by The Investor

on February 2, 2009

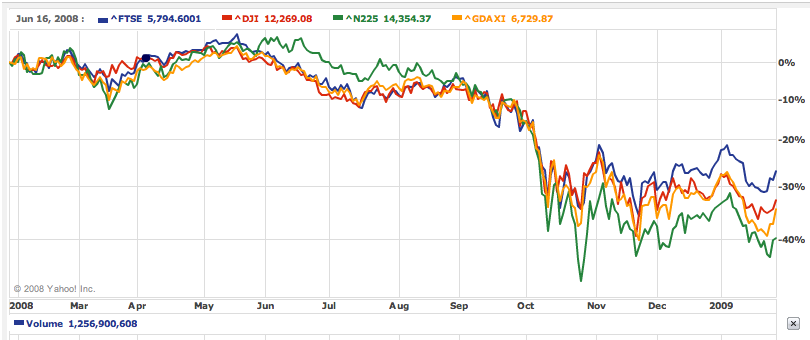

World markets have moved in step through the credit crisis (click to enlarge)

(Source: Yahoo)

Books on investment often suggest investing overseas as a method of diversifying your portfolio. There are several reasons why investing abroad can be a good idea, including:

- If one country or region’s market is doing badly, another could be doing well. Mixing up the returns from several regions helps to smooth the return from your investments.

- Some countries have very different economic profiles to the mature Western regions. In particular, India, China, and other emerging markets are expected to grow much more rapidly, although the journey will be bumpy. Allocating 5-10% of your portfolio to emerging markets enables you to capture some of the growth without suffering too much volatility.

- Currency factors. If you’re an American investor and you invest in European stocks, you will be exposed to the performance of the Euro versus the dollar, as well as the performance of your European stocks. Different currency pairs can diverge a huge amount over time, further diversifying your portfolio – albeit at the cost of extra risk.

Diversifying overseas sounds great in theory. But as the graph at the start of this article shows (click to enlarge), the major world markets have moved in step in recent times.

Even before the credit crisis, many commentators were saying the world’s markets were becoming closely coupled. Is there any point then in putting money overseas?

[continue reading…]

Thanks for reading! Monevator is a spiffing blog about making, saving, and investing money. Please do sign-up to get our latest posts by email for free. Find us on Twitter and Facebook. Or peruse a few of our best articles.

{ }

by The Investor

on January 30, 2009

Zero interest rates arrive at TD Waterhouse

Looks like the age of 0% interest rates has come early for customers of TD Waterhouse in the UK, which just announced the rates pictured for cash held in its various share dealing accounts.

Dealing accounts typically offer terrible interest rates on uninvested cash, but 0% is taking the biscuit (or rather all of the interest the uninvested cash generates).

{ }

by The Investor

on January 28, 2009

With the price of bank shares being driven by fear, should we avoid them completely? Or if we do want to get specific exposure to banks, which banks look the best?

As a private investor, I can only tell you what I’m doing (and remind you an index tracking fund should underpin your portfolio, not individual stock picks).

My personal view is that bank shares will continue to oscillate wildly until house prices stop falling. Then banks should begin to strengthen.

Further falls in house prices in the UK (which I expect) will hit our banks further, though I suspect the scale is now manageable after their capital raising and/or government injections. Much will depend on the performance of their other debt, such as loans to companies struggling through a recession.

The positive spin is that absent a global economic meltdown causing 30-40% of homeowners to default, any bank that survives the credit crisis will at some point be worth a lot more than today. Assets such as mortgages that were previously written right down will then be revalued upwards. (See my post on Prodesse, the investor in US mortgages).

[continue reading…]

{ }

by The Investor

on January 27, 2009

Barclays Bank shares rose 72% on January 27th

Source: Digital Look

I don’t know what annoys me more: That Barclays Bank shares rose 72% on Monday while I was still finishing off a post suggesting they might be worth a punt, or that I didn’t buy any myself.

Oh ‘greedy’ side of the fear-greed investing equation, how we’ve missed you.

[continue reading…]

{ }

{kind=link}