Good reads from around the Web.

I really liked this extended metaphor of the stock market as a forest, from Nate at Oddball Stocks:

I want you to think of the market as a forest. A healthy forest is filled with a variety of trees and plants. There are tall trees, short trees, pine trees, oaks, maples, beeches, bushes, grasses, weeds, as well as numerous other plants. A forest doesn’t grow all at once, it starts with a few grasses and slowly evolves into something mature. Markets are similar, they don’t develop at once, they grow into maturity.

In a forest not all saplings grow into towering trees. Many saplings thrive for a while only to be deprived of enough sunlight or good soil before perishing. Sometimes a sapling falls victim to a grazing deer, or other destructive animal. Likewise there are more smaller companies in the market and not all of them will grow large. Some are small trees won’t ever grow tall. Some fall victim to a predator, or are crowded out of the market place.

Given the right conditions, the right soil, and the right seeds a tree can grow large. A tree doesn’t grow all at once, it takes decades. As a tree journeys from a sapling to a stalwart many things can happen destroying its progress. A tree might drop hundreds or thousands of seeds of which only a few become full fledged trees. Even less seeds become giant trees. A giant tree needs perfect conditions to crest above the other trees. Once it obtains a certain size it’s own size becomes a strength. A larger tree can steal sunshine and nutrients from the rest of the forest. Size becomes a strength for a while.

Trees don’t grow to the sky, eventually all trees, even the giant sequoias face an untimely end. Large trees are more susceptible to violent wind storms, they aren’t as flexible as smaller trees. If the soil or environment changes large trees they have trouble recovering. Large trees are also targets for lumberjacks whose wood is more valuable.

The market as a forest – or an ecosystem – is hardly a new metaphor, but Nate puts it really well.

Still, metaphors shouldn’t be entirely mixed up with reality.

As an active investor you are usually trying to either smaller trees that will grow faster than those around them, or else big trees that mistakenly seem small to other lumberjacks. A real forest has few such optical illusions, while attempts fence in promising saplings are doomed to legal and possibly biological failure.

Perhaps passive investors fair better with the metaphor? Like an owner of forestry assets or even a tribe of hunter gatherers, they get to benefit from all the riches the forest provides, whether the fast growth from seeds, the cool shade of the giants, or the fruit that falls from the more productive trees (as dividends).

Again though the metaphor founders slightly. Running a forest for profit is not cheap, which is why forestry funds tends to have high fees. Yet passive investors prize low costs above all but an accurate index.

I’m really nitpicking to extend the discussion though – I think elegant metaphors are useful, whether you’re a new investor or an old hand in danger of losing the wood for the trees (boom boom!)

Happy Bank Holiday – may all your garden centre trips yield bargains.

From the blogs

Making good use of the things that we find…

Passive investing

- Meet the passive investing dream team – Mintlife Blog

- Change happens in real-life investing – Retirement Investing Today

Active investing

- Chuck Akre: The best investor you’ve never heard of – Clear Eyes Investing

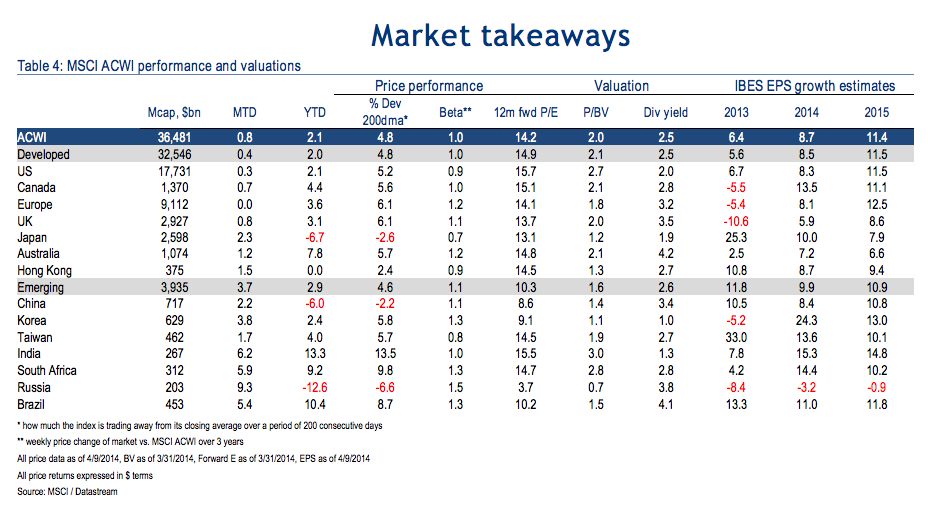

- The world’s markets, by size and valuation [Table] – Reformed Broker

- Analysts should focus on valuation, not forecasts – The Value Perspective

- Sainsbury: Buy, hold, or sell? – UK Value Investor

Other articles

- How Hargreaves Lansdown makes its money – Simple Living in Suffolk

- The stock market is not where you get rich – Pragmatic Capitalism

- Financial advice and innovation – Rick Ferri

- Does renting out a property make sense? – Mister Squirrel

Float flop of the week: Saga has floated, but at 185p the price is at the bottom end of expectations. If you’re one of the hundreds of thousands who bought in, check out this explanation from The Telegraph.

Mainstream media money

Some links are Google search results – in PC/desktop view these enable you to click through to read the piece without being a paid subscriber of that site. 1

Passive investing

- Michael Lewis on rigged markets and index funds – ThisIsMoney

- Lower costs are best in all market conditions – MorningStar

- Incompetent pension boards enrich fund managers – I.I.

Active investing

- Russia looks really cheap by the Tobin Q metric – ETF.com

- How do hedge funds get away with it? – The New Yorker

- Will Vodafone’s big spending pay off? [Video] – YouTube/TMF

Other stuff worth reading

- Britain’s housing dilemma [Search result] – FT

- You need £15,000 a year from a pension to be happy – BBC

- Everyone has their own version of history – Housel/TMF US

- Your brain doesn’t understand risk – Bloomberg View

- UKIP: The bearish case for Britain – Buttonwood/Economist

- The college dropout fallacy – Slate

Book of the week: John Hulton, who runs the DIY Investor UK blog, has written another eBook on investing. This latest is all about maximising income from savings, investment trusts, shares, and bonds – an ever-popular topic. DIY Income: A Practical Guide is only 82 pages long, which some may see as bonus – though more is often more for investing nerds like me. At £2.96, it looks good value on a per page basis though. I may well grab a copy.

Like these links? Subscribe to get them every week!

- Reader Ken notes that: “FT articles can only be accessed through the search results if you’re using PC/desktop view (from mobile/tablet view they bring up the firewall/subscription page). To circumvent, switch your mobile browser to use the desktop view. On Chrome for Android: press the menu button followed by “Request Desktop Site”.”[↩]

{kind=link}

Comments on this entry are closed.

TI,

Many thanks for the mention of my new ebook!

“You need £15,000 a year from a pension to be happy”. A discussion at MSE seemed to conclude that that figure is the gross sum and that it applies to a household not an individual. In which case I have to say it doesn’t apply to us.

@dearieme I’m also surprised by that, I’ve assumed the target is per individual and net, though at that level with careful planning across pensions and ISAs the difference between net and gross can be minimised. I haven’t spent that much for a while, but I’d hate not to be *able* to…

@ermine @dearieme

Looking at the bigger picture, NEST carried out the research. NEST are trying to encourage not to opt out of work place pensions and with their example savings it works out at 15k a year per family unit. It’s aimed at the people who claim there is no point in pensions.

You guys are sophisticated and savvy and will have saved more and have more needs/want to meet.

Presumably it’s no coincidence that it’s somewhere about the size of two of the new-style State Retirement Pensions. I now forecast that in 2016 onwards we will not hear the end of the incessant whine of “pity us poor pensioners”, even from those couples who are on £15k per annum.

By the same token, I think of my SIPP in the same way as I do my compost bin. I don’t get too fussed about the asset allocation, although I do try to stick to a balance of UK, ex-UK and bonds (or greens, browns and moisture) but mostly focus just on keeping it topped up. Time in the market (or for the worms to do their thing) is the thing…