A few years ago I wrote about market efficiency and investing edge [1] – and about how you don’t have it.

But let’s dig deeper into why this is true.

You often hear from retail punters and professional investors alike that passive (or index) investing makes markets less efficient.

Their argument is that this inefficiency is what justifies active management.

Well, they’re wrong – but not in the way you might think. The reality is more nuanced.

Let’s do a little maths to explain how passive investing actually makes life harder for active managers, not easier.

Model market: Alice, Bob, and Clifton

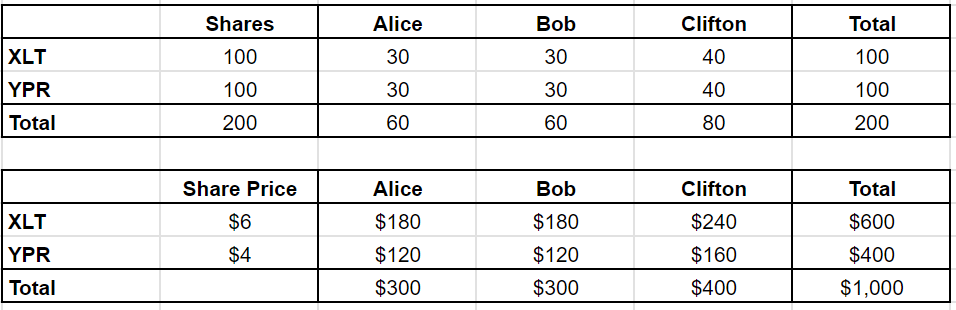

Imagine a market with two stocks, XLT and YPR, and three investors: Alice, Bob, and Clifton.

The total market capitalisation is $1,000.

Between them, Alice, Bob, and Clifton hold portfolios that add up to that $1,000.

There are no other companies and no other investors – we’re keeping things simple – but the ways in which this model is ‘wrong’ are not really material to the point today.

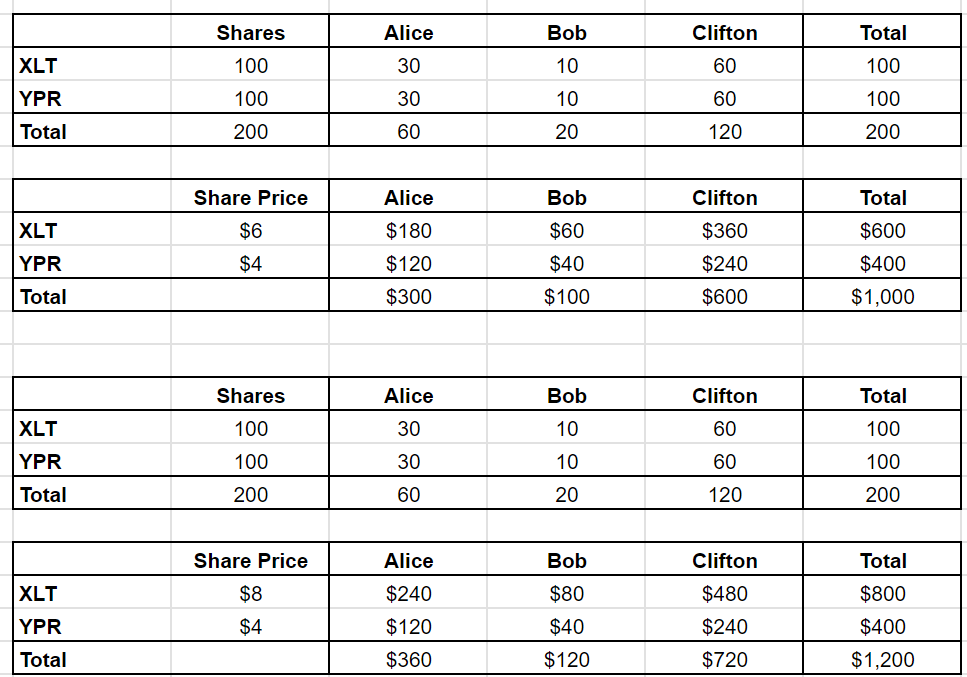

Alice and Bob each hold $300, while Clifton has $400.

XLT and YPR each have 100 shares outstanding, with XLT priced at $6 per share and YPR at $4.

(Yes, this is starting to sound like GCSE maths, but stay with me.)

In other words:

Now, Alice, Bob, and Clifton all hold market weight portfolios. This makes them passive investors by default.

Ideologically though, Clifton is your classic index fund investor – passive [2] through and through.

Alice and Bob, on the other hand, are active traders. They are willing to take a punt if they sense an edge.

So this market is 40% passive (Clifton) and 60% active (Alice and Bob).

Dumb passive money?

One common misconception is that passive investors blindly ‘buy expensive stocks’ when prices rise.

Let’s expose this myth with an example.

XLT releases stellar results before the market open, and Alice decides she’s bullish. She calls Bob to buy some of his XLT stock, knowing that Clifton – the passive guy – basically does not trade. (Clifton doesn’t even bother going to the office till after lunch!)

Here’s how their conversation goes:

Ring, ring…

- Alice: “Hey Bob, I’m in the market for XLT. What are you offering?”

- Bob: “Hmm, I saw their results. Strong stuff. I’d have to start with an 8…”

- Alice: “I was thinking more like $7.95.”

- Bob: “LOL, nope. I’d buy from you at that price. $8.05 – final offer.”

- Alice: “I’ll leave my bid on Quotron. Call me if you change your mind.”

- Bob: “Catch you later.”

When Clifton finally gets into the office – sometime after his tennis match and a long lunch at the club – he logs onto his Quotron and sees that XLT has jumped 33% to $8.00.

A news headline reports: XLT Surges on Blowout Results – Light Volume.

Pleased with his morning’s ‘work’, Clifton updates his portfolio to reflect the new prices.

So note that nobody did any trading at all here. Alice and Bob just sort of agreed that $8 was a reasonable price for XLT, and so, by proxy, did Clifton.

This is how most price moves in the stock market happen. You don’t need trading to move prices.

The alpha chase

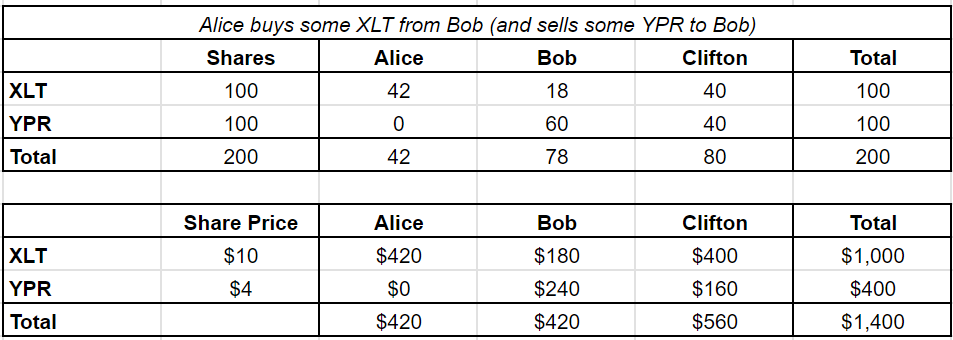

Fast-forward a few weeks, and Alice gets some inside info on XLT – let’s say from a friendly round of golf with its CEO. The company is about to secure a major government contract.

Alice tries again to buy from Bob, who smells something fishy. He agrees to sell her some XLT shares – but at an even higher price, $10 per share.

Since this is a closed system, Alice needs to sell YPR to raise the cash to buy XLT. And guess who she has to sell it to? Bob. They agree to swap their stakes.

Alice is now all-in on XLT, while Bob holds more YPR. (For convenience we’re ignoring that Bob would probably demand a discount on the YPR he’s buying, as well as a premium on the XLT he’s selling – Alice’s ‘market impact’).

Here’s a status check:

And here’s the kicker: for Alice to overweight XLT, Bob must underweight it. Clifton, as the passive investor, doesn’t change his positions at all.

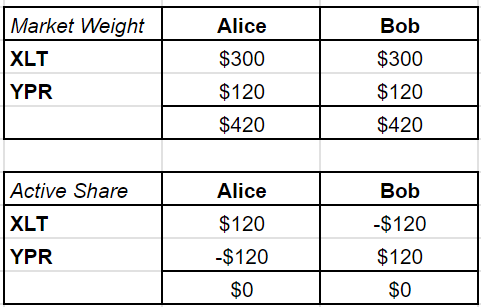

This is a zero-sum game [3]. Every dollar of ‘active share’ that Alice holds has to be offset by Bob’s:

None of this has changed their relative portfolio values – but it will.

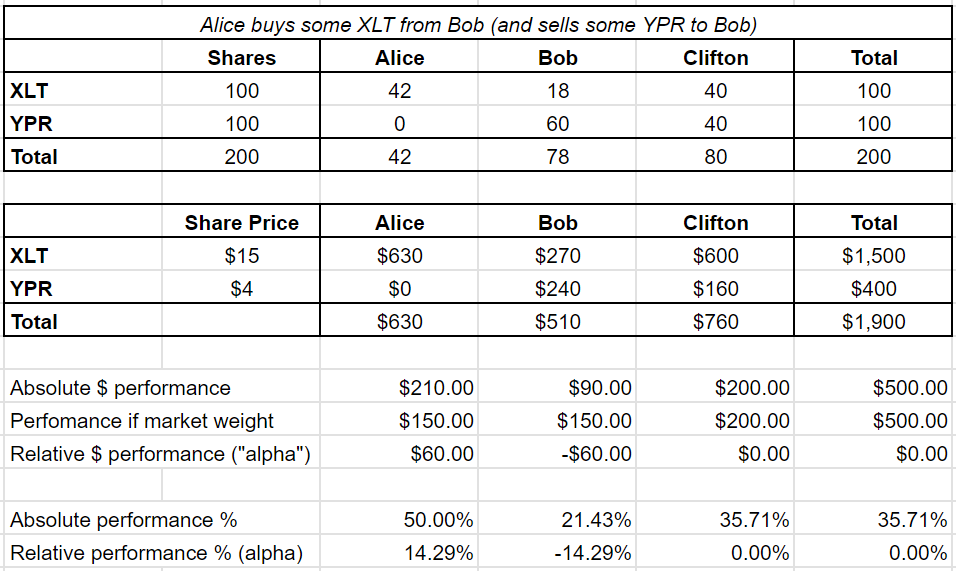

When XLT surges 50% on news of the contract, Alice makes a $60 profit.

But Bob? His loss is the exact mirror of Alice’s gain:

Since anyone can just buy the market, what matters for active investors is outperformance.

Alice’s outperformance (aka alpha or profit) of $60 is exactly offset by Bob’s underperformance of $60.

Bob still made money. Just less money than he would if he’d stayed market weight.

I know I keep making the same point, but it’s important: Alice can only make her $60 alpha at the expense of Bob.

The winner needs the loser. 1 [4]

Increasing passive share

Now let’s imagine that Clifton, our passive investor, controls more of the market than before.

Let’s say the market has shifted so Clifton now runs $600 of the total $1,000.

Meanwhile Bob only has $100 to manage while Alice’s capital stays the same at $300.

The passive share of the market has grown from 40% to 60%. Let’s re-run that first conversation between Alice and Bob that bumped up the price of XLT to $8, to see where it gets us.

Ring, ring…

So far, nothing changes. However when Alice returns from golf with XLT’s CEO and tries to buy more shares, things get trickier.

Bob doesn’t have enough shares to sell her all that she wants. Now Bob only has ten shares of XLT, priced at $10 each, for a total of $100.

Alice has $120 worth of YPR to sell, but she can’t buy as much XLT as she would have liked:

As passive investors like Clifton take up more market share, Alice’s strategy runs into a brick wall. She can’t go all-in on her insider tip because there aren’t enough active participants to trade with.

And that’s a major problem for her alpha.

In fact let’s check what it’s done to everyone’s alpha compared to our previous example of 40% passive market share:

[5]

[5]It’s got worse for everyone except Clifton!

- Alice’s alpha has reduced.

- Bob’s negative alpha, in proportion to his capital, is now even worse.

- Clifton doesn’t care either way.

The passive doom loop

Let’s imagine that Alice keeps getting lucky – or inside information – and Bob consistently underperforms.

Eventually, some of Bob’s investors will redeem their money. Diehard believers in the quest for outperformance, they would like to hand it to Alice – but they can’t.

Why not? Because Alice’s strategy is capacity-constrained.

Alice can only make money if she can trade against someone else, like Bob. But if Bob’s investors leave him and put their money into Alice’s fund, she’ll have fewer people to trade with – meaning she can’t deploy the capital effectively.

Bob’s redemptions have to flow to Clifton.

And so passive money grows, and active managers like Alice and Bob have ever fewer opportunities to beat the market. As passive share increases, active management becomes harder and harder.

It does not matter how good Alice’s inside information is. Her ability to monetise her edge is limited by the supply of suckers she can trade against.

This is where the so-called doom loop comes in.

As passive investing grows, active investing gets tougher, which drives more money to passive funds, which makes life even harder for active managers… and so on, in a vicious cycle.

Who’s Alice?

So, how do you spot a bad hedge fund?

Easy. They’re the ones willing to take your money.

The true hedge fund giants – names like RenTech, Citadel, and Millennium – won’t even let you invest.

Why? Because their alpha is capacity constrained.

These guys often can’t even compound their own money.

If you’re an investor with RenTech – which means you’d have to work there – it cuts you a cheque for the profits every quarter. You don’t get to leave the money in there compounding for the long-term.

Such funds have already soaked up all the market inefficiencies their strategy has unearthed.

They can’t let just anyone in – in fact they need suckers on the other side of their trades, so why not you.

Don’t be Bob

Finally – who is Bob?

Bob is anyone willing to underperform for long periods without having the money taken away.

For years, this was the underperforming active mutual fund manager.

Now? Increasingly, it’s retail investors.

Why do you think hedge funds, prop shops, and market makers will pay brokers to trade against their retail order flow?

*Cough* *cough* – I mean, provide ‘price improvement’ services!

Don’t be Bob.

Follow Finumus on Twitter [6] and read his other articles [7] for Monevator.

- Incidentally I hope our model market makes it obvious, if it wasn’t already, that Alice’s insider trading is not a ‘victimless crime’. She is taking money directly from Bob.[↩ [8]]