Monevator reader Anna sent us a common question about investing in particular sectors of the stock market:

How should one behave if I would like to be overweight in a specific sector or theme, like clean energy or AI for instance, or perhaps being overweight in a specific country like Russia? Would it be possible to implement these themes in the global portfolio?

Our world is changing rapidly. The ground rules of our lives constantly shift beneath our feet as society is reshaped by geopolitical, socioeconomic, technological, and environmental transformation.

Surely we need to reposition our portfolios, then? Tweak them like wind turbines, pivoting to harness these powerful forces?

There’s an exchange-traded fund for that

The ETF industry certainly wants to help you feel like you’re in control.

For example a dozen climate change ETFs launched in Europe in 2020 alone, according to the ETF data service justETF.

Other ETFs enable you to invest in everything from cannabis to robotics, through esports, gender equality, genomics, and immunology.

Like fashion houses, fund providers know their job is to stay on trend.

Those options come on top of existing ETFs targeting sectors and industries, smart beta strategies, countries, and regions.

And that is but a cherry balanced on a giant fruitcake of investments of every candy-stripe – slicing and dicing the global economy into a pick ‘n’ mix cascade.

All you have to do is predict which themes, megatrends, rising powers, and techno-tipping points will profitably rewrite the future.

(Ahem. “All”…)

Spread your bets

There was a similar explosion of ETFs in 2018 that enabled us to invest in exciting themes such as:

- Blockchain

- Cybersecurity

- Artificial intelligence and robotics

- Bio-tech

- Battery tech

I picked a selection at random to see how they did.

It turned out that all these ETFs beat a plain old MSCI World ETF in the short-term 1:

Source: justETF [Click to enlarge.]

- The MSCI World ETF benchmark (orange line) falls flat into last place with a 28% cumulative return over two years.

- The battery ETF (grey line) went from last place to third in just six months, with a 83% cumulative return. Hmm, volatile!

- The blockchain ETF beat the World ETF by less than 2% despite Bitcoin going berserk.

- Try tearing your eyes away from the towering 121% return of the artificial intelligence ETF in the no.1 spot.

First AI beat me at chess, next it’s having my job, and now it’s a better investor, too? Humans are yesterday’s news, baby.

Maybe, but it’s easy to get overexcited about new toys.

Let’s take a longer term view

Here’s some megatrends that I could get medium range data for: 2

- Big tech

- Rise of China

- Global water resources

- Clean energy

- Healthcare in the face of aging demographics

- Global infrastructure fueled by urbanisation

Source: justETF [Click to enlarge.]

This time our MSCI World ‘accept you have no edge’ benchmark ETF (orange line) sits comfortably mid-table.

Three of the selected big trend ETFs beat the world market. Three under-performed.

Here are the scores (returns are cumulative):

- Big tech – 931% – Win

- Healthcare – 268% – Win

- Global water – 267% – Win

- World tracker – 213% – Acceptable

- Global infrastructure – 114% – Fail

- China – 101% – Fail

- Clean energy – 14% – Fail

Are you surprised? Could you have predicted these outcomes in advance?

It’s not that the narrative behind the underperforming themes was wrong.

- The world has continued to urbanise since 2007.

- China has continued to rise.

- Clean energy is a growing part of the world economy.

What then?

- Was the importance of the theme overblown?

- Were the companies overpriced?

- Did the lion’s share of returns fail to accrue to shareholders – diverted instead to management, employees, customers, future investment, or private equity?

- Was the industry hit by an ill-wind? Loss of subsidies, social backlash, constrained by regulation or the technology failing to fulfill its potential?

- Was there something wrong with the index? Perhaps it wasn’t truly representative of the industry or country or was too concentrated in less competitive companies? Or did it include firms that jumped aboard a sexy new trend train but were mere passengers, not the real engines of growth?

Identifying a trend seems to be easier than profiting from it.

A much longer term view

To understand how the roulette wheel of progress affects market performance, I recommend reading Industries: Their Rise & Fall by the finance academics Dimson, Staunton, and Marsh.

Here’s their breakdown by industry sector of the US stock market in 1900 as compared to 2015:

Source: Credit Suisse Global Investment Returns Yearbook 2015

You can see that the market has been radically remixed over a century.

According to the professors:

Of the US firms listed in 1900, more than 80% of their value was in industries that are today small or extinct.

For instance it’s hard not to notice the huge blue wedge devoted to the rail industry in 1900. That snake-jawed Pacman was worth 63% of the market at the dawn of the Twentieth Century.

But by 2015 rail made up less than 1% of the stock market.

Meanwhile 62% of the 2015 US stock market’s value lay in industries that were negligible or nonexistent in 1900.

Back on this side of the pond, 65% of the 1900 UK market value resided in industries that were marginal or had disappeared by 2015, while 47% lay in industries that were small or not yet invented in 1900. (More evidence that US capitalism has been more dynamic than its UK counterpart?)

Here’s how those 1900-era industries fared against the market during the upheaval of the subsequent 115 years:

Source: Credit Suisse Global Investment Returns Yearbook 2015

The wider market is in dark red and is beaten by five industries.

Notice the market is beaten by rail (light green) despite its huge slice of the pie being reduced to crumbs by 2015.

But the runaway winner is tobacco.

What’s the story here?

Tobacco – addictive, cool, seductive as a ‘50s film star – so of course it won?

Given the number of kids in my school who couldn’t wait to drag on a fag, that was a plausible narrative up until the 1990s.

But few industries have taken such a cultural and regulatory battering in the developed world as tobacco since then.

The equivalent now would be placing all your chips on coal as the fuel of the future. Would you make that bet?

The Investor will pop a long in a moment to explain that pumping out cigarettes required little investment in innovation over the subsequent 100-plus years, and so it was wildly cash generative. Reinvesting that cash drove up returns. [Confession: I just popped along and did – @TI]

But multiplying the difficulty of picking a winning sector by the uncertain strength of its business models does not lead to odds I’m willing to take.

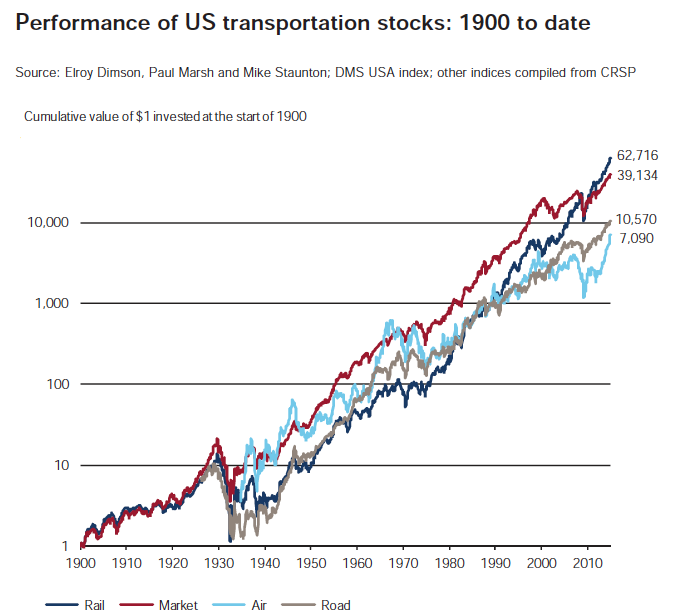

Here’s another counter-intuitive finding. The US rail industry was laid low by the rise of road and air, but rail is the only one of those industries that had beaten the market by 2015:

Source: Credit Suisse Global Investment Returns Yearbook 2015

Rail had a torrid time for 80 years, especially over the 1960s to 1980s. But it emerged fit as a super-productive flea to overtake the market in 2013.

The road industry never beat the market. Air had a few golden ages but always returned to earth with a bump.

Think of how unbelievably exciting the air industry must have looked after the role it played in World War 2. You can see the value of aviation equities spike in the mid-1940s in the graph above.

Would you have predicted that the air industry’s promise would not be fulfilled for shareholders, as opposed to the rest of society?

Could you credit that you’d have been better off just staying invested in the broad market?

The cycle of rise and fall

The merry-go-round of modern capitalism hastens our desire to predict new dawns and to declare existing hierarchies dead.

Survival in the knowledge economy makes us desperate to stay ahead of the curve, after all.

Dimson, Staunton, and Marsh highlight market historian Jeremy Siegel’s explanation of this anxiety from an investing perspective:

Investors have a propensity to overpay for the ‘new’ while ignoring the ‘old’ …

Growth is so avidly sought after that it lures investors into overpriced stocks in fast-changing and competitive industries, where the few big winners cannot compensate for the myriad of losers.

The academics observe how technology cycles through:

- Scepticism

- Over-enthusiasm, which can lead to a bubble

- Sober reassessment once everyone cools off

Could the explanation for the outperformance of AI, robotics, and battery tech in our first example be that investors are caught up in the over-enthusiasm phase?

Dimson, Staunton, and Marsh advise:

Investors should shun neither new nor old industries.

There can be times when stock prices in new industries reflect over-enthusiasm about growth, and times when investors become too pessimistic about declining industries.

However, it is dangerous to assume that investors persistently make errors in the same direction: they may at times underestimate the value of new technologies and overestimate the survival prospects of moribund industries.

It’s clear the market can be beaten. If you’d backed tobacco equities in 1900 then you’d have smashed the market over the long-term.

But can you beat the market?

Remember, as a passive investor you don’t have to get involved in making these explicit bets.

You already gain exposure to AI, robotics, cybersecurity, blockchain, China, and every other plausible investment narrative through a broadly diversified global tracker.

By over-weighting any theme, strategy, or country you’re claiming greater insight than the aggregate of all investing decisions that make up the market.

A market that’s dominated by huge financial players rather than greater fools. A market even the world’s best investors struggle to consistently beat.

Your prospects rest on this key insight from our academics:

It all depends on whether stock prices correctly embed expectations.

Expectations amount to the market’s best guess, given current information.

The smart money has better information than you or I. It reacts to new developments with frightening speed.

- Did you see a global pandemic coming in 2020?

- Did you see shares rebounding right after the fastest crash in history?

- Can you predict the winners and losers as Covid-19 reorders society?

Or, to highlight another sweeping change, will big tech be more or less profitable by the time the antitrust lawsuits have played out?

As ex-hedge fund manager Lars Kroijer wrote about overweighting:

What is it that you know that the wider market doesn’t?

The best strategy is to be humble

Plan A is to stick with a global tracker fund.

Can’t resist a wee flutter?

Plan B is to limit the damage of being wrong.

Just like you wouldn’t bet your house on the outcome of the Grand National, keep your stock market bets survivable.

Overweight 10% of your equity allocation, tops.

Enough to enjoy your win should you back the right horse. But not so much that the pain will unbearable if you invest in the next air industry or Argentina.

Take it steady,

The Accumulator

- The time frame chosen was simply the maximum span over which I could compare these ETFs. It was no more scientific than that, and I don’t think it tells us anything except that the short-term is no guide to the quality of investing decisions.[↩]

- The time frame is the longest period I can compare the ETF selection against each other.[↩]