challenge you pose to us. To what extent do we believe we are in love with money?

I think it is hard to self-diagnose. One person’s saving and investing for purely instrumental purposes is another person’s love of money for its own sake. Can we really understand our own motivations?

My family was relatively poor. My father was a serially unsuccessful business man. He really was very bad at it, and went bankrupt twice. I learnt a lot about how not to handle money and business by watching my father. I watched the corrosive effect of that on my parents’ marriage and our family life. As a result I craved certainty in my youth and swore never to start my own business and to always seek secure employment (I did not know then that there is no such thing as secure employment!).

So it went through several career changes with big employers whilst I raised a family, bought a house and built a pension. All conventional, and with little savings outside pension as it felt like there was little to spare. We were not extravagant people, but young children coincided with mortgage rates peaking at 15% (or whatever it was – I seemed to have blocked the memory and it is now firmly locked behind a solid door in a dark cellar of my mind).

Eventually the usual merry go round of corporate reorganisation left me without an interesting job, and I finally summoned the courage in my late 40’s to strike out independently. Something I had sworn a mighty oath on leaving home never to do. Possibly the hardest personal decision I ever made in my life (yes the job had become psychologically shitty, but the salary, the pension!). My partner and family were immensely relaxed about the whole thing – “she’ll be right!”. Something I found as scary as my own concerns as to whether I had bought a one way ticket to the workhouse.

Fortunately things went well (lucky again!) and I started investing once I had paid down debts of starting up and paid off the mortgage, because I was now responsible for my own pension.

Now I have gone through another period of employment because the work was interesting, and am approaching some form of early retirement.

I know in my head that I have enough pension and money to cope with just about anything that could realistically be thrown at me. I know this in my head, but in my stomach I am scared. Really scared that I am in some way going to run out. My partner looks at the numbers with me, stares at me, shakes her head and says “what are you worrying about? Enjoy life!”. She is right and yet I worry.

Those early miserable days with the stress and anguish of not enough money are part of what formed me. It meant I left it late to try and develop something on my own, it meant I felt the weight of providing for my family more than was necessary, and it meant that I cannot feel comfortable that I have enough resources for retirement. Even though retirement probably means some new kind of economic activity and not lotus eating.

Am I in love with money? I don’t know. I am probably trying to accumulate more than I require to live the lifestyle we desire. We are neither of us big spenders, and the kids will probably be happy with the inheritance, but why can’t I do the sums and congratulate myself on reaching FI?

Somewhere between being rational about what you want and how hard you will strive to get it, and a ‘pathological’ desire to accumulate with no purpose in mind because it makes you a ‘success’, is the accumulation of money because you are just damned scared about the future.

The grandmother of a friend when I was young was a delightful lady who was pretty wealthy. The only problem was she was extremely close with her money and apt to become loud and aggressive at any suggestion she could make her life easier by spending some of her wealth (no dishwasher for her!). Why? She had come to the UK as a refugee from Austria at the outbreak of WWII.

Our attitudes to money are shaped by our history and experiences, and however much we rationalise and explain our decisions, there are some pretty deep-seated ideas driving us.

So am I obsessed with money? I am afraid you are going to have to ask someone else. I cannot be objective.

@ Old Eyes – you seem very self aware of where your money drives come from, which I think is the best way of controlling them rather than being controlled. We’ve all been conditioned with our own attitude towards money as much as sex, status etc. The danger is not being conscious of it.

Enjoyed this article about defensive pessimism which I hadn’t heard of before:

http://tonyisola.com/2016/08/the-positive-power-of-negative-investor-thinking/

Made me realise that my propensity to worry isn’t so daft afterall. Especially comforting after writing a comment elsewhere which made me realise that I was worried about not reaching FI, not triggering FI once I’d accumulated ‘enough’ and then not enjoying FI once I’d triggered it. What a basketcase / brilliant defensive pessimist.

@ Anyone who cares – that Telegraph piece about the 4% rule is total BS. It’s sloppy it does more harm than good. Who ever said withdrawing 4% might not eat into your capital. If you don’t want to eat into capital then don’t spend more than your income.

“enough pension and money to cope with just about anything that could realistically be thrown at me”: “realistically” – there’s the rub. Was the Wall St crash realistic? WWI? The Great Depression? The Weimar inflation? The Bolshevik coup? The Japanese invasions of half the Orient?

I look at such a list and infer that having some of our money abroad would be a good idea. But I haven’t the faintest idea how to arrange that.

Great article about Vanguard fund manager Gerry O’Reilly and how the company works. Thanks for the link!

The Telegraph 4% piece seems to mix up two completely different ideas: aiming to maximise spending without hitting zero before death, and aiming to preserve the capital so any offspring (soon retiring themselves!) can inherit it. Any discussion of SWR really needs to define what that is, unambiguously, and avoid terms like “deplete” which can be read both ways.

@TA Thanks for the link. The power of ‘moderate pessimism’ is much under-rated. When I was involved in new product development and launches one of the things we would do is war-game how our competitors could atta ck our product. A vital way of not being consumed by our own advertising and PR. In a strange way moderate pessimism helps the less confident take greater risks. It gives us a worst case that is probably not as bad as we feared.

@dearieme – spot on. A global economic or environmental collapse, a decade or more of double digit inflation, expropriation of assets, any number of things would destroy my plans. But for these extreme events there is probably no amount of money that would protect me.

Perhaps my fears are a bit more under control than I think. If I would need four, five, ten times as much wealth as I have now to be secure; well there is nothing practical I can do about it at this stage. The idiocy of my thinking is worrying that 5% more than I have would make all the difference. So I don’t fret about financial meltdown, but I do about a marginal difference in my circumstances. How dumb is that!

Yes, the Telegraph article is a bit confused, which was why I separately extracted the Schroders’ piece it references up top. I thought the graph was worth a second though, and the fact that debating 4% had gone mainstream, especially after all the recent discussions here. 🙂

@TEA — Cheers!

“Money doesn’t make you happy. I now have $50 million but I was just as happy when I had $48 million.” Arnold Schwarzenegger

Money doesn’t make you happy but it does buy a better class of misery.

Personally, I’d say that I’m not in love with money itself but I am in love with what it represents to me: freedom.

The FT’s “Rise of the DIY algo traders” is fascinating. Anyone here dabbled with it? Numerai looks like a pure machine learning problem due to the obfuscated data, but the other platforms mentioned seem accessible to financial types.

Enjoyed the Spectator golden age article , reminded me of Han’s Rosling https://www.youtube.com/watch?v=jbkSRLYSojo

@TI, your decision to live off capital despite inheritance being a non-issue smells like you have strong feelings for money to me.

I too worry that i will struggle to see my net wealth diminish. Like everyone else i don’t want to admit i love money though. My Facebook status is “it’s complicated”.

Lots of the extreme frugal FIRE bloggers view money as a way of keeping score, all the ones posting the minutiae of their monthly finances at savings fractions. It is all to easy for that to become a game, where the balance sheet is all, and bragging rights for how rough their hair shirt is, all the sacrifices they are making. For comparison with others they have to use a common reference frame, and money is that, so they love the numbers rising.

http://www.psyfitec.com/ is worth a read on the psychology of money

Blimey, what a difficult one. My parents taught me respect for money as they both left school at age 14 and had to work hard for everything. As a result, I took on 30 hour a week jobs from age 13 (fit around school) to earn enough to buy myself a bicycle, calculator and home computer (this latter one n 1979).

Fortunately (or otherwise!) my precociousness with electronics and computers meant I was earning more than my teachers at school (and let them know it), more than my lecturers at university (ditto), and in my 1st post university year, probably earned more than them all put together.

This gives you a certain swagger at age 21 and early lessons went out of the window. Let’ just say that 12-18 months later, all the money had gone. It took a while to get back on an even keel but the product we created to achieve this is still talked about to this day. Lot’s of pride but not quite as much money as before. Oh well. Things picked up from there on, but never quite matched the early days.

I’m now a “stockpiler” of money because I know how easy it is to blow it. I also know that earning huge sums in the here and now is no guarantee that it will continue.

@Gregory… Took the words right out of my mouth, there’s no ‘real’ answer to “How much is enough/ how much is too much?”, But money, like everything, is subject to the law of diminishing returns…

…much like my first pint on a Friday is enjoyed far more than the sixth, being able to holiday twice a year rather than one probably brings far more joy than a third one would over a second…

I have always seen money as a means to solving life’s problems. There has never been enough when problems were at their greatest. Mortgage, kids, university, weddings, grandchildren.

So it seems to me whatever makes you happy and is achievable is a good decision.

Thanks for the links, TI.

The 4% debate rages on — and hopefully readers of these pages will be alert to all the pitfalls that lurk in the reporting — is these UK investments only, or a globally diversified portfolio? Is the withdrawal rate inflation-linked? Is it a sharp number or actually a probabilistic forecast (what chance of running out in 30 years?). Should it be 30 years or much much longer? Can the glide path be tweaked — spend less, earn some more? Troubling for the serious student, and possibly too much for the average broadsheet article. Like all things in FI planning — I think you need to stick something to get going and plan around it, knowing that you will be wrong-ish. Perfect portfolio? Get one you stick with. Predictive withdrawal rate? Choose one and see how it goes. There are many more important things than trying to have just one penny left on your death-bed (pace IHT advocates).

I also enjoyed the FT’s algo-trading article. I know Dan pretty well and he’s a smart and successful guy, but he doesn’t know what the market is going to do any more than I do. He knows full well that the route to success is unlikely to be his algorithm, but managing his business well. Ultimately it’s a haven for amateur chartism and some sort of belief in the wisdom of crowds. Which — let’s face it – is what passive investing is too. Focus on the costs and take all the beta you can eat.

@acorns it’s not the number of holidays, it’s the length of them. I look forward longingly to two two month holidays a year instead of two two week holidays. So much of a holiday is overhead: booking effort, to/from airport, time travelling, flights, paraphanelia, it can actually be very cheap for the time you are ‘there’ once you’ve found affordable accommodation.

…or just make your non-holiday life so pleasant that you don’t need to take a holiday from it.

I have no love of money but I have a huge fear of being without it.

It started when we had children six years ago. Prior to that I couldn’t even have told you my net wealth and I didn’t manage it in any way at all; it just accumulated from my earnings and bonuses. When I did calculate my net wealth, a seven figure sum, I was initially rather pleased with myself. That feeling didn’t last long. I looked at our expenditure and realized that adding 2 children had tripled it. I projected the cashflows needed for schools/university, buying them houses (or giving them deposits) etc. It doesn’t help that I have a pessimistic long-term view on asset returns (I see the majority of market gains in recent years as nothing more than discounting effects from lower long-term risk free yields; upfront capital gains now at the expense of lower income later). That’s when the fear really kicked in.

When I was only looking after myself, it’s seemed much easier to take financial risks but when you have children then your failure becomes their failure and that responsibility can be crushing. It’s made me far more risk-averse about money when I probably should be taking more risk given a financial position many would love to be in. So I don’t love money – in fact I’m increasingly obsessive about it which I hate.

Thanks for the thoughts all (and welcome back Mathmo. 🙂 )

Regarding my own desire to have the freedom to live off income and not touch capital — despite not dependents — it’s a fair point that does suggest I see value (/love?!) in having my stash for its own sake. However I’d offer a few counters.

Firstly, we live in a time of unprecedented technical change. It’s not clear to me that life expectancy is at all static, even though it has been curbing/topping out recently. I am not comfortable looking say 40-50 years into the future and dwindling my pot down to zero, against a world that, who knows, may be solving old age frailty and mental infirmity (perhaps via virtual realities or similar, who knows). We can wildly speculate about such stuff, of course, but if I have the option (which I plan to) I think slowly getting rid of all my options/firepower sounds willfully reckless.

Also on uncertainty, I far prefer the idea of absenting myself from the debate then arguing whether 3.25% or 2.68% is a sustainable withdrawal rate. I personally believe higher rates of withdrawal will be possible in most outcomes than most commentators these days seem to believe, but I don’t want to find out in the field. It’s totally against the way my mindset works.

On that note, one of the best arguments for living up to certain unproven beliefs such as religious feelings or humanism or the faith that humanity won’t incinerate itself via nuclear weapons or global warming or whatnot is that having such beliefs can improve life personally (and perhaps more widely) day-to-day. If you believe there’s a divine purpose in life, simply put, you will enjoy each day more than if you have a hunch there isn’t. I sort of see my goal to live off income similarly. It is more of a stretch, it means I haven’t ‘early retired’ yet, and when I do (my version of it) it means I won’t spend as much as I would if I was eating my own tail via eating into my capital. But on the way up and day-to-day, I feel given what I know about how I think, my life will be more congruent with my plan, for me, personally — even if it turns out when I do my last Weekend Reading and shuffle off that I could have lived like a hip-hop mogul for 20 years if only I’d touched the precious capital.

Finally, it’s true that it looks like I won’t have any children, and it’s true that I believe inheritances are iniquitous and should be taxed at 80-95% anyway (or better 100% over some threshold such as, say, £50,000 per person — I am freestyling these figures, we can debate all this again some other day).

But there are ways I consider more worthy/justifiable/less socially destructive of deploying my capital than making some people randomly rich when I die, such as charities, or start-up businesses, say. I can imagine earmarking a growing pot of capital for such a use – and perhaps getting involved with it well before (hopefully!) the last — could be life-enriching, even if it seems to amount for much of the time of just husbanding a big wodge of cash and investments. 🙂

But who knows, perhaps that proverbial bus has my name on it already and it’ll all prove moot. If that happened today I’ve definitely been too infatuated with money over the past decade, I think. There’s stuff I would have done, but didn’t.

But that’s a bit like the “how would you live the next day if you only had 24 hours left to live” question. Even I wouldn’t be commenting on my own blog, I don’t think — but with luck I fully expect to be blogging here for the next decade and hopefully potentially much longer. 🙂

@TI, thanks that’s a very interesting comment. Getting involved in a start-up business sounds pretty life enriching to me too. I hope I am able to make myself part with the capital when the time comes.

For my own part I know my heart wanted to hoard the precious before I came up with a logical justification for doing so. The Pangloss in my brain is saying “All of your justifications are for the best, since you have the best of all possible plans” but I’m trying to ignore him.

Interesting brief article on recent survey that groups people into those who find purpose in their work, those who do it for status and those who do it for money https://www.fastcoexist.com/3063039/understanding-the-purpose-driven-worker-and-why-its-ok-if-youre-not-one . These very personal differences in motivation may explain some of the variation in readers attitudes to work, financial independence and retirement.

@old_eyes interesting article.

I would describe it as interest and challenge that I find in work (most of the time) and money a little because it does pay the bills.

I wouldn’t claim it gives me a purpose unless maybe I did something to help an open source or charity project I believed in.

A surprising number of people don’t even think much about money, they just follow the rest of the herd – education, job, retire when burnt out and just hope there’s enough to be comfortable at the end.

For those who do like to think though, your attitude changes with your circumstances, as has already been alluded to in this thread. Personally, since money ultimately represents freedom to me, I worry about running out because I never want to be in a position again where I have to follow orders.

Living a decent life, then making it to the end in comfort is the general plan, after which, it’s easy, I don’t have to even consider various options, I have younger siblings, so anything left when I’m done wasting oxygen is their good luck. (that I never had)

That’s just how society is. You need money to do everything and if you don’t have money you’re screwed. It’s not that I’ve fallen in love with it, but it’s important to my survival.

Maybe I have a fairly low expectation of what I expect to get from work; it needs to pay the basic bills and beyond that if it’s interesting it’s a bonus.

Just came an article on this subject http://www.thebookoflife.org/how-we-came-to-desire-a-job-we-could-love/