Note: DeFi is the Wild West of even the wildest frontiers of investing. Seriously, messing about with DeFi makes punting on GameStop [1] look a hobby for widows and orphans. This piece is for general interest and the (mis)education for those who want to know more about the Byzantine realm of DeFi. It is definitely not advice to do anything.

Like Fight Club, the first rule of crypto is: don’t talk about crypto. Unless you’re a crypto ‘bro’ on the Internet, that is.

In which case the rule seems to be to never discuss anything else.

But back in what we increasingly must call ‘real-life’, mentioning crypto to your friends will probably prompt one of several judgements:

- You’re a boring nerd.

- You’re an idiot for promoting a pyramid scheme.

- You’ve gotten rich out of it but they haven’t, and now they feel inadequate.

- They assume you’ve gotten rich out of it – but you haven’t, and now you both feel inadequate.

None of which will do much for your social life.

We’re among a different sort of friends here, however. And let’s face of it – most of us are Type 1s.

So let me tell you a story.

Bank error in my favour

A year or so ago I accidentally [2] made £1 million in a small cap crypto-mining stock, simply because my bank wouldn’t let me send money to Coinbase.

Yes. Really.

Afterwards I rectified the banking situation, just in case I should need to buy any crypto again.

I wasn’t particularly looking to ‘do’ anything in crypto, mind you. I just wanted to make sure the pipes were clear if I got the urge.

Soon enough that opportunity presented itself.

Pump and dump

So-called pump and dump [3] schemes are rife in the crypto world. Long illegal in the real-world, crypto and social media have given them a new lease of life.

Here’s how it works. An organized group of insiders quietly buy up a lot of some small cap coin. They then promote it to their followers, who in turn buy it up and further ‘pump’ it on social media – until at some point everyone ‘dumps’ it onto whomever was last in.

Apart from the initial insider buying, all this unfolds over a few seconds. It’s an ultra-high-frequency Ponzi scheme. Prices sometimes go up 500% or more in a few seconds after the target coin is announced.

Having been something of a market micro-structure geek in a previous life, I thought all this was quite interesting. Especially if I could identify the coin that the promoters were quietly buying it up, pre-pump.

Musing on Twitter about the likely identity of the next such coin, I fell in with some other people trying to do the same.

And we sort of did.

Well, once, and only once, the first time, we guessed right.

We made quite a lot of money in about five minutes. It felt great at the time. But it also gave us a great deal of false confidence .

The truth is we’d just got lucky.

And despite many hours of work – and money spent buying the wrong coins – we never repeated the trick.

Also whilst we’d never actively promoted anything, it raised the question of whether we were taking advantage of the same suckers as the promoters?

So we gave up.

Mental accounting

A healthy dollop of mental accounting [4] and house money [5] bias meant I kept this pot in cryptocurrency.

Indeed I’d learnt quite a bit about the crypto ecosystem in my explorations. (Not least that it contained a lot of scammers.)

So I set myself up for the long haul. I got a hardware wallet, bought a few coins I liked the sound of, and then put the rest in stable coins [6].

The question then turned to how to maximise the yield on these assets.

DeFi lending

My first introduction to decentralized finance (DeFi) was lending my stable coins on platforms like AAVE [7].

The concept here is pretty simple. A borrower posts collateral, say Ether. They then then borrow against it, at a loan-to-value (LTV) of say 30%.

If the price of Ether falls such that the LTV rises to 60%, for instance, the Ether gets sold automatically.

But why would people want to borrow stable coins against their crypto?

Two reasons:

- Tax. Let’s say I have $10m worth of Bitcoin [8] that I bought eons ago for circa $0 (I don’t for the record), and I want to buy a house worth $2m. I can sell $3m worth of Bitcoin, pay capital gains tax of $1m, buy my house, and be left with $7m worth of Bitcoin. Alternatively, I can borrow $2m against my Bitcoin, buy the house, pay no tax, and still have $10m worth of Bitcoin.

- Leverage. Is 200% annualized volatility not exciting enough? A crypto whale [9] might do the same trick but buy more Bitcoin with the money they’ve borrowed. This is pretty alien to me – I prefer to apply leverage to low volatility assets like property or bonds – but each to their own.

All this is managed through smart contracts, so there’s no need to trust anyone. (Okay – it’s slightly more complicated than that).

These sort of arrangements are one reason why crypto is so volatile – automated liquidation cascades from leveraged platforms.

Anyway, lending on these platforms could net me mid-single-digit yields on the USDC [10] stablecoin.

I don’t like the more popular Tether (aka USDT), because it seems so obviously dodgy. For a while I even tried depositing USDC on the AAVE platform, borrowing USDT, selling it for USDC, and then depositing the USDC back in AAVE.

Effectively that created a position where I got paid to be short USDT. But I suspect we may be waiting a long time for that situation to blow up.

Incidentally, if you’re earning yield in one of the centralised exchanges like Coinbase, they are just doing this sort of thing on your behalf – for a cut.

Much simpler and maybe worthwhile from an admin perspective.

Liquidity provision

Soon enough even this got pretty boring. So I started experimenting with Automated Market Makers (AMMs) and liquidity provision on platforms like Uniswap [11] and SushiSwap [12].

AMMs are a central DeFi building block. They enable users to swap one token for another in a trust-less fashion.

I’m not going to get into the mechanics (others have [13]). In simple terms, you supply a pair of tokens (ETH and USDC, say) and you’re betting that the fees earned outpace the losses from being arbitraged.

The risks?

The biggest is the deceptively-branded ‘impermanent’ loss (there’s nothing impermanent about it) if one asset moves a lot versus the other asset.

And of course ever-present smart contract risk [14].

Yield farming

The hyper-competitive nature of DeFi means that protocols (coins and tokens) are competing with each other all the time.

Hence they’ll often pay you (in yet another pointless token) for providing liquidity on their platform, as opposed to someone else’s.

You want to sell these ‘reward’ tokens as soon as you can. They aren’t really useful for anything else – they are ‘down-only’ assets.

But why not automate the process, constantly sell the rewards, and invest the proceeds back into the liquidity pool?

Doing it manually is a bore – but there’s an app for that. So-called ‘yield optimizers’ get it done whilst adding another layer of smart contract risk.

And guess what? These all compete with each other too, so they’ll pay you in some other pointless token to use their yield optimizer.

And so on and so on. You can see why people call this stuff ‘Money LEGOs’.

(The lingua franca of crypto is American English, so no, not ‘Money LEGO’.)

More DeFi hot air gas

The amazing thing about the whole space if you come from a traditional finance background is the rate of innovation.

Teams build platforms that attract billions of dollars of Total Value Locked (TVL) in a few weeks or days. That’s less time than it would take to get your idea on the product committee’s agenda for discussion back in the centralised world. Let alone actually build anything.

There are downsides. Many of these are scams (so-called rug pulls [15]) for a start.

Also, you’ve got to keep moving your money to get the best returns. Every time you do, you pay a bit of ETH, called ‘Gas’. And that can really add up.

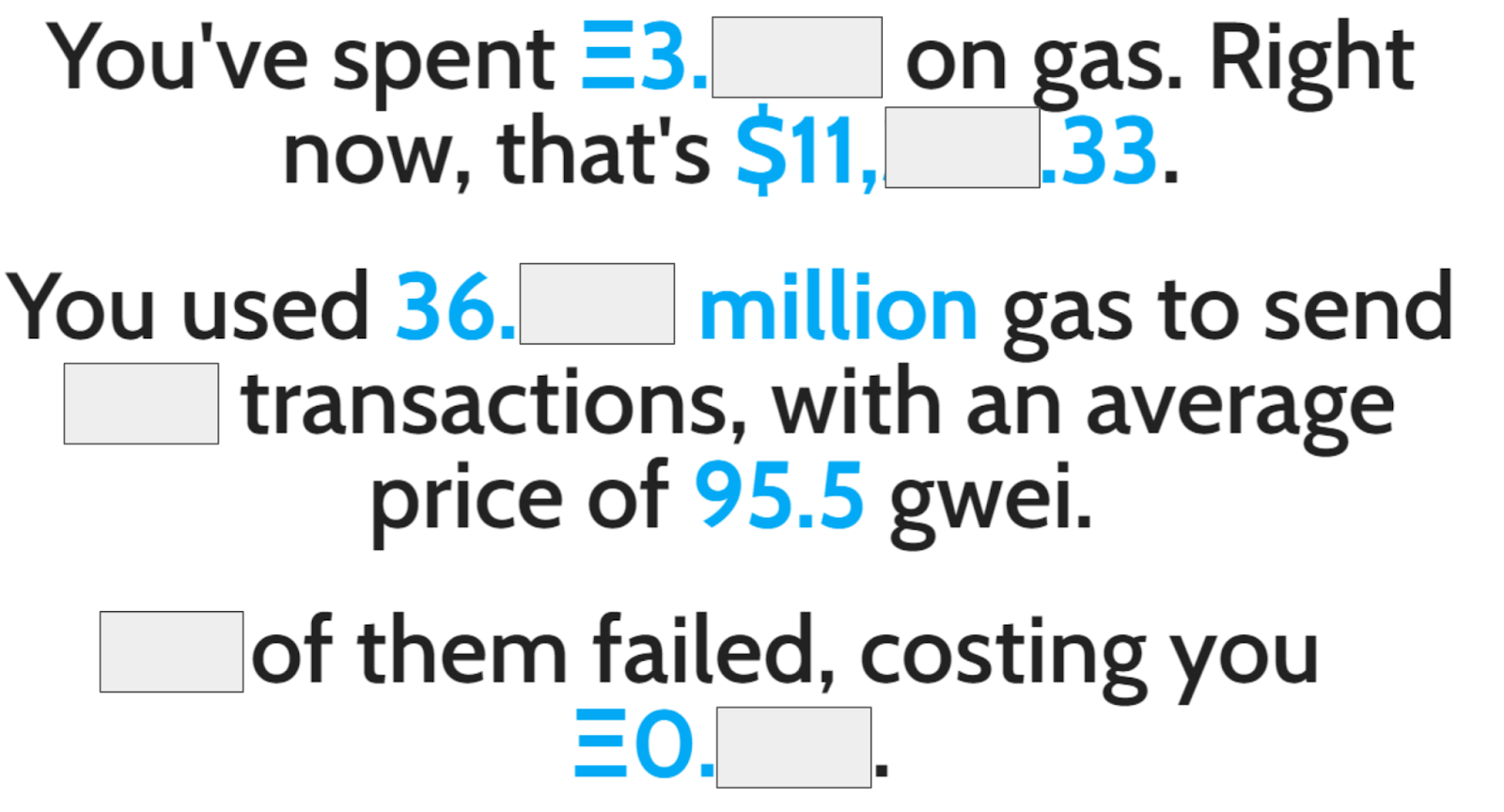

In fact you can go to fees.wtf [16] to see how much you’ve spent:

[Details obscured for privacy.]

Um, $11,000 in transaction fees? Fees.wtf indeed!

I thought this stuff was supposed to cut costs by removing the middleman?

Picking up pennies

Soon enough I was seeking out cheaper blockchains, which, once you’ve ‘bridged’ over to them, open up whole new ways of getting confused. But at least less expensively.

Before you know it you’re:

- On the Binance Smart Chain staking your Cake-BNB LPs on Pancakeswap [17] to earn CAKE that you then stake in its auto-compounder to earn still more CAKE.

- Using Solona and the appropriately named tulip.garden [18] to leverage yield-farm some Samoyedcoin [19]-USDC (with obviously the borrow on the $SAMO leg – leaving you net short the ‘shitcoin’).

- On Terra [20] using the Mirror Protocol [21] to run a delta-neutral long/short farming strategy, but obviously using Spectrum [22] to auto-compound and earn extra $SPEC on the long-leg, to effectively earn 40% or more on UST.

And no I’m never going to say any of those sentences aloud.

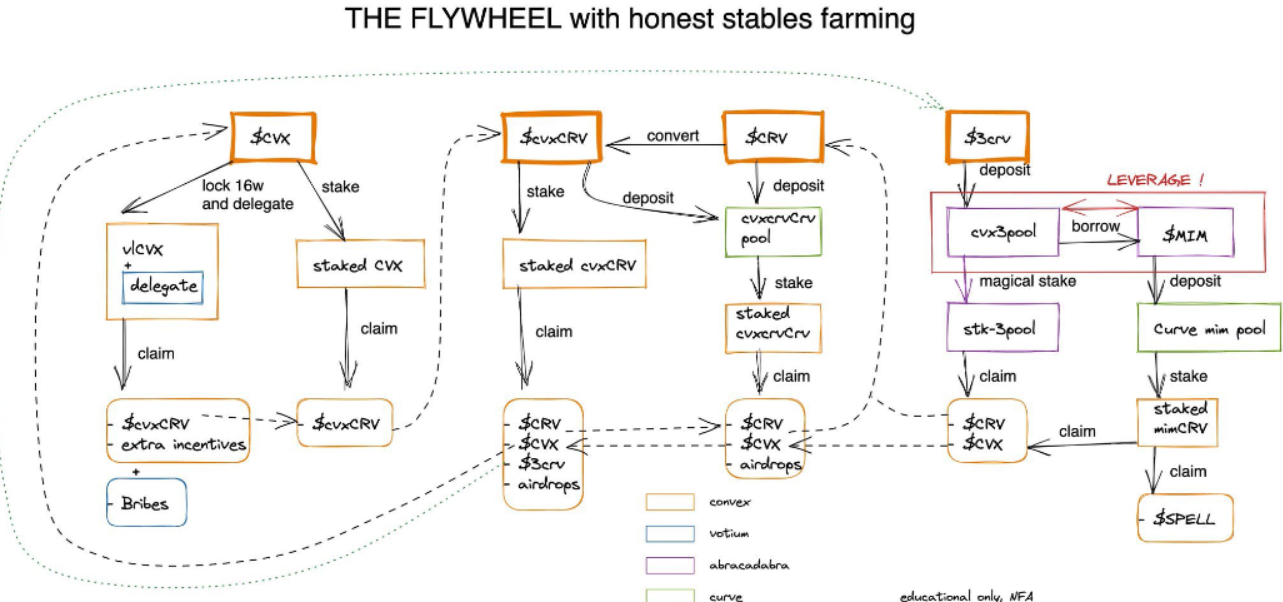

Eventually you come across a flowchart like this 1 [23]:

You think you understand it. You even start to think about putting the trade on.

But then you remember….

Yes, you pay tax on your DeFi gains

It may be news to some of my fellow Guardian readers (“Crypto is burning the planet and is only used by crooks”) but you pay taxes on all of this.

Taxes should be simple. I’ll just give my ETH address to my accountant, and we’re good right?

After all, it’s all publicly on the block chain, isn’t it? My accountant can surely just look it up on Etherscan [24]? In fact I should be able to provide my address to HMRC and it can send me a bill, right?

Sadly that’s not the world we live in.

Whilst HMRC has published some good guidance [25], there’s still a lot of reporting stuff on a ‘best guess’ basis.

Some tax tips

Monevator is not able to give tax advice. However here are a few things to be aware of:

- Do not believe anyone who tells you that tax is only payable once you convert crypto to real money. This is nonsense. Swap ETH for BTC and that’s a sale of the ETH and a purchase of the BTC. There are capital gains tax [26] (CGT) considerations.

- The native reporting currency of crypto is USD. There’s always an extra leg on cost / proceeds calculations to turn it into sterling (GBP).

- There’s a lot of transactions on which both income and capital gains tax are effectively payable. If you receive ‘rewards’, you pay income tax on their value when you receive them. You also form a cost basis, because you will pay CGT on any gain when you sell them. Far more likely though is the opposite problem: their value will fall. When you sell you probably won’t even receive enough proceeds to cover the income tax to pay. Nice!

Tax complexity is a deterrent from engaging in the racier stuff. It’s not the paying that’s the problem. It’s the paperwork.

The lack of any sort of tax wrapper – such as an innovative ISA – or failing that just a simplified reporting regime is frustrating.

Crypto bros get about as much public sympathy as BTL landlord though, so I can’t see this changing any time soon.

Why is there money to be made in DeFi?

In my experience you can make fairly low risk returns of 10-30% per annum in DeFi, at least at the moment.

Which leads to the obvious question: how come?

If we pop our Efficient Markets Hypothesis (EMH) hats on, there’s a few possible explanations:

- Reasonable pricing for risk. These yields represent the correct pricing for all the risks: smart contract flaws, bugs, rug pulls, hacks, legal issues, wrench attacks, self-custody risks, tax risk, and so on. Most of these are uncorrelated with the other risks I take in, say, equities. To be clear, I’m not saying crypto prices are uncorrelated with equities. As we’ve been reminded in recent weeks, these are risk assets like any other – and stablecoin pegs will probably not be maintained in extreme risk-off scenarios. What I am saying is that the risk of my MetaMask wallet getting hacked is not correlated with stock prices. Which all suggests, from an efficient frontier [27] perspective, that there’s a place for a small allocation to defi in a wider portfolio.

- Arbitrage constraints. This theory holds that there’s friction between the crypto and real-money worlds, particularly from an institutional perspective. This constrains arbitrage. Why else would pension funds invest in junk bonds yielding 3% a year, when they could deposit in Anchor Protocol [28] and earn 19.5% a year? I believe these constraints must exist, at least to some degree. But why don’t rich individuals already in crypto bid away these opportunities? Maybe double-digit annualized returns on stablecoins isn’t enough excitement when they believe they can make a 1,000% return on SHIB INU, or whatever.

I suspect there’s a bit of both going on.

Either:

- The whole space will blow-up. Yields are currently high because of the demand for stablecoins to speculate on ‘proper’ crypto. In a long bear market for crypto the demand won’t be there. Hence yields will fall.

- Alternatively maybe institutional money will eventually find the market. Again, yields will then fall.

Either way, yields will fall. It’s only natural. Markets always get more efficient as they mature. Hence why I’m making hay while the sun is shining.

WAGMI [29]! But please please read that disclaimer we started with.

You can follow Finumus on Twitter [30] or read his other articles [31] on Monevator.

- If anyone knows the source we’d love to link to it.[↩ [32]]